What Are Tokenized Trade Finance Invoices?

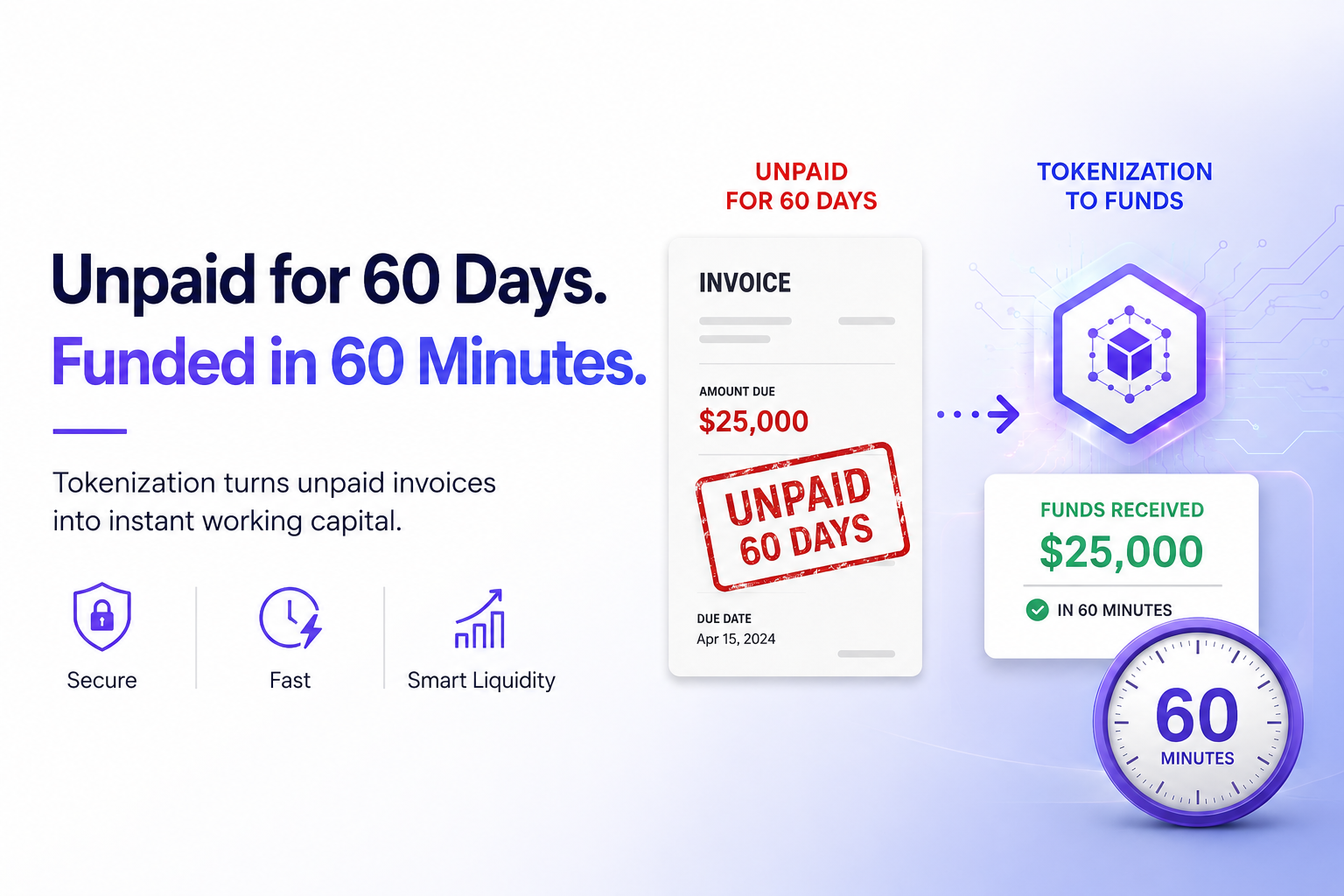

Tokenized trade finance invoices represent a fundamental shift in how businesses manage working capital. At their core, this process involves converting an unpaid invoice—a static document representing a financial claim—into a digital token on a blockchain. This is not merely a digitization effort; it transforms a PDF into a dynamic, programmable asset with verifiable ownership and settlement rules.

Unlike traditional invoice factoring, where a third party buys the receivable at a discount, tokenization allows the underlying claim to be traded or financed directly on a ledger. This distinction matters because it preserves the relationship between the buyer and seller while unlocking liquidity. As noted by Chainlink, invoice tokenization specifically targets the representation of these financial claims as on-chain assets, enabling faster settlement and greater transparency.

The result is a system where trade receivables become liquid instruments. Instead of waiting 30, 60, or 90 days for payment, companies can tokenize the invoice and offer it to investors or lenders in a decentralized market. This approach reduces friction, lowers financing costs, and provides a clear audit trail for all parties involved.

The infrastructure behind onchain receivables

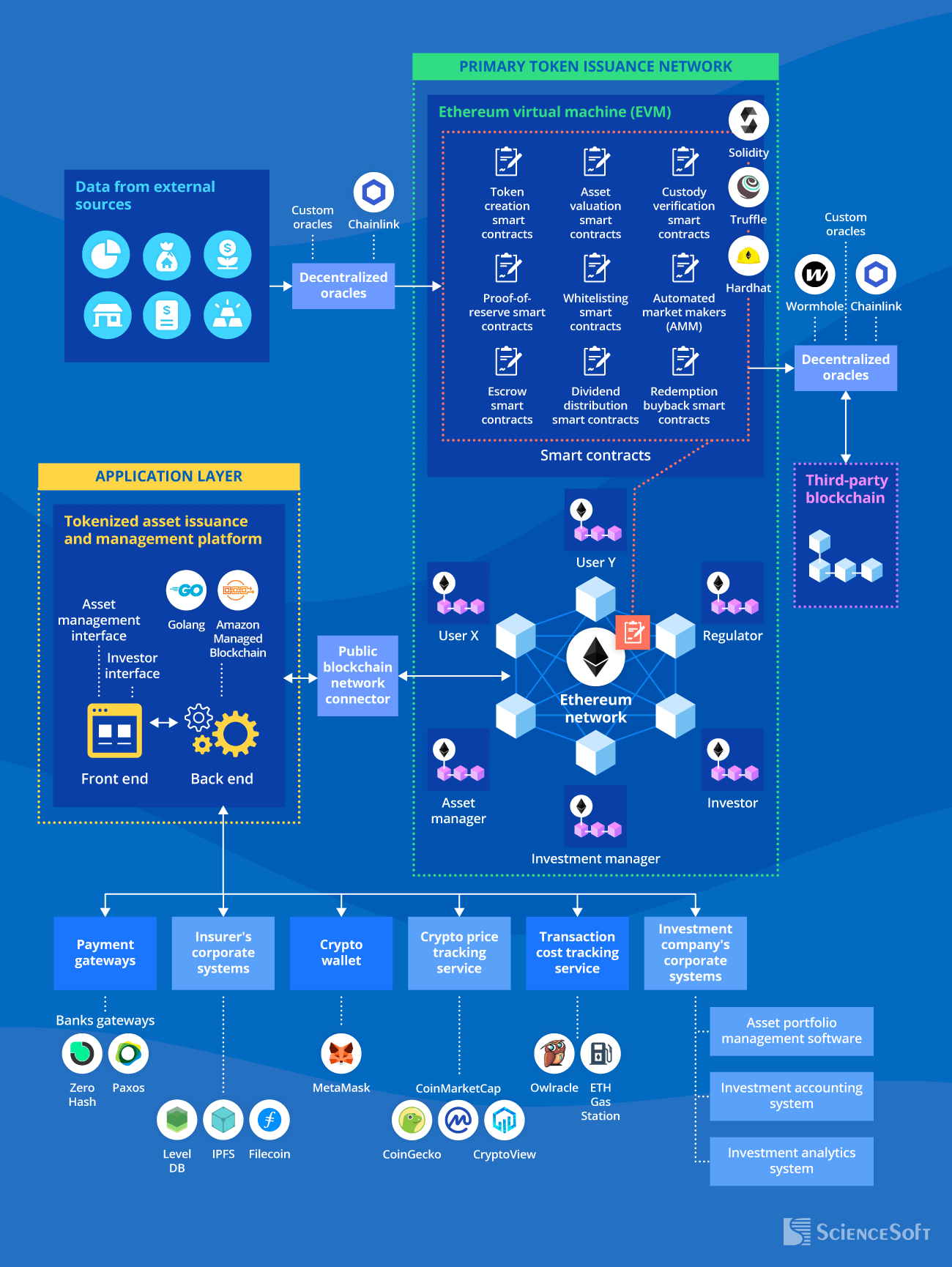

Tokenizing a trade finance invoice isn't just about minting an ERC-20 token; it requires a bridge between the physical world of shipping documents and the digital certainty of the blockchain. Without this infrastructure, an onchain invoice is just a digital promise with no proof of backing. The stack relies on two non-negotiable components: oracle networks for real-world data verification and smart contracts for execution logic.

Bridging the oracle gap

The primary challenge in tokenized trade finance is the "oracle problem": how does a blockchain know if a shipment actually arrived? Blockchain networks are deterministic and isolated; they cannot natively read external emails, customs records, or Bill of Lading statuses. This is where oracle networks like Chainlink come into play. They act as the trusted middleware, aggregating and cryptographically verifying off-chain data before feeding it on-chain.

In a typical workflow, an oracle network pulls data from multiple independent sources—such as logistics providers, banks, and trade platforms—to verify the existence and status of an invoice. This ensures that the tokenized asset accurately reflects the underlying real-world claim. As noted in industry analysis, this data tokenization converts assets like invoices and trade credits into secure, tradable tokens while maintaining interoperability with legacy systems [src-serp-8]. Without this verification layer, the risk of fraudulent tokenization would remain unmanageable.

Smart contracts as the execution engine

Once data is verified, smart contracts take over. These self-executing programs encode the terms of the trade finance agreement, automating payments and transferring ownership of the tokenized invoice. They handle the complex logic of conditional payments—for example, releasing funds to a supplier only when the oracle confirms delivery.

This automation reduces the need for intermediaries, cutting down on settlement times from days to minutes. However, the contracts must be rigorously audited, as they hold real capital. The infrastructure must also support interoperability, allowing the tokenized invoice to move across different blockchain networks if needed, ensuring liquidity isn't trapped in a single silo.

The stability of USDC, often used in these settlements, provides a reliable benchmark for the underlying asset value, ensuring that the tokenized invoice maintains its peg to real-world value during the settlement process.

Deep-tier supply chain liquidity

Use this section to make the Tokenized Trade Finance Invoices decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Market adoption and regulatory hurdles

The shift toward tokenized trade finance invoices is no longer a theoretical exercise; it is an active, albeit uneven, evolution of global supply chain infrastructure. While pilot programs and early adoption are gaining traction among forward-thinking financial institutions, the broader market remains constrained by a complex web of regulatory uncertainty. The core tension lies in reconciling the speed of blockchain settlement with the slow, deliberate pace of international securities law and cross-border compliance frameworks.

Regulatory clarity remains the primary bottleneck. Unlike traditional trade finance, which operates within established legal precedents, tokenized assets often fall into gray areas regarding their classification as securities, commodities, or digital property rights. This ambiguity creates hesitation among institutional investors and traditional banks, who must navigate varying jurisdictional requirements before committing capital. For a comprehensive Tokenized Trade Finance Invoices guide to be effective, it must address these legal complexities, offering a roadmap for compliance rather than just technical implementation.

Cross-border compliance adds another layer of difficulty. Trade finance is inherently international, involving multiple legal systems, banking regulations, and anti-money laundering (AML) protocols. Tokenization promises to streamline this process by creating a single source of truth, but only if all participating jurisdictions recognize the legal validity of the digital token. Until harmonized international standards are established, the market will likely see fragmented adoption, with hubs emerging in regions with progressive regulatory sandboxes, such as Singapore and the EU, while other markets lag behind.

Despite these hurdles, the momentum is undeniable. The potential for increased liquidity, reduced counterparty risk, and enhanced transparency continues to drive interest from major financial players. As regulatory bodies begin to formalize guidelines for digital asset custody and settlement, the path for widespread adoption becomes clearer. The market is currently in a phase of cautious experimentation, where early adopters are testing boundaries while waiting for the legal framework to catch up with the technology.

How to tokenize trade invoices: a practical workflow

Moving from traditional receivables to a Tokenized Trade Finance Invoices guide strategy requires a structured approach. The process involves selecting the right infrastructure, preparing your data, and managing the lifecycle of the digital assets. This workflow outlines the essential steps for businesses ready to modernize their supply chain finance.

Before tokenizing, assess whether a public, permissioned, or hybrid blockchain suits your compliance needs. Look for platforms that offer interoperability with existing ERP systems and support for standardized smart contract templates. The goal is to minimize integration friction while ensuring regulatory adherence.

Tokenization begins with data integrity. Aggregate your outstanding trade receivables and verify that each invoice contains clear payment terms, due dates, and counterparty details. Standardize your data formats to ensure that the digital twins of your invoices are accurate and legally enforceable on-chain.

Once the platform is selected and data is ready, mint the invoices as tokenized assets. This step involves creating a unique digital identifier for each invoice or pool of invoices. Ensure that the smart contracts correctly encode the underlying legal rights and payment obligations.

Expand your network by inviting suppliers to issue invoices directly onto the platform and investors to participate in financing. Use the platform’s native tools to manage KYC/AML checks and access controls. A robust onboarding process ensures that only verified participants can interact with the tokenized assets.

Monitor the tokenized invoices for payment events and automated settlements. When a buyer pays, the smart contract should automatically distribute funds to investors and update the status of the token. This reduces administrative overhead and provides real-time visibility into your cash flow position.

No comments yet. Be the first to share your thoughts!