The tokenized trade finance invoices limits to account for

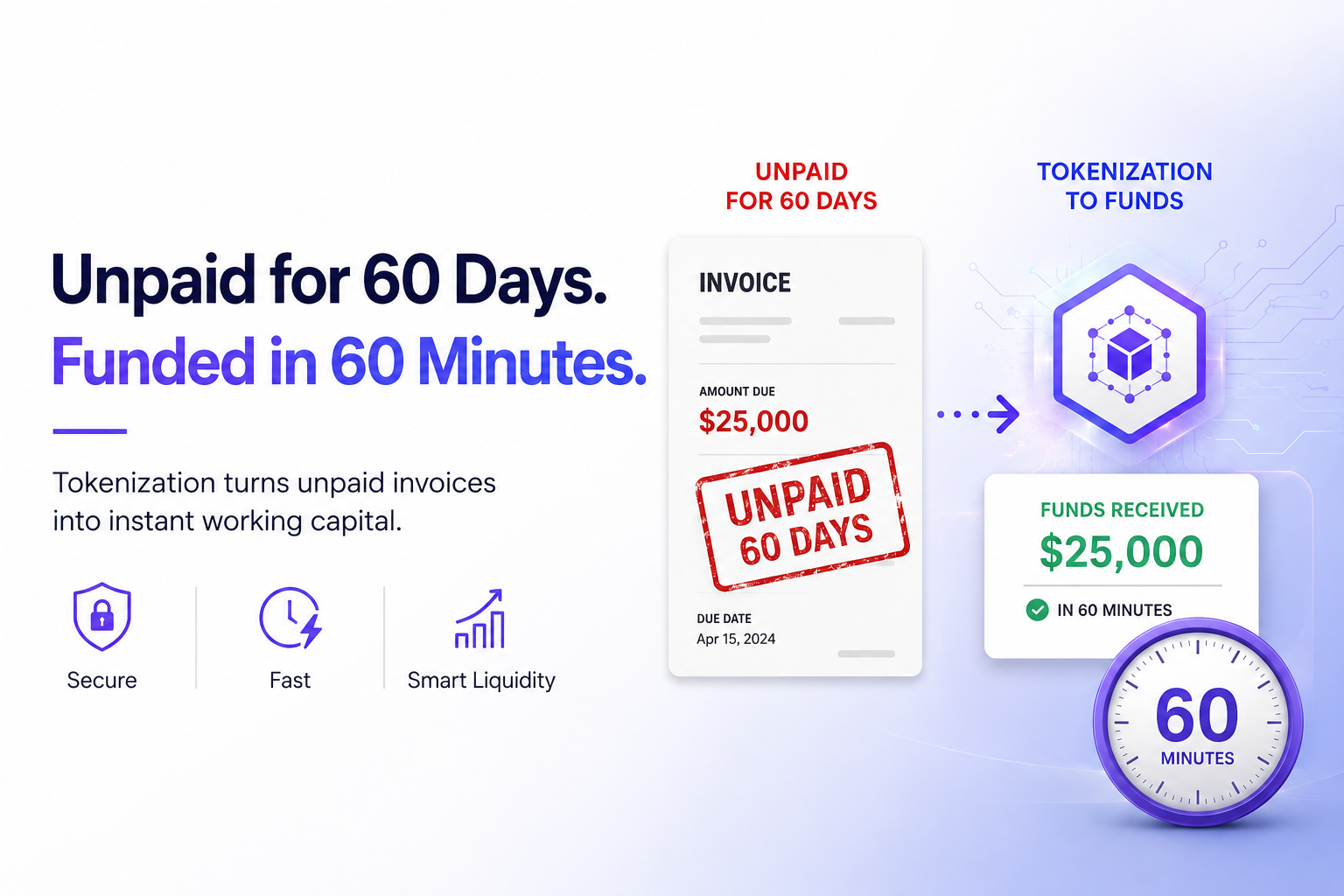

Tokenized trade finance invoices represent a shift from paper-based receivables to digital assets on a blockchain. This process converts an unpaid invoice into a token that can be financed, traded, or settled on-chain. While the technology offers speed and transparency, its adoption is limited by specific structural and regulatory hurdles that define the current market landscape.

The primary constraint lies in the integration of legacy banking infrastructure. Most trade finance transactions still rely on traditional SWIFT networks and off-chain legal frameworks. Bridging these off-chain obligations with on-chain tokens requires robust oracle systems and legal wrappers that are not yet standardized across global jurisdictions. Without this bridge, the token remains a digital representation without enforceable legal claim.

Another significant constraint is the fragmentation of liquidity. Unlike major cryptocurrencies, the market for tokenized trade invoices is niche. Investors require trust in the underlying debtor’s creditworthiness and the authenticity of the trade goods. This necessitates extensive due diligence and KYC/AML checks that can slow down the very efficiency the tokenization promises to deliver. The result is a market that is growing but remains constrained by trust and interoperability challenges rather than technical limitations alone.

Tokenized Trade Finance Invoices: Key Tradeoffs to Evaluate

Before adopting tokenized trade finance invoices, you must weigh the operational benefits against the implementation friction. The shift from paper-based or siloed digital records to on-chain assets offers liquidity, but it introduces new risks regarding legal enforceability, data privacy, and technical integration.

The following comparison breaks down the primary tradeoffs between traditional trade finance methods and tokenized invoice structures. This analysis helps you determine if the infrastructure costs and compliance requirements align with your treasury strategy.

| Factor | Traditional Invoice Finance | Tokenized Invoice | Key Tradeoff |

|---|---|---|---|

| Settlement Speed | 5-10 business days | Minutes to hours | Tokenization accelerates cash flow, reducing working capital gaps. |

| Liquidity Access | Limited to primary supplier | Open to secondary market investors | Broader investor base lowers financing costs but increases complexity. |

| Verification | Manual document review | Smart contract validation | Automation reduces fraud risk but requires robust oracle integration. |

| Legal Framework | Established case law | Evolving regulatory landscape | Enforceability varies by jurisdiction; legal counsel is essential. |

| Data Privacy | Controlled access portals | Public or permissioned ledger | Sensitive trade data must be hashed or stored off-chain to comply with GDPR. |

| Integration Cost | Bank fees and manual labor | API development and blockchain gas | High initial setup cost, offset by long-term efficiency gains. |

The choice between traditional and tokenized models often hinges on volume and counterparty diversity. High-volume supply chains benefit most from the automated verification and secondary market liquidity that tokenization provides. However, for smaller enterprises with stable banking relationships, the regulatory uncertainty and technical overhead may outweigh the speed advantages.

Always consult legal experts in your specific jurisdiction before deploying tokenized invoices. The regulatory landscape for digital assets is still forming, and the enforceability of smart contracts as legal instruments differs significantly across regions. Ensure your infrastructure partners provide clear audit trails that satisfy both accounting standards and local financial regulations.

Choose the next step

Tokenized Trade Finance Invoices works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Spotting weak tokenization options

Not every tokenized invoice platform delivers the liquidity or compliance it promises. Several vendors market their infrastructure as a plug-and-play solution for trade finance, yet they lack the necessary legal wrappers or on-chain settlement rails. Before committing capital or integrating systems, you must audit the underlying structure for these common pitfalls.

Ignoring legal enforceability

Many platforms tokenize invoices without ensuring the smart contract matches the legal assignment of the debt. If the token holder cannot legally enforce payment in a traditional court, the token is merely a speculative derivative, not a financial claim. Always verify that the platform has a signed legal opinion confirming the token represents a valid, enforceable receivable under the jurisdiction of the invoice issuer.

Overlooking settlement finality

A token is only as good as its settlement mechanism. Some solutions promise instant financing but rely on off-bank transfers that can fail or reverse. This creates a gap where the seller is exposed to counterparty risk even after the token is transferred. Look for platforms that integrate directly with central bank payment systems or use atomic settlement protocols to ensure funds and tokens exchange simultaneously.

Misreading the liquidity source

It is common to see platforms claiming deep liquidity pools for invoice tokens, but these pools are often thin or controlled by the platform itself. This creates a false sense of market depth. You must check the actual order book activity and the identity of the liquidity providers. If the only buyers are the platform’s internal treasury, you will likely face wide spreads or inability to exit positions when needed.

Tokenized Trade Finance Invoices: Practical FAQs

Before committing capital or integrating new infrastructure, stakeholders need clear answers on risk, liquidity, and operational reality. Tokenization is not a magic bullet for creditworthiness, but it does change how liquidity moves.

These questions highlight that tokenization is an infrastructure play, not a credit fix. The value lies in efficiency and access to deeper capital pools, not in altering the fundamental risk profile of the trade.

No comments yet. Be the first to share your thoughts!