What tokenized trade finance invoices actually are

Tokenized trade finance invoices are digital tokens representing the value of an outstanding commercial invoice. This process converts invoice details—such as the amount, due date, and buyer-seller information—into a unique cryptographic asset on a blockchain [src-serp-5]. The result is a digital claim that can be held, transferred, or collateralized, effectively turning static receivables into liquid, tradable assets.

The primary mechanism involves locking the invoice data on-chain, where the token’s value is directly pegged to the invoice’s face value. When a business tokenizes an invoice, it is essentially creating a bridge between traditional trade finance and decentralized liquidity. This allows the invoice to be sold to investors or used to secure immediate funding, bypassing the slower, paper-heavy processes of traditional factoring.

Unlike traditional factoring, where a third-party factor buys the invoice at a discount and manages the collection, tokenization allows the original creditor to retain more control while accessing capital. The tokens can be traded on secondary markets, enabling a more dynamic pricing mechanism based on the perceived risk and creditworthiness of the buyer. This structure unlocks liquidity that was previously locked in long payment terms, offering a faster alternative to conventional supply chain finance.

The Infrastructure Layers for Onchain Credit

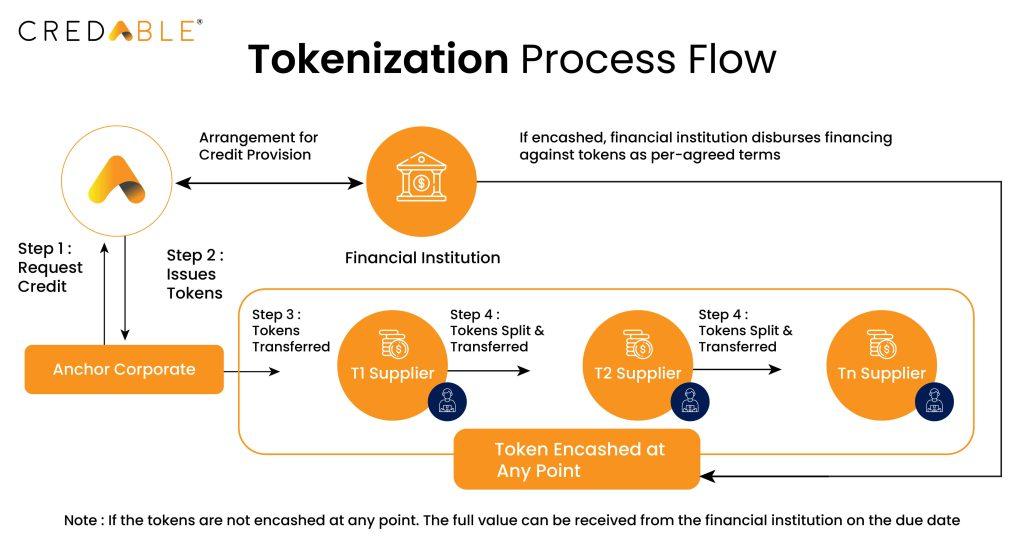

Tokenized trade finance relies on a stack that bridges traditional accounting with blockchain execution. This infrastructure connects real-world invoices to digital rails, allowing trade receivables to be used as collateral. The system depends on three core components: the blockchain network for settlement, oracles for off-chain data verification, and smart contract standards to define asset behavior.

Blockchain Rails

The underlying blockchain acts as the settlement layer. It provides the immutable ledger where tokenized invoices are recorded and transferred. Public networks like Ethereum or specialized L2s are common choices due to their security and liquidity. These rails ensure that ownership records are transparent and tamper-proof, which is essential for financial institutions managing high-value trade assets.

Oracle Feeds for Real-World Data

Smart contracts cannot natively access off-chain information. Oracle feeds, such as those provided by Chainlink, bridge this gap by bringing real-world invoice data on-chain. These oracles verify the status of an invoice—whether it is outstanding, paid, or disputed—and update the blockchain state accordingly. This verification is critical for maintaining the integrity of the tokenized asset, ensuring that the on-chain representation matches the legal reality of the trade.

Smart Contract Standards

To represent trade assets effectively, developers use specific smart contract standards. These standards define how tokens are created, transferred, and managed. Common standards like ERC-3643 or ERC-1400 are often preferred in regulated environments because they support compliance features, such as KYC/AML checks, directly into the token logic. This ensures that only verified participants can trade these tokens, aligning the technical infrastructure with legal requirements.

Key benefits for supply chain participants

Tokenized trade finance invoices shift the structure of working capital from a bilateral constraint to a networked asset. By converting invoices into digital tokens, the system allows buyers, suppliers, and investors to interact with greater speed and transparency than traditional factoring permits. This shift addresses the friction points that historically stalled trade finance, particularly for small and medium-sized enterprises (SMEs) deep in the supply chain.

Faster settlement and liquidity

The most immediate benefit is the acceleration of cash flow. In traditional models, invoice verification and payment can take weeks due to manual reconciliation and intermediary layers. Tokenization automates this process through smart contracts, enabling near-instant settlement once predefined conditions are met. For suppliers, this means working capital is released much faster, reducing the need for expensive short-term borrowing. For buyers, it extends payment terms without punishing their suppliers, as the liquidity is provided by the token market rather than the buyer’s balance sheet.

Fractional ownership and accessibility

Tokenization breaks large invoice values into smaller, tradable units. This fractional ownership model opens trade finance to a broader range of investors who previously lacked the capital to underwrite large commercial invoices. It also allows suppliers to access deep-tier payables finance, reaching suppliers multiple steps removed from the core buyer. Research indicates that this network effect significantly expands the pool of available liquidity, particularly for SMEs that are often excluded from traditional bilateral supply chain finance programs [src-serp-7].

Reduced counterparty risk

The transparency inherent in tokenized ledgers reduces information asymmetry between parties. Investors can verify the authenticity of the invoice and the creditworthiness of the buyer in real time, reducing the risk of fraud or double-spending. This clarity lowers the cost of capital for suppliers and reduces the risk premium investors demand. The system effectively securitizes trade finance instruments, making them more robust and easier to price [src-serp-4].

Traditional Factoring vs. Tokenized Trade Finance

| Feature | Traditional Invoice Factoring | Tokenized Trade Finance |

|---|---|---|

| Settlement Speed | Days to weeks | Near-instant |

| Access to Capital | Limited to top-tier suppliers | Deep-tier SMEs included |

| Transparency | Low (manual processes) | High (real-time ledger) |

| Fractionalization | Not possible | Fully supported |

| Cost of Capital | Higher due to risk premium | Lower due to transparency |

Market strategy and risk considerations

Tokenized trade finance invoices operate in a high-stakes environment where regulatory uncertainty and credit risk assessment define the viability of any platform. Unlike consumer crypto, trade finance involves real-world assets, complex supply chains, and strict compliance requirements. Success here depends less on technological novelty and more on rigorous due diligence and adherence to official standards.

Regulatory clarity and compliance

The regulatory landscape for tokenized invoices remains fragmented across jurisdictions. While some regions are developing clear frameworks, others treat digital trade assets with caution. Platforms must prioritize compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations, which are non-negotiable for institutional adoption. Relying on official sources and legal counsel is essential to navigate these varying requirements.

Credit risk and oracle reliability

Credit risk in tokenized invoices mirrors traditional trade finance but introduces new variables related to smart contract security and data integrity. The reliability of oracles—systems that feed real-world data onto the blockchain—is critical. If an oracle provides inaccurate invoice data, the tokenized asset becomes worthless. Platforms must implement robust oracle solutions and regular smart contract audits to mitigate these risks.

Due diligence checklist

Before engaging with a tokenized invoice platform, conduct thorough due diligence:

- Regulatory Compliance: Verify the platform’s adherence to local and international trade finance regulations.

- Oracle Reliability: Assess the security and accuracy of the oracle systems feeding data to the blockchain.

- Smart Contract Audits: Ensure the platform’s smart contracts have been audited by reputable third-party firms.

- Credit Assessment: Evaluate the creditworthiness of the underlying invoice issuers and buyers.

Market data and trends

Understanding market dynamics is crucial for strategic decision-making. Monitor key indicators such as transaction volumes, adoption rates, and regulatory developments. Use live provider-backed widgets to track real-time market data, ensuring your strategy is based on current and accurate information.

Tokenization Infrastructure and Platforms

The market for tokenizing trade finance invoices is maturing, with specialized platforms emerging to bridge traditional banking systems and distributed ledger technology. These tools handle the complex workflow of converting unpaid receivables into digital assets that can be financed, traded, or settled on-chain.

Providers like Blockchain App Factory offer end-to-end services that transform trade documents, such as invoices and letters of credit, into blockchain tokens. This infrastructure makes it easier for businesses to manage liquidity and access new financing channels without relying solely on traditional bank credit lines [src-serp-2]. Similarly, ONINO focuses on the technical execution of tokenizing trade receivables, allowing companies to unlock value from their supply chain assets by converting them into tradable digital tokens [src-serp-3].

When selecting a platform, look for solutions that prioritize compliance and interoperability. The best tools integrate seamlessly with existing ERP systems while providing the transparency needed for auditors and regulators. As the infrastructure evolves, these platforms are becoming the backbone of modern trade finance, enabling faster settlement and reduced counterparty risk.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!