Defining the tokenized trade finance invoices strategy

The tokenized trade finance invoices strategy moves beyond simple digitization. It is not about replacing paper with PDFs or storing records in a database. Instead, it is about transforming outstanding trade receivables into standardized, tradable digital assets on a blockchain. This shift creates a liquid secondary market for what has historically been an illiquid, opaque asset class.

Traditional trade finance relies on a fragmented chain of banks, suppliers, and buyers. Invoices often sit in limbo, tied up in verification processes and credit checks. Tokenization breaks this bottleneck by converting unpaid claims into on-chain tokens. These tokens can then be financed, traded, or used as collateral across a broader network of participants. The result is a marketplace where liquidity is no longer constrained by individual bank balance sheets.

This approach aligns with the broader institutional push for asset tokenization in financial services. As noted by PwC, tokenization allows institutions to digitally represent asset ownership for both tangible and intangible assets, accelerating adoption in day-to-day operations. For trade finance, this means suppliers can access capital faster, while investors gain exposure to a diversified pool of short-term, real-economy assets.

The infrastructure required to support this strategy involves smart contracts that automate payment terms, verify invoice authenticity, and manage token transfers. By embedding trust into the code, the strategy reduces counterparty risk and operational friction. This is not just a technological upgrade; it is a structural change in how trade credit is priced and distributed globally.

Core Infrastructure for Tokenized Trade Finance Invoices

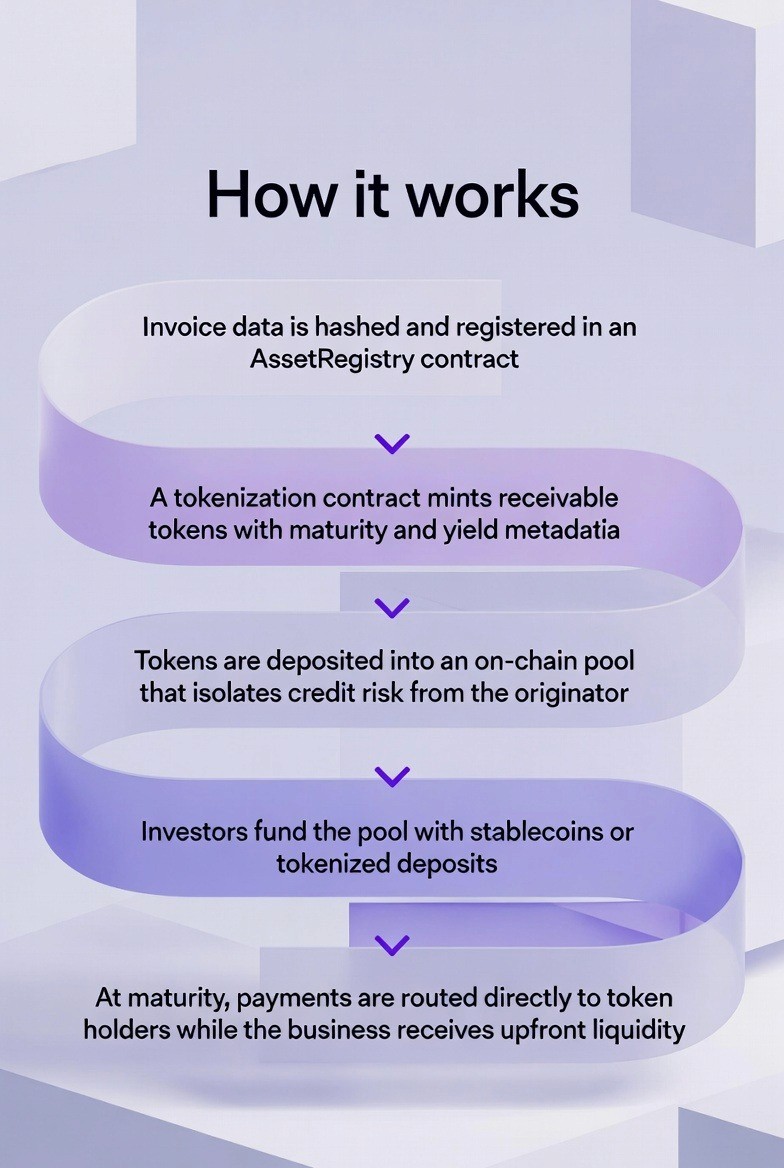

Building a tokenized invoice system requires bridging the gap between traditional trade finance workflows and blockchain infrastructure. The stack rests on three pillars: a suitable blockchain network, reliable oracles to verify off-chain data, and standardized smart contracts to manage issuance. Without this technical foundation, tokenization remains a theoretical exercise rather than a functional financial tool.

Blockchain Selection

The choice of blockchain determines the speed, cost, and regulatory compliance of the tokenized assets. For trade finance, permissioned networks or private layers of public blockchains are often preferred over fully public chains. This approach ensures that sensitive invoice data remains accessible only to authorized parties while still benefiting from cryptographic immutability. Networks like Hyperledger Fabric or enterprise-grade Ethereum implementations provide the necessary control for institutional players who cannot expose their ledgers to the public.

Oracle Integration

Smart contracts cannot natively access real-world data, making oracles the critical link between the invoice and the blockchain. Oracles fetch and verify off-chain information, such as shipping documents, bill of lading status, and payment confirmations from traditional banking systems. Chainlink, for example, provides decentralized oracle networks that can securely transmit this data to the blockchain. This verification process is essential because the value of the tokenized invoice depends entirely on the accuracy of the underlying off-chain assets.

Smart Contract Standards

Once the data is on-chain, smart contracts must manage the lifecycle of the tokenized invoice. These contracts handle issuance, transfer, and redemption, ensuring that the token represents a valid claim on the underlying debt. Standardization is key here; using established token standards like ERC-1400 or ERC-3643 allows for better interoperability with existing financial software and regulatory compliance tools. These standards often include features like transfer restrictions, which are necessary to ensure that only verified participants can hold or trade the invoice tokens.

The shift from traditional factoring to on-chain receivables

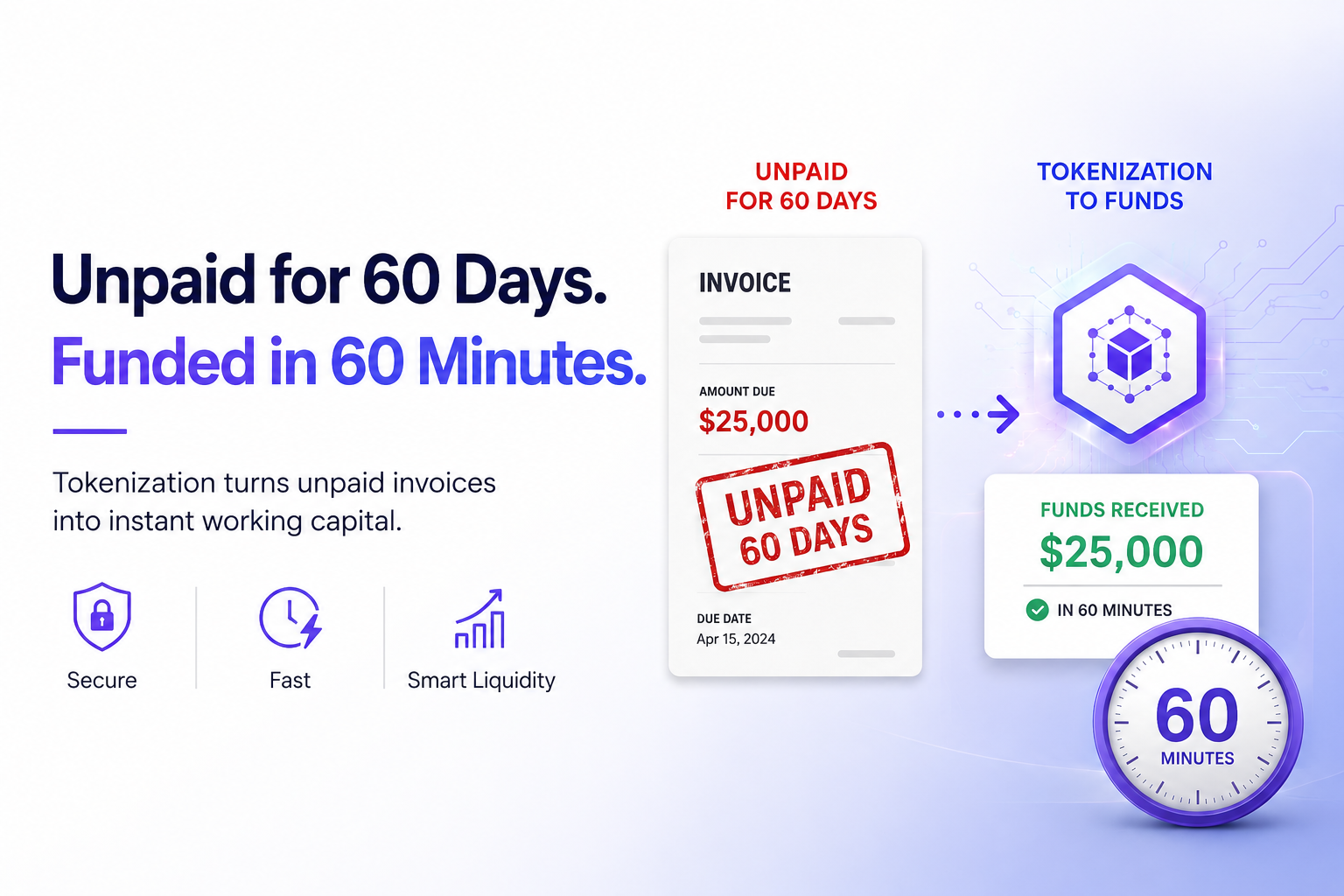

Tokenized trade finance invoices are moving from pilot programs to active market infrastructure. The primary driver is the ability to unlock deep-tier supply chain capital. Traditional factoring models typically stop at Tier 1 suppliers, leaving smaller vendors without access to affordable working cash. Tokenization changes this by making receivables verifiable and instantly tradable across the entire supply network.

The market dynamics are shifting because tokenization transforms invoices into secure, verifiable, and instantly tradable digital assets. This liquidity allows SMEs to access capital previously reserved for large enterprises. According to recent research, this paradigm change is reducing the cost of capital for deep-tier suppliers while increasing transparency for lenders.

To understand the scale of this shift, it helps to compare the operational realities of traditional invoice factoring against tokenized trade finance invoices. The differences in speed, cost, and accessibility are significant.

| Feature | Traditional Factoring | Tokenized Trade Finance |

|---|---|---|

| Cost Structure | High fees (1-3% per month) due to manual verification | Lower fees (0.5-1.5%) via automated smart contracts |

| Processing Speed | 5-10 business days for approval and funding | Near-instant settlement upon invoice verification |

| Accessibility | Limited to Tier 1 suppliers with strong credit | Open to deep-tier suppliers via supply chain finance programs |

| Liquidity | Illiquid until invoice maturity or resale | Tradable on secondary markets for immediate cash |

This table highlights why institutions are adopting tokenization. The reduction in manual verification costs and the increase in liquidity make tokenized trade finance invoices a more efficient infrastructure for modern trade. As regulatory frameworks mature, this model is expected to become the standard for cross-border receivables financing.

Tools and platforms for implementation

Building a tokenized trade finance strategy requires integrating specialized software, blockchain protocols, and service providers. Enterprise-grade solutions focus on converting unpaid claims into digital assets that can be financed or traded on regulated ledgers.

Invoice Tokenization Software

Platforms like ONINO and Yodaplus provide the infrastructure to convert invoice details—such as amount, due date, and buyer information—into digital tokens. These systems handle the initial digitization and ensure the data integrity required for downstream liquidity.

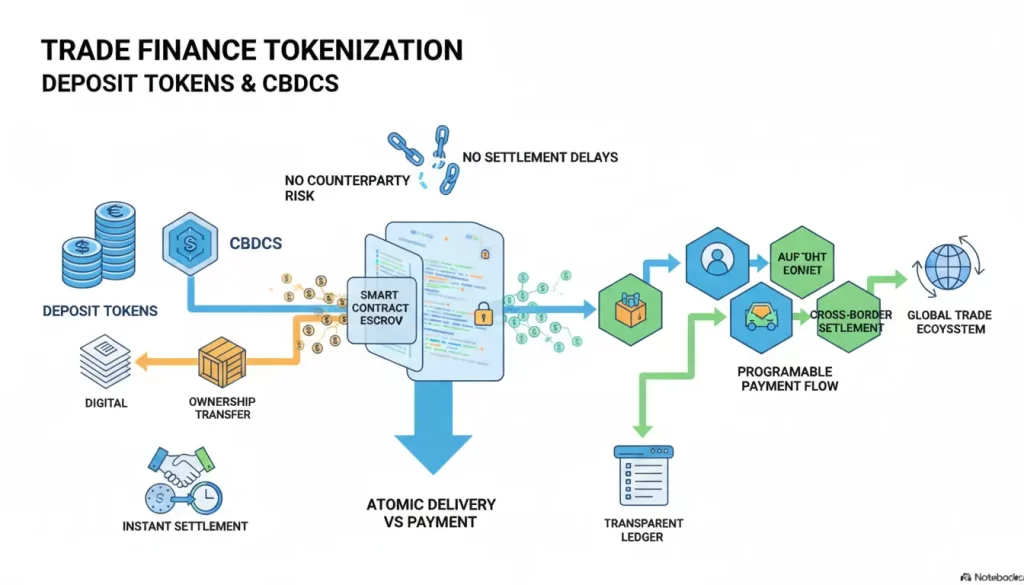

Stablecoin and Liquidity Infrastructure

Tokenized invoices often settle in stablecoins or tokenized treasury bills. Monitoring the liquidity and price stability of these underlying assets is critical for risk management. Financial institutions rely on live data feeds to ensure the tokenized assets maintain their peg and value during the financing process.

Compliance and Settlement Providers

The final layer involves providers that handle legal wrappers, KYC/AML checks, and settlement. These services ensure that the tokenized invoice complies with financial regulations in the jurisdictions of both the supplier and the buyer, bridging the gap between traditional finance and blockchain technology.

Risk Management and Compliance

Tokenized trade finance infrastructure operates in a high-stakes environment where a single smart contract vulnerability or compliance gap can halt liquidity or trigger regulatory penalties. Building this layer requires rigorous technical security, strict adherence to financial regulations, and robust credit risk assessment. The goal is to create a system that is not only fast but also legally defensible and financially sound.

Compliance is the foundation. Tokenized invoices must adhere to existing financial regulations, including anti-money laundering (AML) and know-your-customer (KYC) protocols. Unlike traditional trade finance, where documentation is siloed, tokenization requires a digital identity layer that verifies every participant on-chain. Ensure your infrastructure supports immutable audit trails that satisfy regulators from day one, rather than retrofitting compliance later.

Financial infrastructure demands zero-trust security. Before any tokenized invoice goes live, the underlying smart contracts must undergo multiple independent security audits. Focus on identifying reentrancy vulnerabilities, access control flaws, and oracle manipulation risks. Treat the code as you would a vault: every line of logic must be verified, and every edge case must be stress-tested against malicious actors.

Tokenization reduces risk but does not eliminate it. The primary risk remains the counterparty’s ability to pay. Integrate traditional credit scoring models with on-chain data to assess the financial health of both the supplier and the buyer. This hybrid approach allows for dynamic discount rates based on real-time risk profiles, ensuring that financing remains affordable for low-risk transactions while adequately pricing high-risk ones.

By integrating these three pillars—compliance, security, and risk assessment—you create a resilient infrastructure that can withstand both technical failures and market volatility. This structure transforms tokenized invoices from speculative assets into reliable financial instruments.

Frequently asked questions about tokenization

What is a tokenization strategy?

Tokenization is the process of converting ownership rights to tangible or intangible assets into digital tokens on a blockchain. This strategy allows institutions to represent assets like invoices or trade finance instruments digitally, enabling them to integrate tokenized assets into day-to-day operations and liquidity pools.

How does invoice tokenization work in practice?

Invoice tokenization converts outstanding invoices into digital tokens on a blockchain. These tokens can then be used as collateral for loans or traded in secondary markets. The process relies on smart contracts to automate payments and verify ownership, reducing the administrative burden typically associated with trade finance.

Is tokenization only for large banks?

No. While large institutions lead adoption, the infrastructure is increasingly accessible. Tokenization lowers the barrier to entry for smaller businesses by providing fractional ownership and improved liquidity. As the technology matures, more mid-market players are adopting tokenized trade finance to optimize working capital.

What are the main risks of tokenizing trade finance?

The primary risks involve regulatory compliance and smart contract security. Since tokenized assets are subject to financial regulations, institutions must ensure their blockchain infrastructure meets legal standards. Additionally, technical vulnerabilities in smart contracts can pose significant risks, requiring robust auditing and security protocols.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!