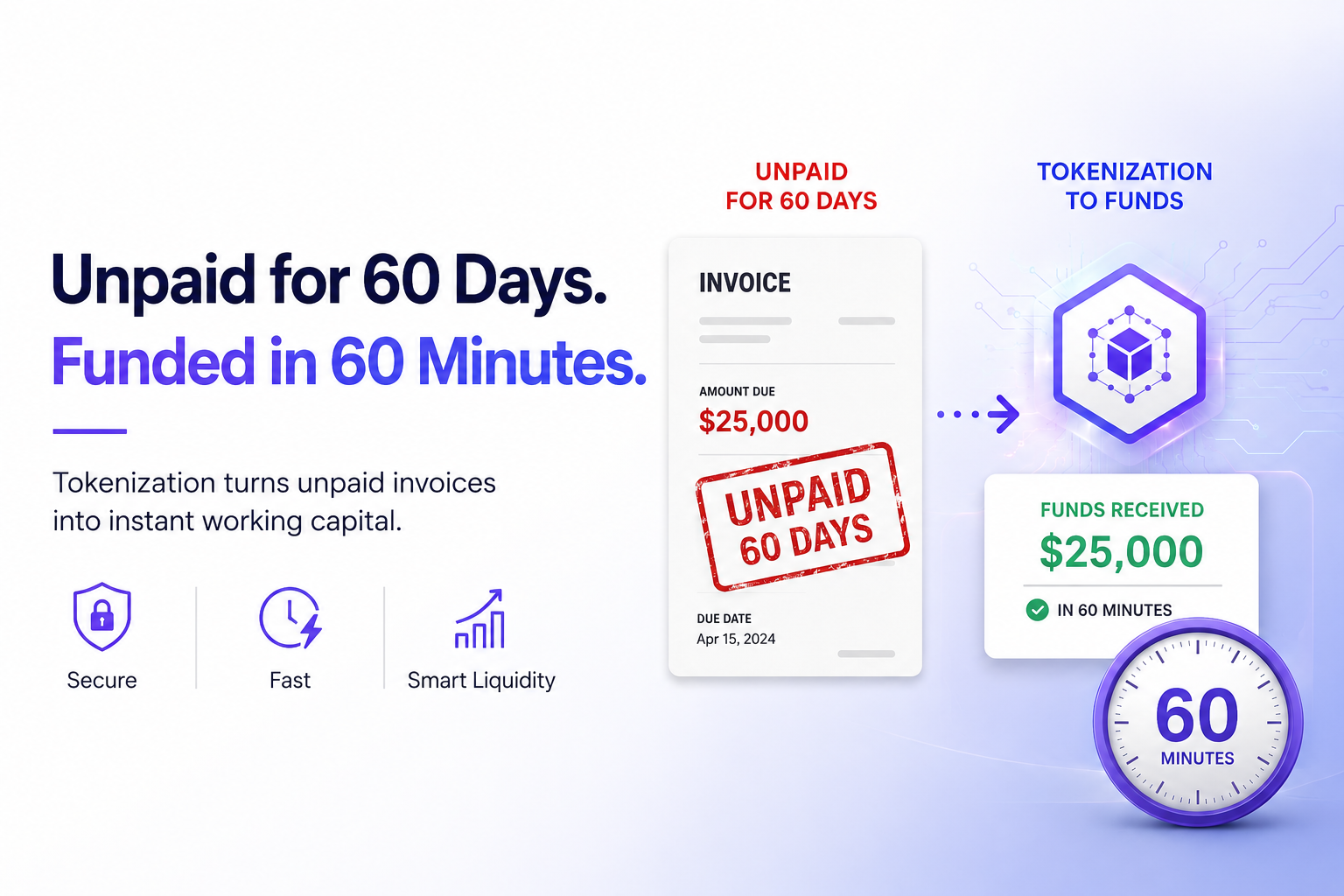

Defining tokenized trade finance invoices

Tokenized trade finance invoices are digital representations of unpaid financial claims, issued as tokens on a blockchain. This process transforms a static invoice into a programmable, transferable onchain asset. Unlike simple digitization, which often involves converting a PDF into a digital file, tokenization embeds the invoice’s terms and ownership rights directly into a smart contract.

This distinction matters for infrastructure and strategy. Traditional factoring relies on off-chain legal agreements and manual verification, creating friction and delays. In contrast, tokenized invoices enable real-time verification of ownership and terms through the blockchain’s immutable ledger. This allows for faster liquidity access and more efficient secondary market trading of trade receivables.

The result is a shift from static, paper-based records to dynamic, onchain financial instruments. This infrastructure supports automated compliance, instant settlement, and greater transparency for all parties involved in the trade finance lifecycle.

The technical stack for onchain credit

Tokenizing an invoice isn't just about putting a PDF on a blockchain. It requires a coordinated stack of oracles, smart contracts, and settlement rails to turn a static financial claim into a liquid, tradable asset. Without this infrastructure, the token remains a digital replica rather than a functional financial instrument.

Oracles: Bridging Off-Chain Reality

The most critical layer is the oracle network. An invoice exists in the real world, governed by legal contracts and banking systems that blockchains cannot natively read. Oracles act as the bridge, verifying that the invoice is genuine, that the goods were delivered, and that the payment terms are met. Chainlink and similar networks provide the decentralized data feeds necessary to attest to these off-chain events, ensuring that the onchain token reflects the true state of the debt.

Smart Contracts: Automating Rights and Transfers

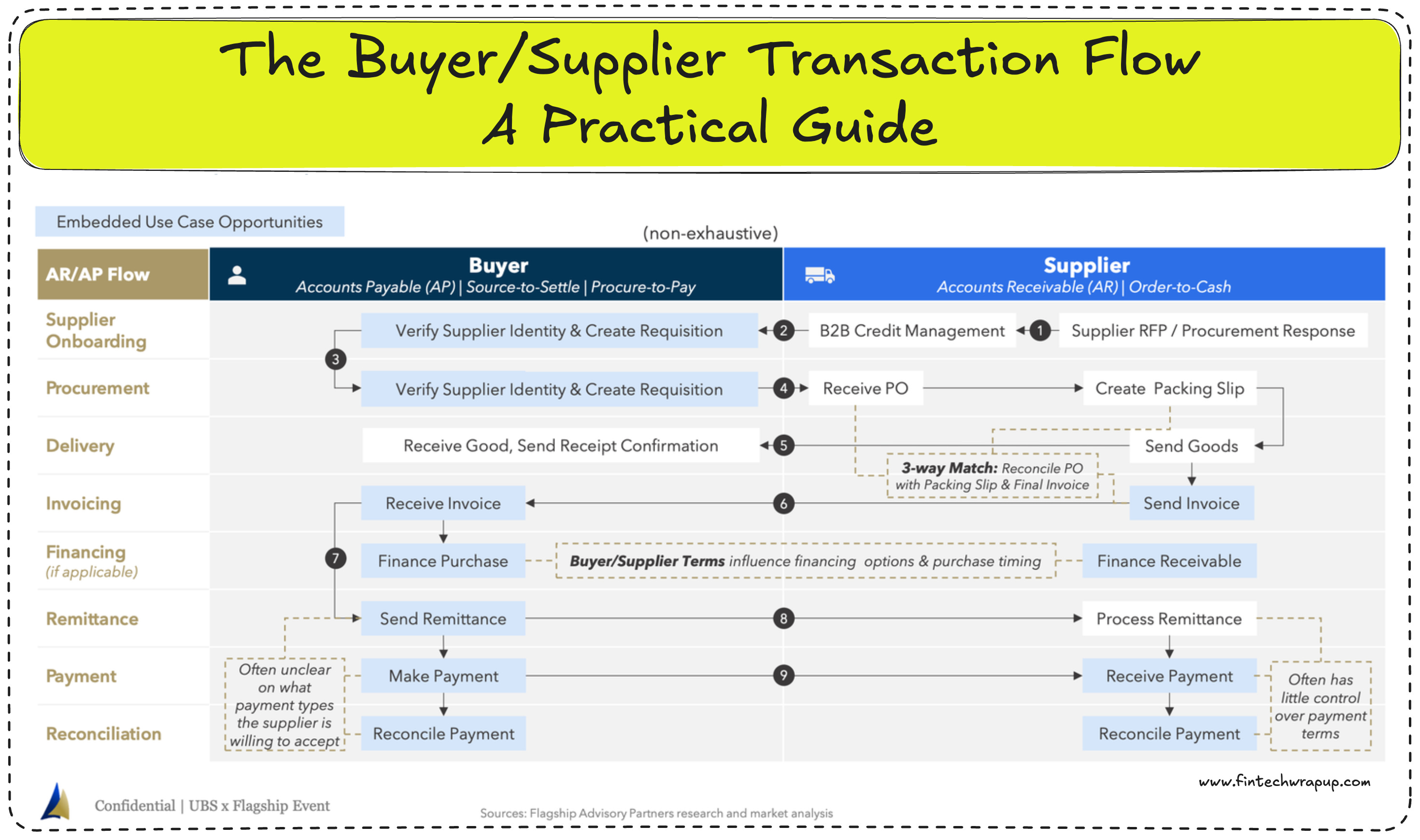

Once the data is verified, smart contracts manage the token's lifecycle. These contracts encode the legal rights associated with the invoice, such as the right to receive payment or the ability to transfer ownership. They automate the transfer of title, allowing the invoice to be traded or used as collateral without manual intervention. This programmability is what enables fractional ownership and real-time settlement, turning illiquid trade receivables into flexible liquidity.

Settlement Rails: Finality and Speed

The final piece is the settlement rail—the blockchain network where the token resides and transactions are finalized. The choice of rail affects transaction costs, speed, and interoperability. While Ethereum offers robust security and liquidity, layer-2 solutions or specialized trade finance chains may offer lower fees and faster finality. The settlement layer must support the token standards (like ERC-20 or ERC-1400) that define the invoice token's properties and compliance requirements.

The infrastructure must work together seamlessly. If the oracle data is delayed, the smart contract execution fails. If the settlement rail is congested, the liquidity dries up. Each layer must be optimized for reliability and speed to support the high-volume, low-margin nature of trade finance.

Choosing the right tokenization platform

Selecting a platform for tokenizing trade finance invoices comes down to matching your operational needs with the right infrastructure. The market offers distinct approaches, ranging from enterprise-grade supply chain solutions to specialized invoice marketplaces. Understanding these differences helps you avoid over-engineering simple use cases or under-engineering complex compliance requirements.

The core decision usually involves three main types of providers:

| Platform Type | Primary Focus | Settlement Speed | Compliance & KYC | Target User |

|---|---|---|---|---|

| Zoniqx | Supply Chain Integration | Near real-time | Built-in KYC/AML | Large Enterprises & Banks |

| Spydra | Trade Asset Liquidity | Fast (Blockchain-based) | Institutional-grade | SMEs & Financial Institutions |

| ONINO | Invoice & Receivable Tokenization | Variable (Platform-dependent) | Standard regulatory frameworks | Corporates & Fintechs |

| 2Tokens | Invoice Markets | Market-driven | Investor-focused | Investors & Invoice Originators |

Enterprise supply chain platforms like Zoniqx focus heavily on integrating tokenization into existing ERP and supply chain workflows. These solutions are ideal for large corporations that need to tokenize receivables across multiple tiers of suppliers. The primary benefit is deep integration, allowing for automated data validation and near real-time settlement. However, these platforms often come with higher implementation costs and longer onboarding times.

Specialized trade finance platforms such as Spydra prioritize liquidity and speed. They are designed to make trade assets accessible to a broader range of investors, including institutional funds. These platforms typically offer robust compliance frameworks tailored for financial institutions, making them suitable for SMEs looking to access capital quickly. The trade-off is that they may require more manual data entry or integration with third-party accounting systems.

Invoice marketplaces like 2Tokens focus on creating secondary markets for tokenized invoices. These platforms are best suited for originators who want to sell invoices to a wide pool of investors. The key advantage is liquidity, as the marketplace model allows for price discovery and competitive bidding. Compliance is often handled at the investor level, which can simplify the process for originators but requires careful vetting of the investor base.

General tokenization providers like ONINO offer flexible solutions that can be adapted to various use cases. These platforms are often favored by fintechs and corporates looking for a customizable infrastructure. They provide the tools to tokenize invoices and receivables but may require additional development work to integrate specific compliance or settlement features. This approach offers the most flexibility but demands more internal technical resources.

When evaluating these options, consider your primary goal: is it liquidity, integration, or market access? Enterprise platforms win on integration, specialized platforms on liquidity, and marketplaces on access. Your existing tech stack and compliance capabilities should dictate the final choice.

Market Dynamics and Investor Strategy

The market for tokenized trade finance invoices is shifting from experimental pilots to institutional infrastructure. For investors, the primary appeal is the ability to access short-term, trade-backed yields with greater transparency than traditional commercial paper. By converting invoices into digital tokens, the market unlocks liquidity for deep-tier suppliers who previously struggled to access working capital, creating a more robust secondary market for these assets [src-serp-7].

Liquidity is the key differentiator here. Traditional trade finance is often siloed and illiquid, with invoices locked in long settlement cycles. Tokenization breaks these silos, allowing investors to buy and sell fractional ownership of receivables on secondary markets with near-instant settlement. This reduces the friction that typically keeps capital idle, turning static trade assets into dynamic, tradable instruments [src-serp-3].

However, the yield opportunity comes with specific risks. Unlike government bonds, these assets are tied to the creditworthiness of the underlying corporate buyers and the operational integrity of the supply chain. Investors must scrutinize the smart contract infrastructure and the legal framework governing the tokenization platform. The risk is not just market volatility, but counterparty default and operational failure in the digital ledger.

To navigate this space, investors should focus on platforms with strong institutional backing and clear regulatory compliance. The value lies not just in the yield, but in the diversification benefits of adding trade finance exposure to a portfolio. As the infrastructure matures, we expect to see tighter integration with traditional banking systems, bridging the gap between decentralized finance and established trade finance practices.

Risk assessment and compliance checks

Tokenized trade finance moves traditional credit risks onto a digital ledger, but it does not erase them. Participants must evaluate counterparty reliability, regulatory alignment, and smart contract integrity before deploying capital.

1. Counterparty and Credit Risk

The core value of tokenized invoices lies in liquidity, but the underlying credit remains tied to the original debtor. If the buyer defaults, the token holder bears the loss. Platforms like Spydra allow multiple investors to fund portions of invoices, which spreads risk but requires rigorous due diligence on the originator’s creditworthiness and the buyer’s payment history.

2. Regulatory and AML Compliance

Trade finance is heavily regulated. Tokenization must comply with anti-money laundering (AML) and know-your-customer (KYC) standards. The International Trade Administration’s Trade Finance Guide emphasizes that any financing tool must ensure proper documentation and legal enforceability. Smart contracts should embed compliance checks to prevent unauthorized transfers or sanctions violations.

3. Smart Contract and Operational Risk

Code errors can lead to irreversible losses. Audited smart contracts are non-negotiable. Additionally, operational risks include oracle failures (incorrect invoice data) and platform downtime. Participants should verify that the underlying infrastructure has robust fallback mechanisms and clear legal recourse for technical failures.

Verify the credit rating of the invoice issuer and the buyer. Check historical payment data and platform transparency reports to assess reliability.

Ensure the tokenization platform complies with local AML/KYC laws and international trade regulations. Confirm that legal frameworks support token ownership and dispute resolution.

Review third-party audit reports for the smart contracts governing the tokens. Test for vulnerabilities in oracle data feeds and transfer mechanisms.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!