What a Tokenized Trade Finance Invoice Actually Is

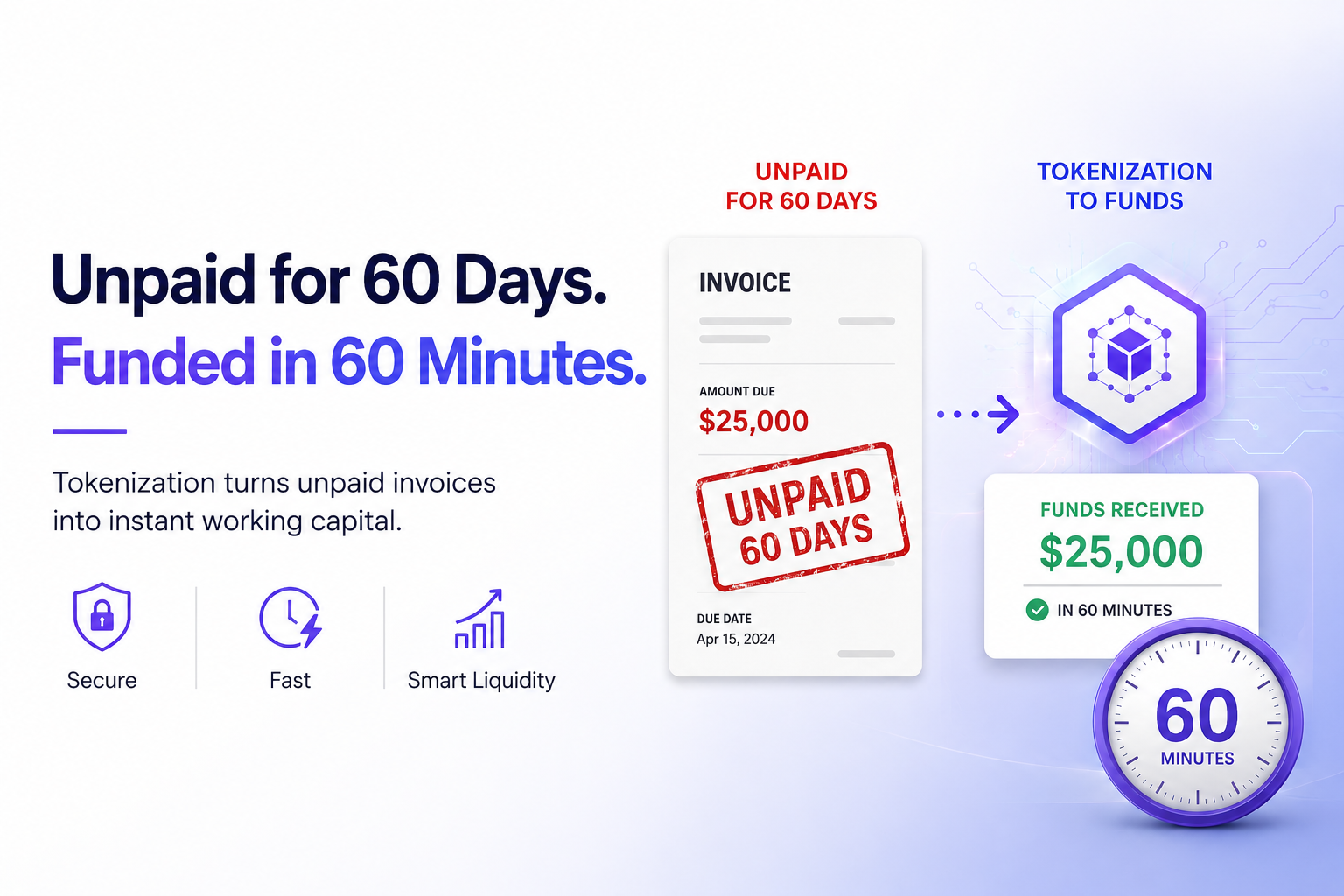

An invoice is simply a request for payment. When you tokenize it, you turn that unpaid claim into a digital asset on a blockchain. This doesn’t change the underlying debt; it changes how the debt moves. Instead of waiting for bank transfers or factoring agreements, the invoice becomes a transferable token that can be held, traded, or used as collateral.

This shift matters because it breaks the friction between the seller and the buyer. The seller gets faster access to capital, and the buyer’s obligation is recorded immutably. The token represents the right to collect that payment, and its value is tied directly to the creditworthiness of the buyer. If the buyer defaults, the token’s value drops, but the record of that failure is permanent and transparent.

Tokenization isn’t just about digitizing paper. It’s about making trade receivables liquid. In traditional trade finance, an invoice is often stuck in a silo, verified by multiple parties, and settled over weeks. Onchain, the invoice can be verified instantly, split into smaller fractions, and sold to investors who want short-term yield. This creates a marketplace for trade credit that was previously inaccessible to most small and mid-sized businesses.

The infrastructure supporting this requires smart contracts to manage the lifecycle of the token. These contracts handle payments, enforce compliance, and distribute returns to token holders. Without this backend, tokenization is just a database entry. With it, the invoice becomes a financial instrument that can be integrated into broader DeFi strategies or traditional banking systems.

Tokenized trade finance invoices choices that change the plan

Moving unpaid invoices onto a blockchain shifts working capital from opaque, relationship-based lending to transparent, programmable assets. For treasury teams and fintech operators, this transition is not merely a technical upgrade; it is a structural change in how risk is priced and liquidity is accessed. Before adopting tokenized receivables, you must weigh the operational friction against the potential for deeper-tier funding.

The primary advantage lies in visibility. Traditional supply chain finance often stops at tier-one suppliers, leaving smaller vendors behind. Tokenization breaks this barrier by creating a verifiable, immutable record of the invoice’s origin and payment terms. This transparency reduces due diligence costs for investors, allowing capital to flow further down the supply chain. However, this benefit comes with the cost of integration complexity and regulatory scrutiny.

When evaluating tokenization platforms, focus on these four concrete tradeoffs:

| Factor | Onchain Tokenization | Traditional Supply Chain Finance | Risk Profile |

|---|

Choose the next step: Turn the research into a practical decision framework

Transitioning from market research to execution requires a structured evaluation of your current infrastructure and strategic goals. Tokenized trade finance is not a simple plug-and-play upgrade; it demands careful alignment between legacy systems and onchain capabilities. The following steps outline a decision framework to help you determine the right path forward.

Before selecting a protocol, audit your internal data structures. Tokenization requires high-quality, standardized invoice data. Assess whether your accounts receivable systems can produce machine-readable, tamper-evident records. If your data is fragmented or manual, prioritize improving data governance before attempting onchain integration. This foundation determines the speed and reliability of future tokenization efforts.

Choose between single-asset tokenization and pooled invoice structures. Single-asset models offer transparency for specific high-value invoices, appealing to institutional investors seeking direct exposure. Pooled models, often backed by diversified receivables, provide liquidity and risk mitigation through diversification. Evaluate your target investor base: if they prefer yield stability, pools may be suitable; if they seek specific counterparty risk assessment, single assets are better.

Tokenized invoices are financial instruments subject to securities, money transmission, and anti-money laundering regulations. Identify the jurisdictions of your invoice originators, borrowers, and token holders. Determine if your tokens will be classified as securities or utility tokens, which dictates the necessary KYC/AML infrastructure. Engage legal counsel early to structure the issuance and secondary trading mechanisms in compliance with local laws.

Determine how tokenized invoices will be financed and settled. Integrate with DeFi protocols for liquidity or partner with traditional finance institutions for hybrid models. Ensure your platform supports automated settlement via smart contracts to reduce counterparty risk and settlement times. Consider the gas costs and network congestion of your chosen blockchain, opting for L2 solutions or specialized trade finance chains if cost and speed are critical.

Start with a pilot program using a limited set of trusted partners and invoice types. Monitor key metrics such as token liquidity, investor participation, and settlement success rates. Use this data to refine your smart contract logic and operational workflows before scaling to a broader audience. Continuous monitoring allows you to address technical or regulatory issues early, ensuring a smoother full-scale launch.

Implementing this framework ensures that your transition to tokenized trade finance is grounded in operational reality and regulatory compliance, turning market opportunities into sustainable business value.

Watch out for these weak options

Not every tokenized invoice project delivers real liquidity. Some platforms simply wrap existing trade finance instruments in blockchain jargon without solving settlement friction. Before committing capital or operational bandwidth, verify that the infrastructure actually reduces counterparty risk and provides transparent audit trails.

Avoid platforms that promise instant financing but rely on opaque off-chain custodians. True onchain credit requires verifiable identity and real-time data feeds, not just a digital receipt. Look for projects integrating Chainlink or similar oracle networks to ensure invoice validity is cryptographically proven before tokenization occurs.

Also, steer clear of solutions that ignore regulatory compliance. Tokenized receivables often fall under securities or money transmission laws. If a platform cannot clearly articulate its KYC/AML framework or jurisdictional licensing, it poses a significant legal risk that outweighs any potential yield advantages.

Tokenized trade finance invoices: common: what to check next

Before committing capital or infrastructure to onchain credit, teams need clarity on mechanics, risk, and adoption. The following questions address the practical objections that typically delay deployment in trade finance tokenization.

No comments yet. Be the first to share your thoughts!