What tokenized trade finance invoices actually are

Tokenized trade finance invoices are unique digital assets created on a blockchain that represent a specific underlying receivable. This process converts invoice details—such as the payment amount, due date, and buyer-seller information—into a token that can be tracked, transferred, and settled on-chain.

This distinction matters because it shifts trade finance from a bilateral relationship to a liquid asset class. Traditional factoring relies on a direct agreement between a supplier and a factor, often involving manual verification and slow settlement. Tokenization breaks this silo by allowing the invoice to exist as a tradable commodity. Once tokenized, the asset can be fractionalized, pooled, or used as collateral across different platforms and jurisdictions without the friction of traditional intermediaries.

The infrastructure behind this shift is designed for efficiency. By recording the invoice on a distributed ledger, all parties can see the same verified data in real time. This reduces the risk of double-financing, where the same invoice is used as collateral for multiple loans. It also opens the door for institutional investors to access trade finance markets that were previously restricted to large banks with established supplier relationships.

The infrastructure powering onchain credit

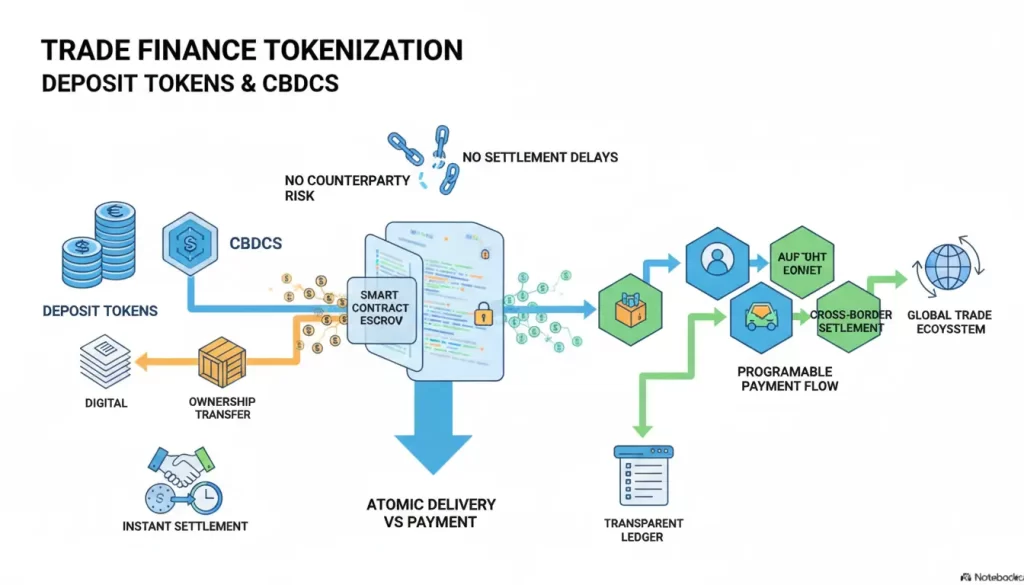

Tokenizing trade finance invoices isn’t just about moving paperwork to a blockchain; it requires a specific technical stack to bridge the gap between traditional finance and decentralized protocols. This infrastructure relies on three core components: oracles to verify real-world data, smart contracts to manage issuance, and stablecoin rails for settlement.

Oracles: Bridging Real-World Data

Smart contracts cannot natively read off-chain information, such as whether a buyer has actually received goods or paid an invoice. Oracles solve this by feeding verified data onto the blockchain. In trade finance, this means connecting traditional ERP systems or banking APIs to the ledger. Without reliable oracles, the tokenized invoice would lack the trust necessary for lenders to accept it as collateral.

Smart Contracts: Issuance and Logic

Once data is verified, smart contracts handle the issuance of the token. These self-executing agreements define the terms of the loan, the repayment schedule, and the rights of the token holders. They automate the lifecycle of the invoice, from creation to maturity. This reduces administrative overhead and ensures that all parties adhere to the agreed-upon rules without manual intervention.

Stablecoin Rails: Settlement

The final piece is the settlement layer. Stablecoins provide the liquidity and speed needed for cross-border trade. Unlike traditional banking wires, which can take days to clear, stablecoin transactions settle in minutes. This efficiency is critical for businesses that rely on cash flow to operate. By using stablecoins, lenders can disburse funds instantly, and borrowers can repay with minimal friction.

This stack creates a transparent, efficient, and automated system for trade finance. By leveraging oracles, smart contracts, and stablecoins, businesses can access the value of their unpaid invoices and obtain liquidity faster than traditional methods allow.

Liquidity and investor access

Tokenized trade finance invoices shift how capital moves through the supply chain. Instead of relying on a single bank or factor to fund a receivable, the asset is split into digital tokens. This structure allows multiple investors to buy fractional shares of the invoice, bringing new capital into a market that has traditionally been closed to anyone outside large financial institutions.

For small and medium-sized enterprises (SMEs), this fragmentation solves a persistent cash flow problem. Traditional factoring often involves high fees and strict eligibility criteria that exclude smaller businesses. Tokenization opens the door to a broader pool of capital. SMEs can access funding faster because the settlement happens on-chain, reducing the administrative lag typical of traditional banking. This access to liquidity helps businesses manage working capital without waiting 30 to 90 days for their clients to pay.

Investors gain entry to a new asset class with distinct risk and return profiles. By holding tokens backed by real trade receivables, investors can diversify their portfolios with short-term, self-liquidating assets. This exposure is not limited to major corporations; it includes invoices from diverse industries and regions, spreading risk across a wider base. The ability to trade these tokens on secondary markets also adds flexibility, allowing investors to exit positions before the invoice matures if needed.

The following comparison highlights the structural differences between traditional invoice factoring and tokenized trade finance.

| Feature | Traditional Factoring | Tokenized Trade Finance |

|---|---|---|

| Capital Access | Limited to bank partners | Open to fractional investors |

| Speed | Days to weeks | Hours to days |

| Minimum Investment | High thresholds | Low entry points |

| Secondary Market | Rare and illiquid | Enabled by blockchain |

| Transparency | Opaque ledger | On-chain verification |

Strategic implementation for businesses

Adopting tokenized trade finance invoices requires a shift from manual document handling to structured digital infrastructure. This process involves mapping existing supply chain workflows to on-chain protocols, ensuring that every invoice, letter of credit, or bill of lading can be securely tokenized and traded.

1. Audit and digitize supply chain documents

Before tokenization can begin, your trade finance documents must be in a structured, digital format. Traditional paper-based invoices or unstructured PDFs cannot be directly converted into reliable on-chain assets. Start by auditing your current accounts payable and receivable systems. Identify which documents are already digitized and which require scanning or API integration. This foundational step ensures data integrity, as the value of the tokenized invoice depends entirely on the accuracy of the underlying off-chain data.

2. Select a compatible tokenization platform

Not all blockchain platforms support the regulatory and technical requirements of trade finance. Look for platforms that offer interoperability with existing ERP systems and support standard token formats like ERC-3643 or ERC-1400, which are designed for security tokens. Evaluate platforms based on their ability to handle complex trade workflows, including multi-party verification and compliance checks. The goal is to choose a platform that acts as a bridge between traditional banking infrastructure and decentralized finance (DeFi) liquidity pools.

3. Integrate with existing ERP systems

Seamless integration with your Enterprise Resource Planning (ERP) system is non-negotiable. The tokenization platform must be able to pull invoice data directly from your ERP (such as SAP, Oracle, or NetSuite) to ensure real-time accuracy. This integration allows for automated token minting when an invoice is approved and automatic redemption when payment is received. Without this connection, the process becomes manual and prone to errors, defeating the purpose of automation.

4. Conduct due diligence on counterparties

Tokenization expands your pool of potential financiers, but it also introduces new counterparty risks. Perform thorough due diligence on the platform provider and any liquidity providers you interact with. Verify their regulatory compliance, security audits, and track record in handling financial assets. Since tokenized invoices represent legal claims on payment, the legal framework governing the token must be robust and enforceable across jurisdictions.

5. Pilot with a controlled invoice batch

Begin with a small, controlled pilot program. Select a subset of invoices from trusted suppliers or customers to test the end-to-end tokenization and financing process. Monitor the system for technical glitches, compliance bottlenecks, and user adoption issues. Use this pilot to refine your workflows and train your finance team. Once the pilot demonstrates reliability and cost savings, you can scale the implementation to your entire supply chain.

Convert paper invoices into structured digital data. Ensure all documents are ready for on-chain conversion to maintain data integrity and legal enforceability.

Choose a blockchain platform that supports security token standards and integrates with traditional banking systems for regulatory compliance.

Connect the tokenization platform directly to your ERP software to automate invoice minting and payment redemption, reducing manual entry errors.

Verify the regulatory status and security audits of the platform provider and liquidity partners to mitigate financial and legal risks.

Test the system with a small group of invoices to identify technical issues and train staff before full-scale implementation.

Risks, regulation, and security considerations

Tokenized trade finance moves real-world debt onto public ledgers, which introduces specific risks that differ from traditional banking. The primary concern is regulatory compliance. Since these tokens represent legal claims on payment, they must adhere to existing securities laws and anti-money laundering (AML) frameworks. Jurisdictions vary widely in how they treat digital assets, so projects must navigate a complex web of local and international regulations to ensure the underlying contracts remain enforceable.

Smart contract risk is the second major hurdle. While blockchain offers transparency, the code governing the token is only as secure as its development. Bugs or vulnerabilities in the smart contract can lead to the loss of funds or unauthorized access to the invoice data. Audits are standard practice, but they are not a guarantee. Developers must also consider oracle reliability, as the system depends on accurate off-chain data to trigger payments or update token status.

Finally, the integrity of the real-world asset is paramount. If the underlying invoice is fraudulent or the debtor defaults, the token’s value collapses. Verification processes must be rigorous, linking the digital token directly to a legitimate, verified trade transaction. Without this bridge to physical reality, the entire infrastructure lacks trust.

No comments yet. Be the first to share your thoughts!