What tokenized trade finance invoices actually are

Tokenized trade finance invoices are outstanding receivables converted into digital tokens on a blockchain. This process transforms static paper records or simple digital PDFs into dynamic, onchain assets that can be traded, fractionalized, or used as collateral for immediate liquidity.

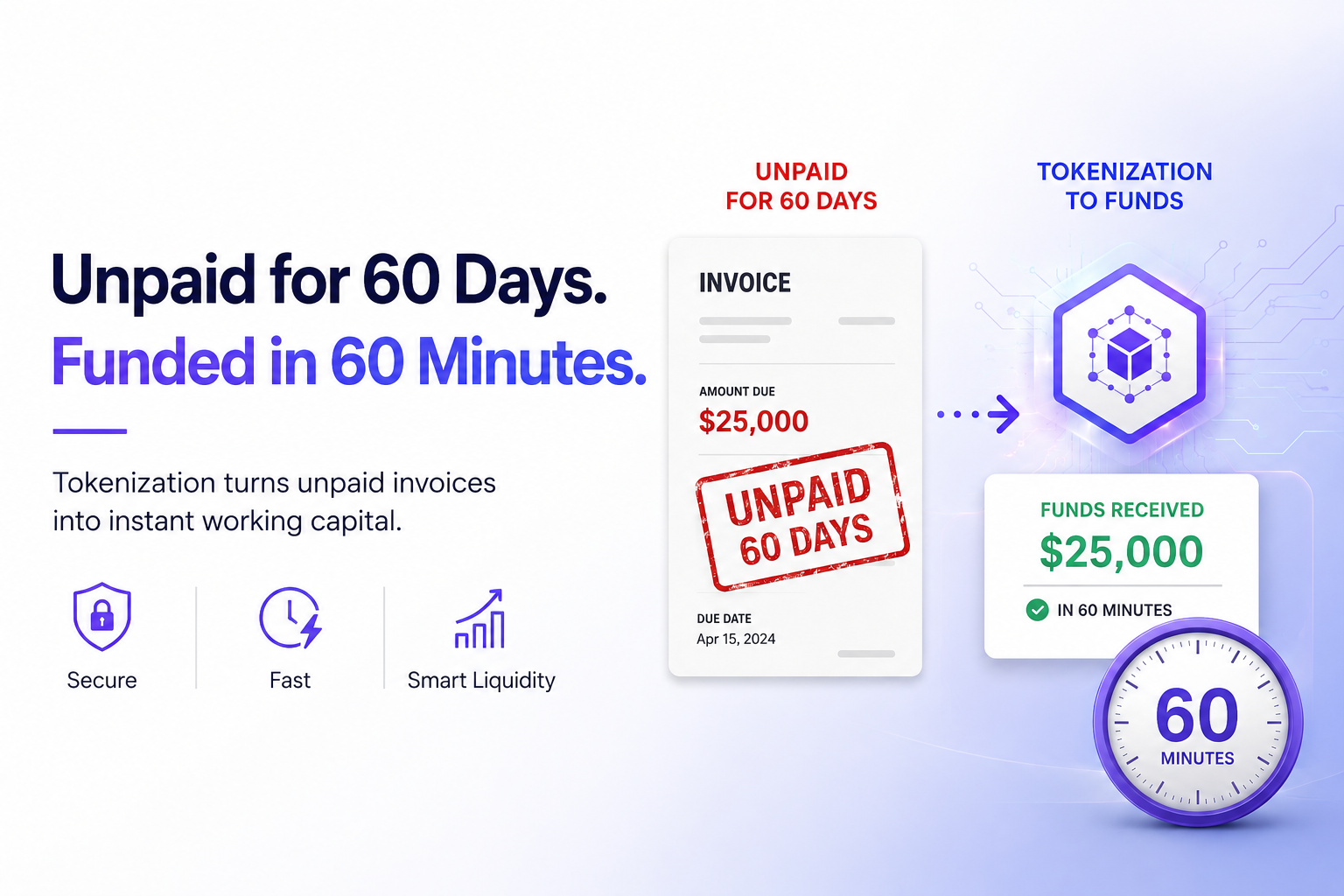

In traditional factoring, a company sells its invoices to a factor at a discount to get cash upfront. The process is often slow, manual, and limited to large volumes. Tokenization removes the middleman. By recording the invoice on a distributed ledger, the asset becomes transparent and verifiable. Investors can buy fractions of an invoice, diversifying their risk across hundreds of smaller trades rather than one large corporate debt.

This shift from static records to tradable assets is the core value proposition. Instead of waiting 60 to 90 days for payment, businesses can unlock capital instantly. The invoice itself becomes the product, moving through the market onchain where settlement is near-instant. This infrastructure supports a new layer of trade finance that is faster, more accessible, and significantly more efficient than legacy systems.

To understand the liquidity dynamics of the broader crypto markets that often underpin these tokenized platforms, it helps to look at the underlying asset performance.

The technology behind this shift relies on smart contracts to automate payments and ownership transfers. When the original debtor pays the invoice, the smart contract automatically distributes the funds to the token holders. This automation reduces counterparty risk and administrative overhead, making trade finance invoices a viable alternative to traditional bank loans for small and medium-sized enterprises.

The infrastructure powering onchain credit

Tokenizing an invoice isn't just about moving data; it's about creating a verifiable bridge between traditional finance and blockchain. The stack that makes this possible relies on three core components: the blockchain ledger, smart contract standards, and oracle networks that verify off-chain reality.

Blockchain layers and smart contracts

At the foundation, you need a blockchain that supports high throughput and low transaction costs. Ethereum remains the standard for security, but many trade finance applications use Layer 2 solutions like Polygon or Base to keep fees negligible. The invoices themselves are represented as tokens, often following standards like ERC-3610 or ERC-1400, which are designed specifically for security tokens and allow for compliance checks directly in the contract logic.

These smart contracts handle the lifecycle of the invoice: issuance, transfer, and repayment. When a buyer approves an invoice, the smart contract locks the obligation, turning it into a liquid asset that suppliers can use immediately. This removes the need for manual reconciliation between ERP systems and bank ledgers.

Oracle networks for verification

Smart contracts cannot see the real world on their own. This is where oracle networks like Chainlink come in. They act as the trusted bridge, pulling data from off-chain sources—such as ERP systems, shipping logs, and bank statements—to verify that the invoice is legitimate and that the goods have been delivered.

Without oracles, tokenized invoices would be unsecured promises. With them, the blockchain has access to real-world proof of trade. This verification process is critical for deep-tier supply chain finance, where the creditworthiness of the anchor buyer must be accurately reflected in the tokenized value.

Market context

The infrastructure is only as valuable as the liquidity it attracts. As institutional adoption grows, the underlying assets backing these tokens often correlate with broader DeFi and TradFi hybrid markets. Monitoring these trends helps investors and financiers understand the health of the tokenized credit space.

Top tools for issuing and managing invoices

The infrastructure for tokenized trade finance has moved beyond experimental pilots to distinct operational categories. Businesses and investors now choose between centralized platforms that integrate with existing ERP systems and decentralized protocols that prioritize open liquidity. Selecting the right tool depends on whether your priority is seamless corporate integration or access to a broader, permissionless investor base.

Centralized Enterprise Platforms

Centralized platforms like ONINO focus on bridging traditional supply chain finance with blockchain technology. These tools are designed for businesses that need to tokenize invoices without disrupting their current accounting workflows. They typically offer API integrations with major ERP systems, allowing companies to issue tokenized receivables directly from their existing data. This approach reduces friction for corporate treasurers who require strict compliance and audit trails.

Decentralized Invoice Markets

Decentralized protocols such as 2Tokens operate as open markets where invoices are listed as tradable assets. These platforms prioritize liquidity and price discovery over direct corporate integration. Investors can browse and purchase tokenized invoices based on risk profiles and yield expectations. This model democratizes access to trade finance, allowing smaller investors to participate in asset-backed opportunities that were previously reserved for institutional players.

Platform Comparison

The table below compares the primary characteristics of leading tools in the tokenized invoice space. This comparison highlights the trade-offs between enterprise-grade control and open-market accessibility.

| Platform | Type | Corporate Integration | Liquidity Source | Supported Chains |

|---|---|---|---|---|

| ONINO | Enterprise | ERP APIs | Institutional Partners | Multi-chain |

| 2Tokens | Decentralized | Wallet-Based | Open Market | Polygon |

| TradeGo | Hybrid | Portal-Based | Bank Network | Hyperledger |

| Marco Polo | Enterprise | SWIFT/GLT | Bank Consortium | R3 Corda |

Extending financing to deep-tier supply chains

Tokenization solves the deepest problem in supply chain finance: credit access. In traditional models, only tier-one suppliers benefit from the anchor buyer’s strong balance sheet. Tier-two and tier-three vendors face higher borrowing costs because their creditworthiness is independent and often weaker. Tokenization fixes this by embedding the anchor’s credit into the digital invoice itself.

When a tier-one supplier breaks an invoice into tokens for a sub-supplier, the token carries the anchor’s credit rating. This allows deep-tier vendors to access liquidity at rates nearly equal to the anchor’s cost of capital. The result is a more resilient supply chain where smaller vendors can operate without the constant threat of cash flow shortages.

This structural shift reduces financing costs across the entire network. By lowering the discount rate for tokenized invoices, the system creates a more efficient capital flow. The anchor buyer’s credit becomes a public good for the supply chain, not just a private advantage for top-tier partners.

-

Verify anchor credit transferability in smart contracts

-

Assess oracle reliability for invoice data integrity

-

Model liquidity depth for tier-2 and tier-3 vendors

-

Ensure regulatory compliance for cross-border token transfers

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!