What tokenized trade finance invoices infrastructure means

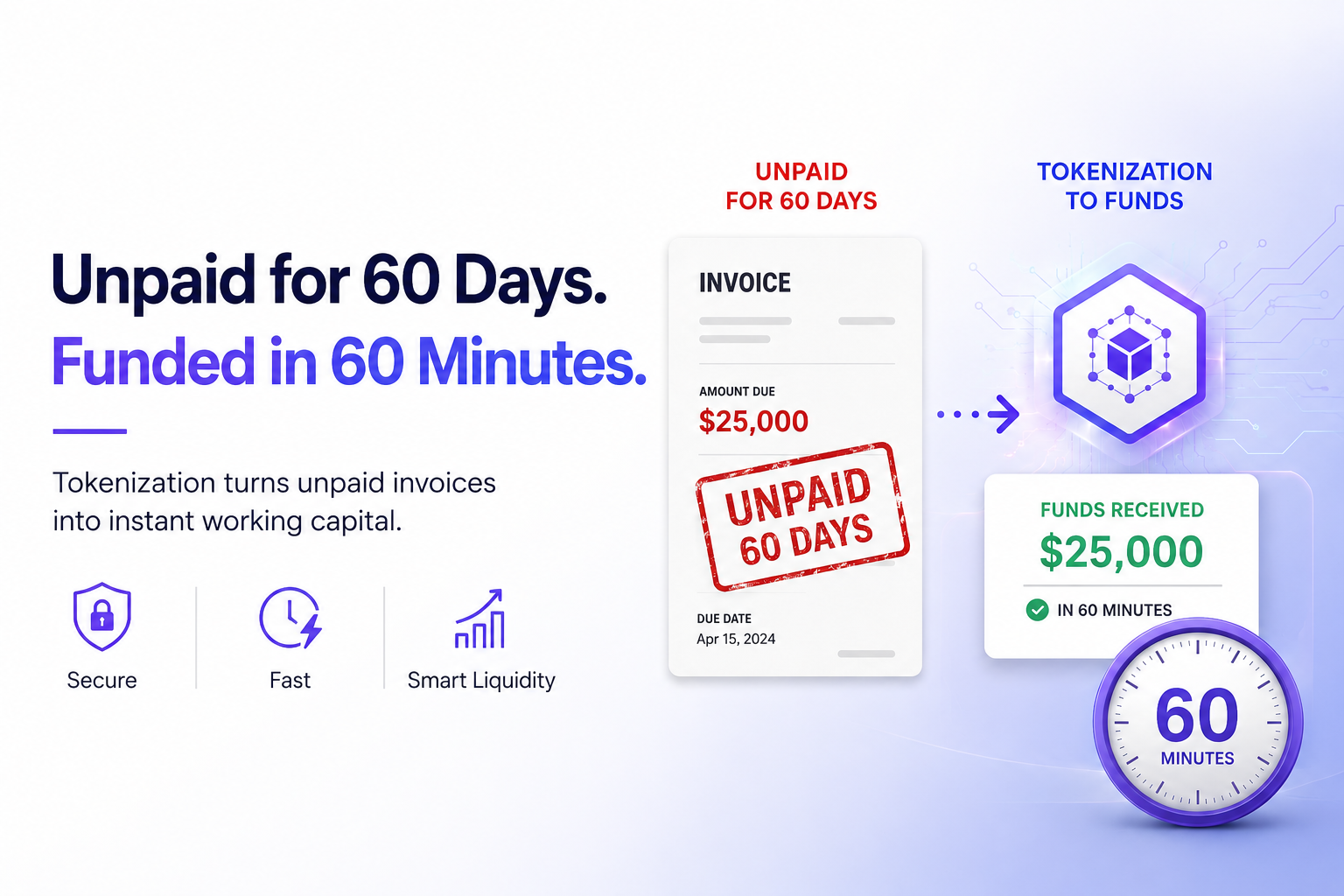

Tokenized trade finance invoices infrastructure is the backbone of modern supply chain liquidity. It converts unpaid commercial invoices into digital tokens on a blockchain, allowing businesses to access working capital instantly rather than waiting 30, 60, or 90 days for payment. This process is distinct from simple digitization. Scanning a PDF invoice does not create liquidity; it only creates a digital record. Tokenization transforms that record into a tradable, collateralizable asset that can move across financial rails.

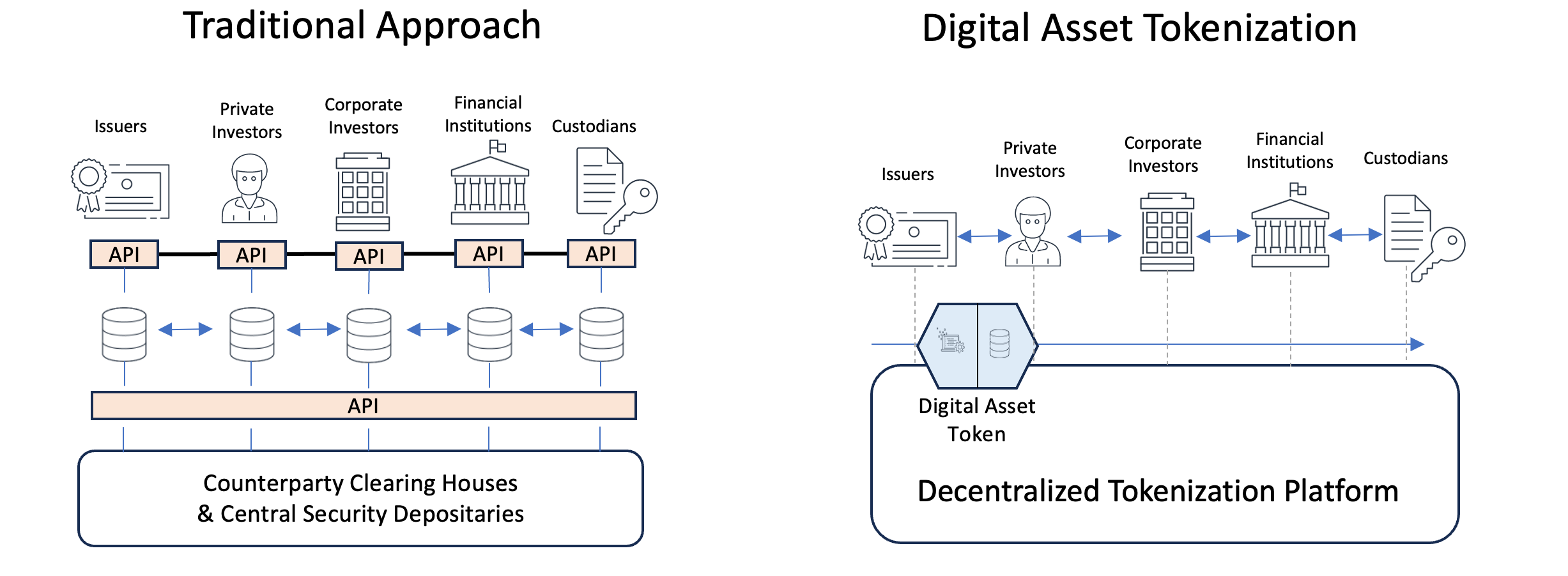

At its core, this infrastructure bridges the gap between traditional trade finance and decentralized finance (DeFi). When an invoice is tokenized, the underlying debt obligation is represented by a digital token. These tokens can be sold to investors, used as collateral for loans, or held as a store of value. This fragmentation allows large commercial debts to be broken down into smaller, more accessible units, democratizing access to trade finance liquidity for smaller suppliers who traditionally struggle to secure funding.

The infrastructure relies on smart contracts to automate verification, payment, and settlement. This reduces the reliance on intermediaries like banks and factoring companies, lowering costs and speeding up the process. By anchoring these digital tokens to real-world trade data, the system creates a transparent, immutable ledger of commercial activity. This visibility reduces risk for lenders and investors, making trade finance more efficient and resilient in a globalized economy.

Key platforms shaping the market

The infrastructure for tokenized trade finance is no longer theoretical; it is being built by specialized platforms that bridge traditional receivables with blockchain liquidity. These providers differ significantly in their target audiences, blockchain compatibility, and liquidity access models. Understanding these distinctions is essential for selecting the right infrastructure for specific trade finance needs.

Platform Comparison

The following table compares leading platforms based on their primary focus and technical capabilities. This comparison highlights how different infrastructure providers serve distinct segments of the trade finance ecosystem, from large corporate supply chains to underserved emerging markets.

| Platform | Primary Focus | Blockchain Compatibility | Liquidity Access |

|---|---|---|---|

| Nomyx | Underserved markets & SMEs | Multi-chain | Direct investor funding |

| Spydra | Corporate supply chain | Enterprise-grade DLT | Institutional investors |

| Chainlink | Data oracles & integration | EVM-compatible | Connects to DeFi/CeFi |

| Tradewise | Cross-border trade | Hyperledger Fabric | Banking partners |

Use Cases and Target Markets

Different platforms excel in different areas. Nomyx, for instance, focuses on releasing liquidity for underserved markets, tackling practical financial problems for SMEs that traditional banks often overlook. Their approach allows multiple investors to fund portions of invoices, increasing liquidity for businesses that lack access to conventional credit.

In contrast, platforms like Spydra and Chainlink serve larger enterprises. Spydra’s blockchain-powered tokenization reduces intermediaries, making the process more efficient for high-volume corporate trade. Chainlink’s role is critical as an oracle provider, ensuring that off-chain invoice data is accurately represented on-chain, which is vital for institutional adoption and integration with existing financial systems.

The choice of platform depends on whether the priority is expanding access to capital for smaller businesses or optimizing efficiency for large-scale corporate trade. Each provider offers a unique set of tools and partnerships that cater to these specific needs.

The technical stack behind tokenized trade finance invoices

Building tokenized trade finance invoices requires more than just a blockchain; it demands a coordinated stack of oracles, smart contracts, and settlement layers. The infrastructure must bridge the gap between traditional off-chain trade documents and on-chain digital assets, ensuring that the token represents a real, verifiable claim on unpaid invoices.

Oracles and Data Verification

The foundation of any tokenized invoice system is reliable data. Oracles bridge the off-chain world of trade finance with the on-chain world of blockchain. They verify the authenticity of invoices, confirm delivery of goods, and ensure that the underlying debt is valid before minting the token. Without this verification layer, the token is just a digital promise with no real-world backing.

Smart Contracts for Automation

Smart contracts automate the lifecycle of the tokenized invoice. They handle the minting process, manage ownership transfers, and execute payments when conditions are met. This automation reduces the need for intermediaries, lowering costs and speeding up settlement. The contracts must be secure and audited to prevent exploits, especially when handling high-value trade finance instruments.

Settlement Layers and CBDCs

Settlement is where the value is realized. Tokenized invoices can be settled using various methods, including traditional fiat or Central Bank Digital Currencies (CBDCs). CBDCs offer a significant advantage by enabling near-instant, final settlement in a digital form, reducing counterparty risk and operational friction. The choice of settlement layer impacts the speed, cost, and regulatory compliance of the entire system.

Key Components Checklist

Launching a tokenized invoice program requires careful attention to these essential components:

- Oracle Network: Reliable data feeds for invoice verification and trade event confirmation.

- Smart Contract Platform: A secure, audited blockchain environment for token issuance and management.

- Settlement Mechanism: A robust system for final payment, potentially leveraging CBDCs for efficiency.

- Compliance Layer: Tools for KYC/AML checks and regulatory reporting integrated into the workflow.

Why businesses are adopting tokenized trade finance

The shift toward tokenized trade finance infrastructure is driven by three practical advantages: immediate liquidity, fewer intermediaries, and broader access to capital. For businesses managing trade receivables, the traditional model often means waiting weeks for settlement while paying fees to multiple banks and factoring agents. Tokenization changes that dynamic by converting invoices into digital tokens that can be traded or financed in near real-time.

Liquidity and reduced friction

Tokenized trade assets allow multiple investors to fund portions of invoices or trade receivables, significantly increasing liquidity [src-serp-3]. Instead of relying on a single bank’s balance sheet, companies can tap into a decentralized pool of capital. This reduces the time it takes to convert receivables into cash, which is critical for maintaining operational flow in global trade.

Lower costs through disintermediation

By reducing the number of intermediaries, tokenization cuts down on administrative overhead and transaction fees. Each traditional layer—correspondent banks, clearinghouses, and factoring firms—adds cost and delay. A tokenized infrastructure streamlines this process, allowing buyers and sellers to settle directly or through smart contracts that automate compliance and payment triggers.

Access to new capital sources

Tokenization facilitates the securitization of trade finance instruments, opening the door to institutional and retail investors who previously had no access to this asset class [src-serp-4]. This democratization of finance means businesses are no longer limited to traditional banking relationships. They can now raise working capital from a global network of investors seeking yield from tangible trade flows.

Risks and regulatory considerations

Tokenized trade finance infrastructure sits at the intersection of traditional credit risk and emerging technology liability. While the promise of liquidity is real, the underlying mechanics introduce distinct vulnerabilities that traditional trade finance did not face. The market is currently navigating a complex web of regulatory uncertainty, where the classification of tokens—whether as securities, commodities, or utility instruments—varies significantly across jurisdictions. This fragmentation creates compliance overhead that can stifle cross-border scalability.

Smart contract risk remains a primary technical concern. Unlike traditional paper-based or even centralized digital ledgers, blockchain-based systems rely on immutable code. A vulnerability in the smart contract governing the tokenized invoice can lead to irreversible loss of funds. In addition, the oracle problem—ensuring that the on-chain token accurately reflects the off-chain reality of the underlying invoice—requires robust, trusted data feeds. If the data source is compromised or manipulated, the token becomes worthless regardless of the underlying asset's validity.

Counterparty default risk has not disappeared; it has merely shifted form. In tokenized systems, the risk extends beyond the original debtor to include the platform operators, custodians, and liquidity providers. If a central entity managing the tokenization layer fails, the liquidity for these illiquid assets can vanish overnight. Investors must scrutinize the legal structure of the special purpose vehicle (SPV) holding the underlying receivables to ensure true bankruptcy remoteness. Without clear legal recourse, tokenization offers liquidity without the security of traditional finance.

Cross-border tokenized trade finance faces conflicting regulatory regimes. A token compliant in one jurisdiction may be classified as an unregistered security in another, creating legal bottlenecks for global trade flows.

Frequently asked: what to check next

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!