What tokenized trade finance invoices actually are

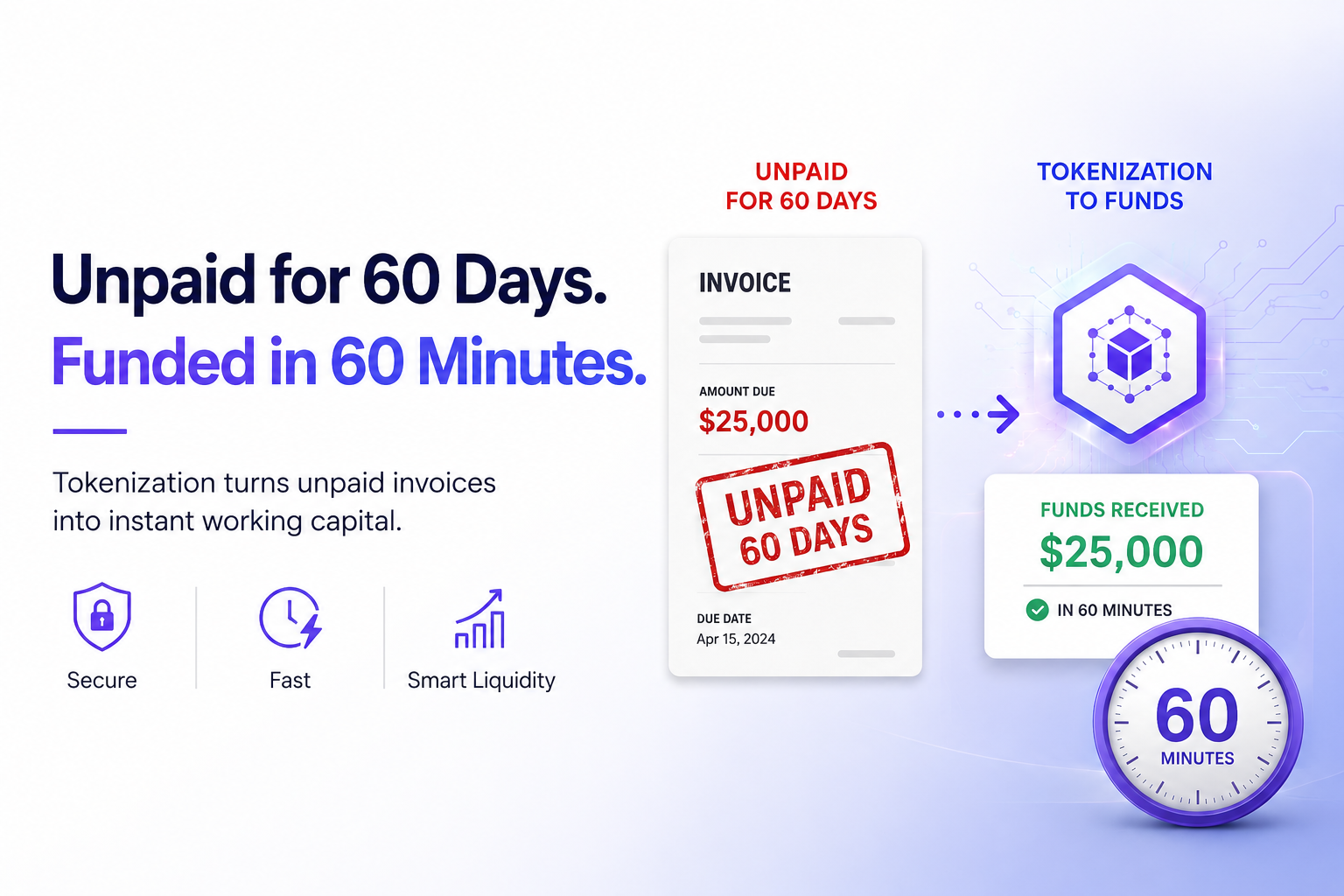

At its core, tokenized trade finance invoice is the process of converting a financial claim—specifically an unpaid invoice—into a digital asset on a blockchain. This isn't just a digitized PDF sitting in a cloud folder. It is a cryptographic representation of the right to receive payment, issued directly on the ledger.

Think of a traditional invoice as a paper promise. In the legacy system, that paper must be physically transferred, manually verified, and often discounted by a factorer who assumes the risk of non-payment. Tokenization replaces that paper promise with a smart contract. The invoice becomes a token that can be held, transferred, or fractionalized, much like a security, but tied to real-world trade receivables.

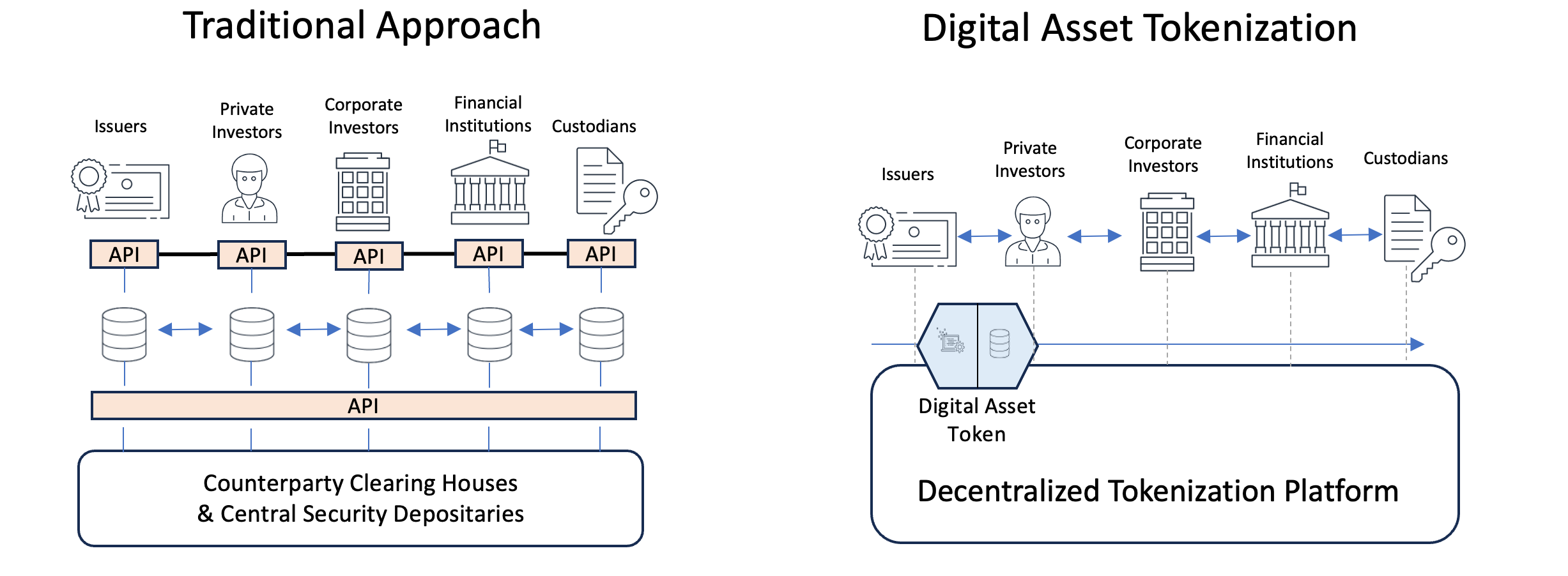

The distinction matters for infrastructure mechanics. In traditional factoring, liquidity is siloed within banks or specialized factoring firms. The process is slow because it relies on trust in the intermediary. With tokenization, the invoice becomes a tradable instrument. Investors or lenders can buy these tokens directly, bypassing the middleman and accessing the underlying receivable.

This shift moves trade finance from a relationship-based model to a data-driven one. The "credit" in credit infrastructure is no longer just about the buyer's reputation; it's about the verifiable, on-chain history of the invoice and its settlement. By putting the claim on-chain, you create a transparent, immutable record that reduces fraud and speeds up the path from invoice creation to cash in hand.

How onchain credit infrastructure works

Tokenized trade finance invoices function by converting traditional unpaid invoices into digital tokens on a blockchain. This process transforms a static financial claim into a liquid asset that can be tracked, owned, and traded programmatically. The infrastructure relies on three core components: the tokenization of the invoice, the verification of off-chain data via oracles, and the automation of repayment through smart contracts.

Invoices as Digital Tokens

The first step is representing the unpaid invoice as a digital token. Instead of a paper document or a PDF in an email, the invoice becomes a unique entry on a blockchain ledger. This token represents the right to receive payment from the buyer. By digitizing the invoice, the asset becomes divisible, allowing multiple investors to fund portions of the invoice rather than requiring a single lender to cover the full amount. This increases liquidity and reduces the barrier to entry for trade finance.

Oracle Verification for Off-Chain Data

Blockchains cannot natively see data from the real world. To ensure the tokenized invoice is valid, oracles bridge the gap between the blockchain and off-chain systems. Oracles pull data from enterprise resource planning (ERP) systems, shipping logs, and banking records to verify that the goods were delivered and the invoice is legitimate. This verification is critical; it ensures that the token represents a genuine financial claim and not a fraudulent entry. Without this oracle layer, the token would lack the trust necessary for financial transactions.

Smart Contracts Automate Repayment

Once the invoice is tokenized and verified, smart contracts manage the lifecycle of the loan. These self-executing contracts encode the terms of the agreement, including the repayment date, interest rate, and payment instructions. When the buyer pays the invoice, the smart contract automatically distributes the funds to the token holders and updates the ledger. This automation removes the need for manual reconciliation, reduces administrative costs, and accelerates the settlement process. The entire workflow—from invoice creation to repayment—can occur in days rather than weeks.

Source: Chainlink - Invoice Tokenization

Why deep-tier suppliers need this liquidity

Most supply chain finance programs stop at tier one. A manufacturer might have a strong credit rating and easy access to cheap capital, but that advantage rarely trickles down. Two or three steps removed, the small parts manufacturer or logistics provider faces a different reality. They lack the balance sheet strength to borrow cheaply, yet they still face the same rigid payment terms as their larger partners.

This creates a working capital gap. These deep-tier suppliers must front the cost of materials and labor for months before seeing a dime from the end buyer. Without tokenization, they are forced to rely on expensive factoring services or traditional bank loans with high interest rates and slow turnaround times. The result is a fragile ecosystem where cash flow constraints stifle growth or force smaller players out of business.

Tokenized trade finance invoices change this dynamic by turning receivables into liquid, tradable assets. Instead of waiting for a net-90 payment, a deep-tier supplier can sell their tokenized invoice on an open market to investors seeking yield. This process is often faster and cheaper than traditional factoring because the underlying data is verified on-chain, reducing due diligence friction.

The infrastructure shift allows liquidity to flow directly to where it is needed most. By integrating with legacy systems through interoperable tokens, these smaller suppliers gain access to a broader pool of capital beyond their immediate bank relationships. This democratization of credit is not just a convenience; it is a structural fix for a broken link in global trade finance.

How tokenized invoices differ from traditional factoring

Tokenized trade finance invoices shift the burden from manual paperwork to automated smart contracts. Traditional factoring relies on a network of intermediaries to verify invoices, manage collections, and distribute funds. This process is slow and expensive. Tokenization replaces these manual steps with code, enabling near-instant settlement and broader access to capital.

The table below breaks down the mechanical differences between legacy factoring and onchain invoice tokenization.

| Feature | Traditional Factoring | Tokenized Invoices |

|---|---|---|

| Settlement Speed | 5-10 business days | Minutes to hours |

| Intermediaries | Banks, factors, lawyers | Smart contracts, DEXs |

| Cost Structure | 1.5% - 5% discount rate | Gas fees + small protocol fee |

| Accessibility | Large corporates only | |

| Liquidity | Locked until maturity | Tradeable on secondary markets |

Key risks and security considerations

Tokenized trade finance moves real capital on public ledgers, which means the infrastructure must be bulletproof. The two biggest technical threats are smart contract vulnerabilities and oracle failures. If the code handling the tokenized invoice has a bug, funds can be drained. If the oracle feeding real-world invoice data to the blockchain is compromised, the entire settlement layer collapses.

Regulatory compliance adds another layer of complexity. Unlike traditional trade finance, where jurisdictional rules are somewhat settled, on-chain assets often exist in a gray area regarding securities laws and anti-money laundering (AML) requirements. You need to ensure that the tokenization platform adheres to the specific financial regulations of every jurisdiction involved in the trade loop. This isn't just about code; it's about legal enforceability.

Building a tokenized invoice strategy

Adopting onchain credit infrastructure requires aligning legacy trade workflows with blockchain settlement. This checklist outlines the essential steps for financial institutions and suppliers to implement tokenized trade finance invoices in 2026.

Identify which trade finance instruments—such as accounts receivable or revenue-based financing—are suitable for tokenization. Map the current issuance, verification, and payment processes to pinpoint where blockchain can reduce friction and improve transparency.

Choose a platform that supports interoperable standards and integrates with existing ERP systems. Verify that the provider adheres to relevant regulatory frameworks for digital assets and trade finance, ensuring legal enforceability of tokenized claims.

Implement smart contracts to automate invoice validation and payment triggers. Integrate with trusted data sources to verify the authenticity of trade documents, reducing the risk of fraud and ensuring that tokenized invoices represent real, settled obligations.

Launch a limited pilot with a small group of suppliers and buyers. Test the end-to-end flow from invoice issuance to tokenized settlement, measuring improvements in speed, cost, and liquidity access. Use these results to refine the strategy before broader rollout.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!