What tokenized trade finance invoices actually are

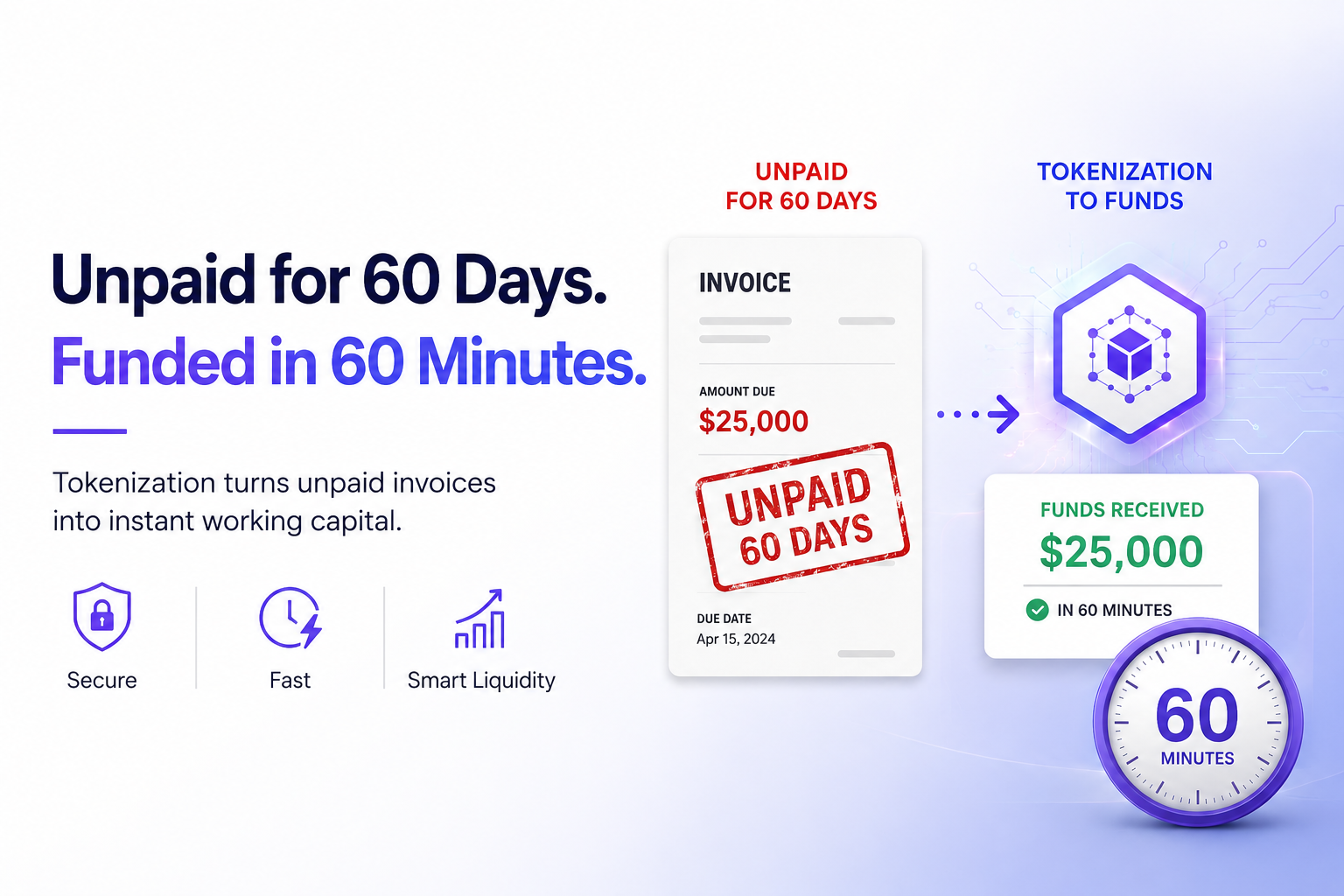

Tokenized trade finance invoices are digital representations of unpaid commercial invoices issued on a blockchain. Rather than relying on paper documents or isolated digital records, these tokens represent a financial claim—a specific dollar amount owed by a buyer to a seller—that can be tracked, transferred, and settled on-chain.

This process converts illiquid trade receivables into tradable digital assets. By anchoring the invoice’s value and payment terms to a smart contract, the asset becomes more than just a record of debt; it becomes a transferable instrument that can be financed, sold, or used as collateral with greater transparency than traditional methods.

The primary difference between tokenized invoices and traditional factoring lies in liquidity and accessibility. In standard factoring, a business sells its invoice to a single financial institution at a discount, often facing lengthy verification processes and limited funding capacity. Tokenization allows these invoices to be broken down or pooled, enabling multiple investors or lenders to participate in financing the debt. This creates a more dynamic market where capital can flow to supply chain participants who might otherwise be excluded from traditional banking channels.

Ultimately, tokenized invoices serve as the bridge between legacy trade finance infrastructure and modern blockchain capabilities. They preserve the legal and financial integrity of the original transaction while unlocking the efficiency, speed, and programmability that digital ledgers provide.

Building the technical stack

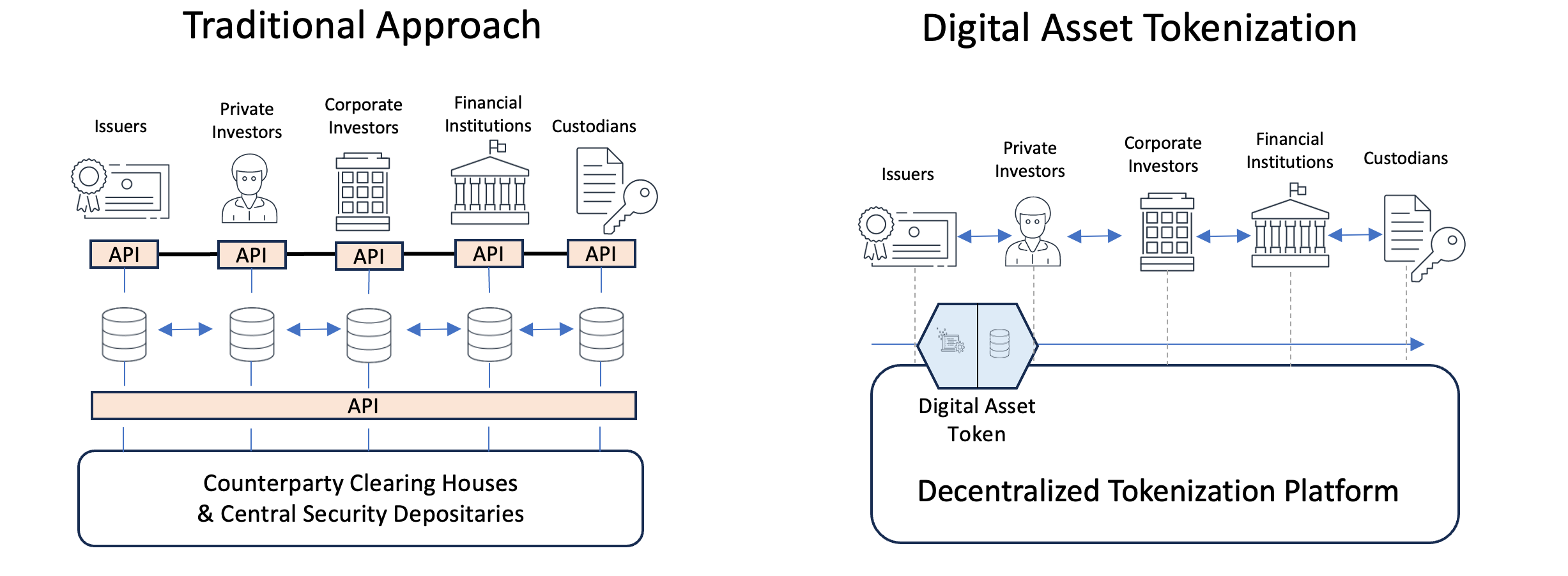

Tokenizing an invoice requires more than just a blockchain; it demands a cohesive infrastructure that bridges the gap between traditional banking ledgers and decentralized networks. The core stack consists of three interconnected layers: the tokenization engine, the legal wrapper, and the oracle network. Each layer serves a distinct purpose in ensuring the digital asset is both technically secure and legally enforceable.

The tokenization engine

At the foundation lies the tokenization engine, which converts physical invoices into digital tokens on a blockchain. This process involves creating a smart contract that represents the invoice's value, payment terms, and maturity date. According to research from the University of Surrey, data tokenization must seamlessly integrate with legacy systems, allowing banks to interact with blockchain-based assets without overhauling their existing infrastructure. The engine typically utilizes permissioned blockchains or private ledgers to maintain privacy while ensuring immutability.

Legal wrappers and compliance

A token is only as valuable as the legal framework supporting it. The legal wrapper defines the rights attached to the token, including who holds the claim to the underlying debt and how disputes are resolved. This layer ensures that the digital representation aligns with jurisdictional contract laws, effectively making the token a legally binding instrument. Without this wrapper, the token remains a speculative asset rather than a trade finance tool.

Oracle integration for real-world data

Oracles act as the bridge between the blockchain and off-chain data, providing real-time updates on invoice status, payment confirmations, and credit risk. Chainlink highlights that tokenized receivables rely on these oracles to unlock liquidity by verifying the authenticity of the underlying debt. By feeding accurate, tamper-proof data into the smart contract, oracles ensure that the token's value reflects the current state of the invoice, reducing counterparty risk.

Liquidity strategies for tokenized invoices

Tokenized invoices transform static receivables into liquid assets by enabling their fragmentation and trading on secondary markets. This process allows businesses to access working capital faster and at lower costs than traditional factoring, while offering investors new yield opportunities backed by real trade flows. The infrastructure supports both institutional and retail participation, creating a deeper pool of capital that responds more efficiently to market demands.

Secondary markets and securitization

The core value of tokenization lies in its ability to facilitate secondary trading. Unlike traditional invoices, which are often held to maturity, tokenized invoices can be bought and sold in real-time. This liquidity is enhanced through securitization, where pools of invoices are bundled into tradeable securities. Research indicates that this approach significantly improves access to deep-tier supply chain finance, allowing smaller suppliers to tap into broader capital markets.

Institutional vs. retail capital

Institutional investors bring scale and stability, often seeking large-volume, low-risk exposure to trade finance. Retail investors, meanwhile, offer diversification and smaller ticket sizes, increasing the overall liquidity of the market. The oncredit ecosystem bridges these two groups, providing transparent, onchain data that reduces due diligence costs and builds trust. This hybrid model ensures that liquidity is not concentrated in a few hands but distributed across a wider network of participants.

| Feature | Traditional Invoice Factoring | Tokenized Onchain Alternatives |

|---|---|---|

| Settlement Speed | 3-10 business days | Minutes to hours |

| Accessible Capital | Large enterprises only | SMEs and deep-tier suppliers |

| Transparency | Limited, private ledgers | Real-time onchain verification |

| Cost Structure | High fees, interest spreads | Lower fees, algorithmic pricing |

| Liquidity | Illiquid, held to maturity | Tradeable on secondary markets |

Managing onchain credit risk

Tokenized invoices move trade finance from opaque ledgers to transparent, programmable assets. This shift doesn't eliminate credit risk, but it changes how the market measures and mitigates it. Instead of relying on delayed bank confirmations, onchain systems use real-time data and automated compliance to reduce default, fraud, and counterparty exposure.

The most significant advantage is visibility. When an invoice is tokenized, its status—issued, accepted, discounted, or paid—is recorded on a shared ledger. This transparency allows lenders to assess the health of the underlying trade in real time. According to the International Trade Administration, clear visibility into trade finance processes is essential for evaluating financing options and ensuring payment security [src-serp-5]. Onchain infrastructure operationalizes this principle by making every step of the invoice lifecycle auditable.

Smart contracts further reduce risk by automating compliance and payment execution. Funds can be released only when predefined conditions are met, such as the arrival of goods confirmed by a digital bill of lading. This removes the possibility of manual intervention or fraudulent documentation altering the payment terms. By automating these checks, onchain systems minimize the window for fraud and ensure that credit is extended only to verified, compliant transactions.

While no system is entirely risk-free, the combination of transparent data and automated enforcement creates a more resilient framework for credit. Lenders can make faster, more informed decisions, and borrowers benefit from reduced friction and lower costs. This approach transforms credit risk from a static, historical assessment into a dynamic, real-time management process.

Implementing a tokenized invoice strategy

Moving from concept to production requires a disciplined approach. The goal is to reduce friction in trade receivables without introducing new operational risks. Start with a controlled pilot, validate the technology, and then expand.

Select a specific subset of trade finance invoices for your initial trial. Narrowing the scope to a single currency, region, or group of trusted counterparties limits exposure. This allows your team to test the tokenization workflow in a controlled environment before committing to broader adoption.

Choose a blockchain platform that meets your institution’s regulatory and performance requirements. Evaluate options based on transaction speed, finality, and compliance features. The infrastructure must support the specific token standards required for your pilot, ensuring interoperability with existing legacy systems.

Connect the tokenization platform to your core banking or trade finance software. This integration is critical for automating the lifecycle of the invoice—from issuance to tokenization, financing, and eventual settlement. Ensure data flows securely between your internal databases and the blockchain network.

Invite a small group of suppliers and financiers to join the pilot. Provide them with the necessary tools and training to interact with the tokenized invoices. Clear communication about the process and benefits is essential to ensure smooth adoption and accurate feedback during this phase.

Track key performance indicators such as processing time, cost savings, and error rates. Gather feedback from all participants to identify bottlenecks or technical issues. This data-driven evaluation will determine whether the pilot was successful and inform the strategy for scaling the tokenized invoice program.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!