What tokenized trade finance invoices are

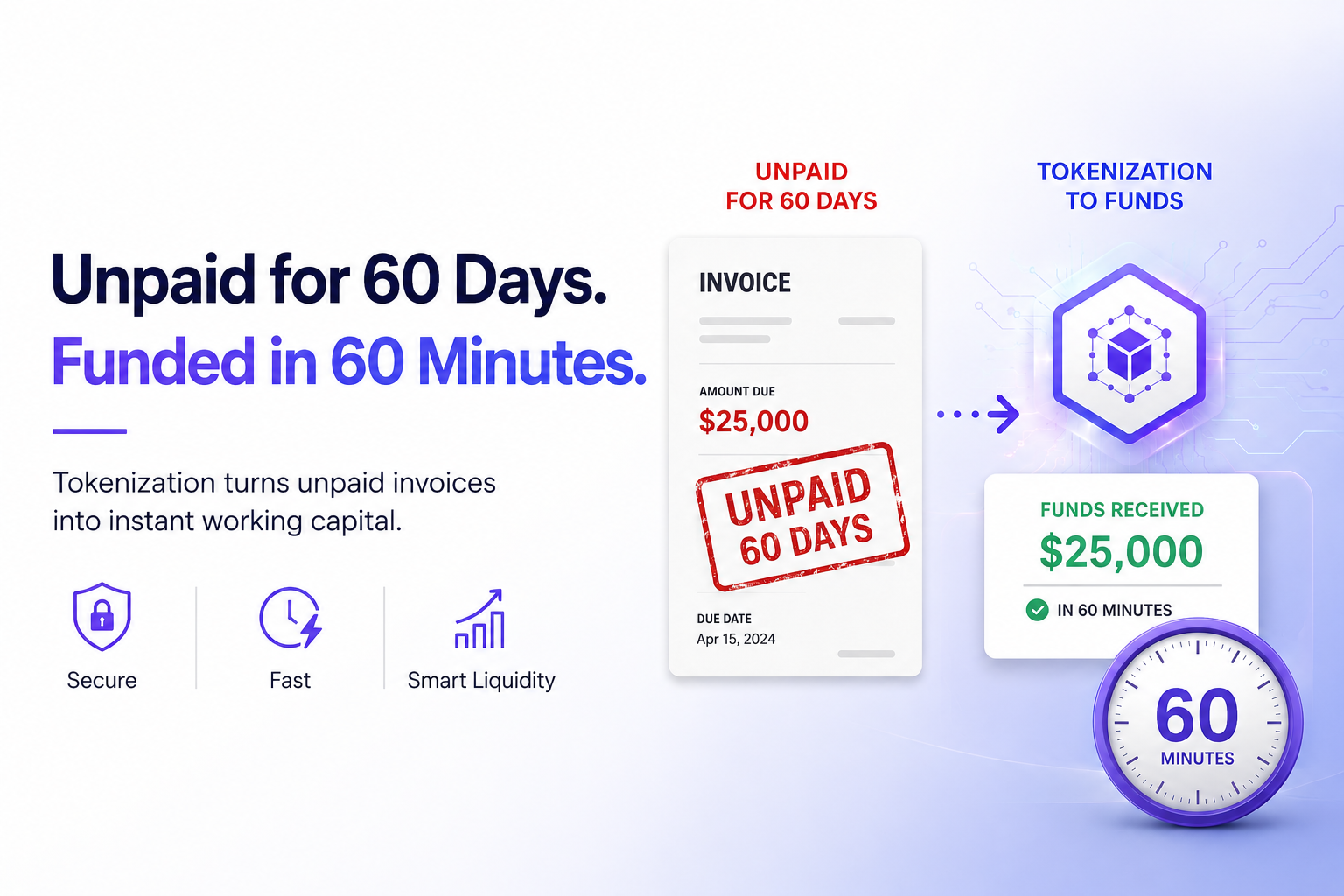

Tokenized trade finance invoices represent a structural shift in how commercial debt is managed. They are not simply digital copies of paper documents or scanned PDFs. Instead, tokenization converts unpaid trade receivables into unique digital assets on a blockchain. This process creates a verifiable, immutable link between the digital token and the underlying legal claim to payment.

The core value lies in this distinction. While digitization merely changes the format of the record, tokenization changes the nature of the asset. It transforms a static invoice into a liquid, tradable instrument. For deep-tier suppliers who often struggle with cash flow, this means their unpaid invoices can be financed or traded directly, bypassing traditional banking bottlenecks. As noted by industry experts, this opens an asset class previously reserved for large institutional banks to a broader range of participants.

This infrastructure enables real-time visibility into the supply chain's financial health. Buyers, suppliers, and financiers can track the status of an invoice from issuance to settlement without relying on fragmented legacy systems. The result is a more efficient market where capital moves faster and risk is better priced.

Market research and liquidity drivers

The tokenized trade finance invoices market is shifting from experimental pilots to a structural component of global supply chains. The primary driver is not merely technological novelty, but the tangible reduction of friction in working capital. By converting paper-based or siloed digital invoices into liquid, programmable tokens, the market is addressing the chronic liquidity gap that has long constrained mid-tier suppliers.

Historically, trade finance was the domain of large multinational corporations with strong credit ratings. Tokenization changes this dynamic. Research indicates that tokenized assets facilitate the securitization of trade finance instruments, allowing smaller, deep-tier suppliers to access working cash more readily and inexpensively. This democratization of liquidity is critical; it transforms illiquid receivables into assets that can be traded or financed at scale, effectively lowering the cost of capital for suppliers who previously relied on expensive factoring services.

The mechanism is straightforward: tokenization enables multiple investors to fund portions of invoices or trade receivables simultaneously. This fractional ownership model increases overall market liquidity by broadening the investor base beyond traditional banks to include hedge funds, family offices, and decentralized finance protocols. The result is a more efficient price discovery process for trade debt, where risk is priced more accurately based on real-time data rather than quarterly reports.

To understand the broader financial context of this shift, it is useful to look at the performance of digital assets that often serve as the settlement layer or collateral in these ecosystems.

Infrastructure and settlement mechanics

Tokenized trade finance invoices rely on a stack of distributed ledger technology (DLT), real-time data oracles, and central bank digital currencies (CBDCs) to function. This infrastructure transforms static paper invoices into dynamic, programmable assets that can be traded and settled instantly.

At the core is the DLT network, which serves as the immutable ledger for invoice ownership and payment history. Unlike traditional banking ledgers that settle in days, DLT allows for near-instantaneous verification of invoice authenticity and status. This transparency reduces the risk of double-spending or fraud, making tokenized invoices more attractive to investors who previously lacked access to this asset class.

Oracles bridge the gap between the on-chain token and the off-chain reality of the underlying trade. They feed real-world data—such as shipment tracking, customs clearance, and invoice maturity dates—into the smart contract. This ensures that the token’s value and transferability are tied to actual commercial events, not just digital entries.

Settlement is where the technology delivers its most significant efficiency gain. By integrating with CBDCs, tokenized invoices can be settled in central bank money rather than commercial bank money. This eliminates counterparty risk and reduces settlement times from T+2 or longer to near-real-time. As noted in research from the University of Surrey, the combination of CBDCs and DLTs enables the seamless settlement of tokenized supply chain finance, fundamentally changing how trade finance operates.

The technical architecture also supports programmability. Smart contracts can automate payment releases upon the fulfillment of specific conditions, such as the arrival of goods at a port. This automation reduces administrative overhead and ensures that all parties adhere to the terms of the trade finance agreement without manual intervention.

Market context

The adoption of this infrastructure is growing as financial institutions seek to modernize trade finance. The tokenized trade finance invoices market is expanding, driven by the need for greater efficiency, transparency, and access to liquidity. As more institutions adopt these technologies, the network effects will further enhance the utility and value of tokenized invoices.

Comparing tokenization platforms and models

Evaluating the tokenized trade finance invoices market research landscape requires looking beyond the hype to understand the underlying infrastructure. The market is currently split between two primary approaches: platform-led tokenization, where a single provider manages the entire lifecycle, and protocol-led models that rely on interoperable smart contracts across multiple blockchains. The choice between these models dictates your settlement speed, regulatory compliance burden, and access to capital.

Platform-led solutions, such as those offered by specialized trade finance fintechs, often provide a more integrated experience. They typically handle KYC/AML checks and investor onboarding within a closed ecosystem, which can accelerate initial deployment. However, this closed-loop nature may limit liquidity sources to the platform’s own network. In contrast, protocol-led models prioritize open access, allowing investors from diverse DeFi or TradFi backgrounds to participate, though this often comes with higher technical complexity for issuers.

To help you weigh these options, we’ve compared key infrastructure providers and models based on settlement efficiency, regulatory stance, and target investor base. This comparison highlights the trade-offs between speed and accessibility in the current market.

| Provider / Model | Settlement Speed | Compliance Approach | Target Investor Base |

|---|---|---|---|

| Platform-led (e.g., Financely Group) | Near-instant (T+0) | Integrated KYC/AML | Institutional & Qualified |

| Protocol-led (DeFi Integrations) | Block-dependent (1-15 min) | Smart contract enforced | Open / Retail & Institutional |

| Hybrid Platforms (e.g., Spydra) | T+1 to T+0 | Hybrid (Off-chain + On-chain) | Mixed (B2B & B2C) |

| Traditional Bank Tokenization | T+1 or T+2 | Strict Regulatory | Internal / Partner Banks |

When selecting a platform, consider your primary bottleneck. If speed and regulatory certainty are paramount, platform-led solutions with integrated compliance layers are often superior. If liquidity depth and cross-border accessibility are your main goals, protocol-led models offer broader reach. Always verify that the provider’s smart contract audits and legal frameworks align with your jurisdiction’s requirements before committing capital.

Strategic Risks and Security Considerations

The shift toward tokenized trade finance invoices market research reveals a complex landscape where technological innovation meets traditional financial gravity. While the potential for liquidity is high, the infrastructure is not without significant vulnerabilities. Smart contract bugs, regulatory ambiguity, and counterparty defaults remain the primary threats to institutional adoption.

Smart Contract Vulnerabilities

Code is law, but code can be flawed. In trade finance, where invoices represent real-world obligations, a single exploit in the underlying smart contract can lead to irreversible loss of assets. Unlike traditional banking errors, blockchain transactions are immutable. This means that a vulnerability in the tokenization layer or the oracle feeding data to the chain can compromise the entire securitization structure. Rigorous auditing and formal verification are not optional; they are the baseline for security.

Regulatory Uncertainty

The regulatory framework for tokenized assets is still evolving. Different jurisdictions treat tokenized invoices differently—some as securities, others as commodities or utility tokens. This fragmentation creates compliance risks for cross-border trade finance. Institutions must navigate a patchwork of laws regarding anti-money laundering (AML), know-your-customer (KYC), and data privacy. The lack of a unified global standard adds operational friction and legal exposure.

Counterparty Risk

Tokenization does not eliminate counterparty risk; it merely changes its form. The risk shifts from the traditional buyer-seller relationship to include technology providers, oracle operators, and custodians. If an oracle fails to report a late payment or a default accurately, the tokenized invoice’s value may be mispriced. Additionally, the insolvency of a key platform provider could freeze assets, highlighting the need for robust contingency planning and decentralized governance models.

Checklist for evaluating tokenized invoice investments

Before committing capital to tokenized trade finance invoices, investors must look beyond the blockchain narrative. The asset class offers liquidity, but it carries specific structural and counterparty risks that traditional due diligence often misses. Use this checklist to assess the viability and safety of any tokenized invoice opportunity.

The token is only as good as the invoice it represents. Confirm that the underlying trade finance documents are real, verifiable, and free of prior liens. Investors should demand access to the original commercial documents, not just a summary. Without this transparency, the tokenized invoice is merely a speculative claim on an unverified asset.

Unlike traditional bonds, tokenized invoices often rely on the credit of the SME or corporation issuing the invoice, not the platform. Evaluate the financial health of the originator. If the issuer defaults, the token’s value collapses regardless of how robust the blockchain infrastructure is. This is a fundamental credit risk, not a technological one.

Ensure the tokenization platform operates within a clear regulatory framework. Look for licenses from financial authorities in the relevant jurisdictions. Platforms operating in gray areas pose significant legal risks, including the potential for asset freezing or forced shutdowns. Compliance is not optional in institutional trade finance.

Tokenization promises liquidity, but secondary markets for trade finance tokens are often thin. Ask how easily you can exit the position. Is there a guaranteed buyback program, or do you rely on finding another buyer? Illiquidity can trap capital, especially during market stress. Verify the depth of the marketplace before investing.

Tokenized trade finance invoices market research shows that while the technology is promising, the execution varies widely. Focus on the fundamentals of the underlying trade, not just the blockchain wrapper.

No comments yet. Be the first to share your thoughts!