Tokenized trade finance invoices: what they are and why they matter

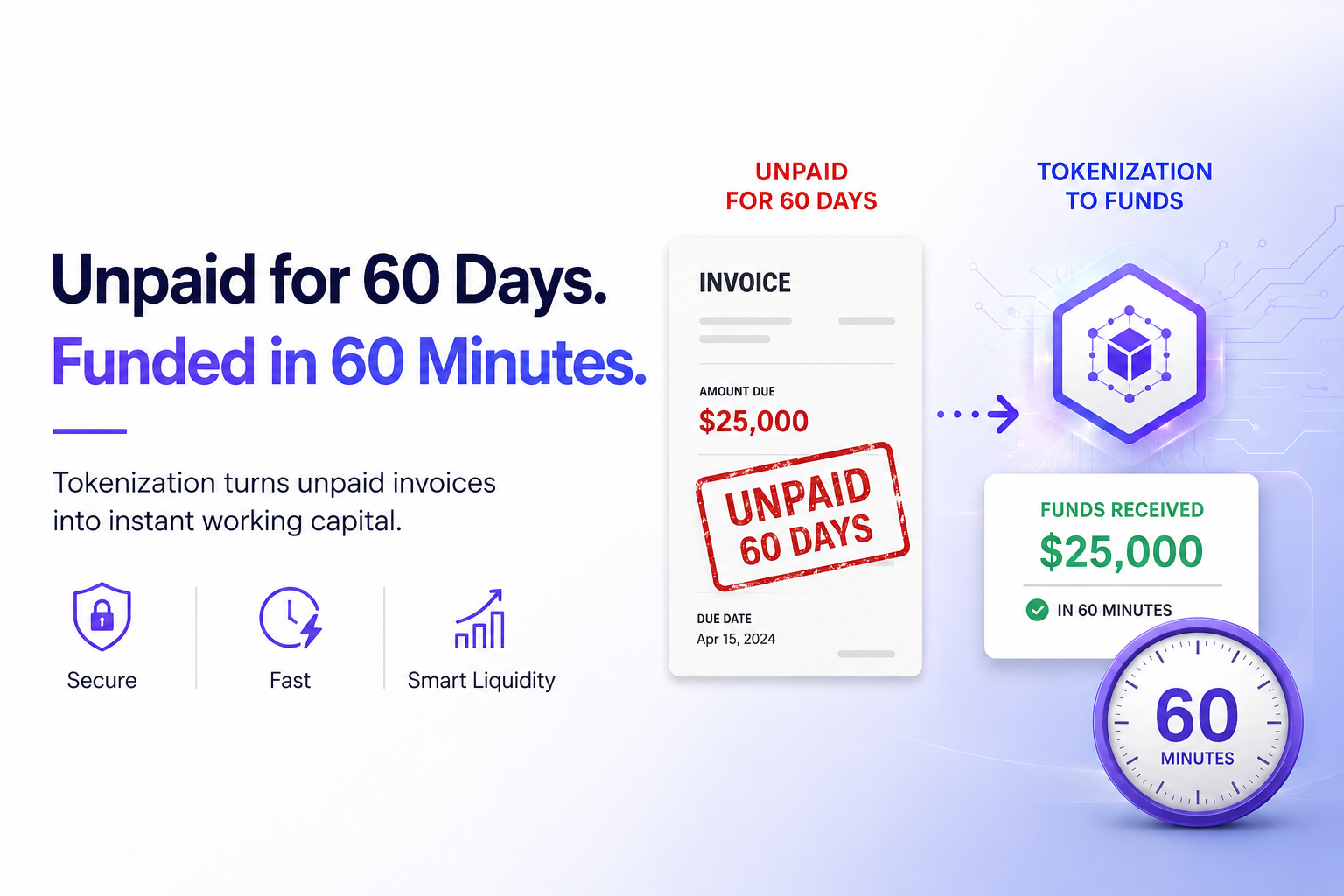

Tokenized trade finance invoices represent unpaid financial claims as digital assets on a blockchain. This process converts traditional receivables into onchain instruments that can be financed, traded, or settled transparently. By moving invoices from static PDFs or legacy ERP systems to a distributed ledger, companies unlock liquidity that was previously locked in long payment cycles.

The core value proposition lies in transparency and speed. When an invoice is tokenized, its status, ownership, and payment terms are recorded immutably. This reduces the friction of verification for lenders and investors, who can audit the asset in real time rather than waiting for manual document checks. For small and medium enterprises, this means faster access to working capital without the heavy overhead of traditional factoring.

However, the infrastructure is still maturing. While the technology promises efficiency, successful implementation requires robust oracle networks to bridge offchain invoice data with onchain truth. Without reliable data feeds, the tokenized asset lacks the credibility needed for institutional adoption. The market is currently focused on standardizing these data connections to ensure that the token accurately reflects the underlying commercial reality.

Tokenized trade finance invoices choices that change the plan

Tokenizing trade finance invoices shifts credit risk and liquidity from traditional banking ledgers to onchain infrastructure. This transition offers speed and transparency but introduces new technical and regulatory complexities. Before committing capital or integrating tokenized receivables, evaluate the following structural factors.

Settlement Speed and Finality

Onchain settlement occurs in minutes or seconds, compared to the 2-5 day cycles typical of traditional trade finance. This acceleration improves working capital turnover for suppliers. However, speed depends on the underlying blockchain’s consensus mechanism. Proof-of-work chains may lag, while proof-of-stake networks like Ethereum or Solana offer near-instant finality. Ensure your platform selects a chain with sufficient throughput to handle high-volume invoice batches without congested fees.

Regulatory Compliance and Jurisdiction

Tokenized invoices are digital representations of legal claims. Their enforceability varies by jurisdiction. Platforms must navigate anti-money laundering (AML) and know-your-customer (KYC) requirements across borders. Some regions treat tokens as securities, while others classify them as utility assets. Non-compliance can freeze assets or invalidate the token’s legal standing. Prioritize platforms that embed compliance checks at the smart contract level and operate within clear regulatory frameworks.

Liquidity and Secondary Market Depth

The value of a tokenized invoice lies in its tradability. Unlike traditional factoring, where liquidity is limited to a few banks, onchain markets can aggregate global investors. However, liquidity is not guaranteed. Thinly traded tokens may suffer from high slippage or inability to exit positions. Evaluate the platform’s investor base and order book depth. A robust secondary market ensures you can convert invoices to cash when needed, rather than holding them to maturity.

Counterparty and Smart Contract Risk

Traditional trade finance relies on bank guarantees and insurance. Onchain, risk shifts to smart contract code and oracle reliability. Bugs in the tokenization contract can lead to permanent loss of funds. Oracles that feed invoice data to the chain must be tamper-proof. If the oracle provides false data, the token’s value becomes detached from the underlying asset. Choose platforms with audited code, insurance funds, and decentralized oracle networks to mitigate these risks.

| Factor | Traditional | Onchain | Risk |

|---|---|---|---|

| Settlement Time | 2-5 days | Minutes | Low |

| Liquidity Source | Banks/Factors | Global Investors | Medium |

| Regulatory Clarity | High | Variable | High |

| Counterparty Risk | Bank Default | Smart Contract Bug | Medium |

Choose the next step

Tokenized Trade Finance Invoices works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Watchouts for Tokenized Trade Finance Invoices

Tokenized trade finance invoices promise instant liquidity, but the infrastructure is still maturing. Several common options in the market fail to deliver on their core value propositions. Buyers need to verify the actual settlement layers and legal enforceability before committing capital.

Over-Reliance on Private Ledger Promises

Many platforms market "on-chain" invoices that are actually settled on private, permissioned ledgers. This creates a liquidity trap where tokens are non-transferable outside a closed ecosystem. True tokenization requires interoperability with public markets or established banking rails. Without this, the asset remains illiquid despite the blockchain label.

Ignoring Legal Wrapper Complexity

Tokenized invoices are not simple debt instruments; they are complex legal wrappers. A common mistake is assuming the smart contract alone defines ownership. In reality, the enforceability depends on the underlying jurisdiction and the legal entity holding the receivable. If the legal wrapper is weak, the token is just a digital IOU with no recourse in case of default.

Underestimating Oracle Risks

Invoice tokenization relies heavily on oracles to verify payment status and invoice authenticity. If the oracle feed is delayed or manipulated, the token price decouples from the underlying asset. Unlike Bitcoin, where price is consensus-driven, trade finance tokens depend on external data accuracy. A single point of failure in the oracle can freeze the entire secondary market for that invoice batch.

Tokenized trade finance invoices: common: what to check next

Tokenized trade finance invoices represent unpaid financial claims as digital assets on a blockchain. While this infrastructure promises faster settlement and lower financing costs, it introduces specific operational and technical hurdles that buyers must evaluate before adoption.

The following questions address the most practical objections regarding risk, liquidity, and technical integration in 2026.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!