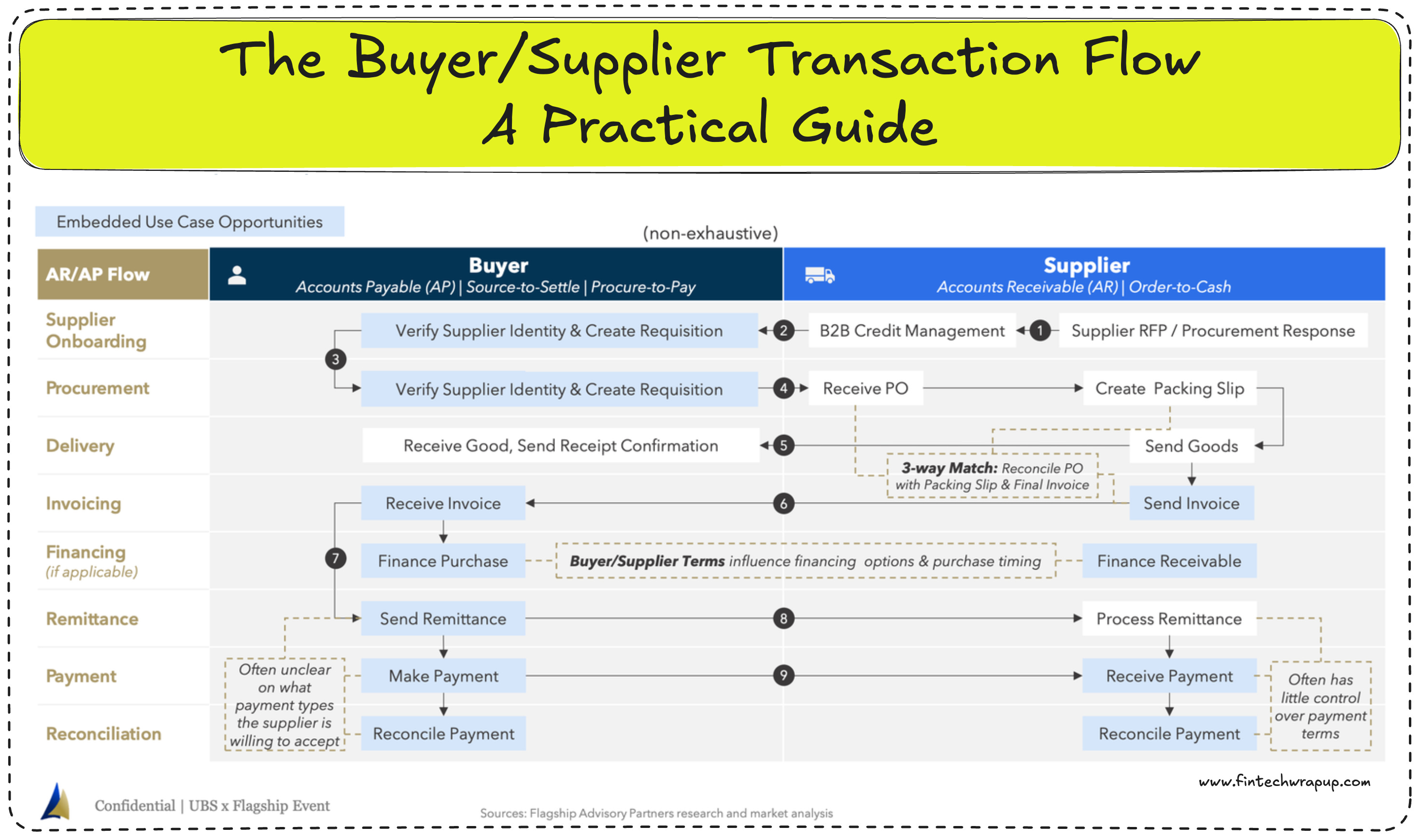

What tokenized trade invoices actually are

At its core, tokenized trade finance invoice is the digitization of an unpaid receivable into a tradable on-chain asset. When a supplier delivers goods but hasn't yet received payment, the resulting invoice represents a claim on future cash flow. Tokenization converts this legal claim into a digital token on a blockchain, effectively turning a static, illiquid paper document into a liquid financial instrument.

This process does not change the underlying debt; it changes how that debt is held and transferred. By recording the invoice on a distributed ledger, all parties—suppliers, buyers, and financiers—can see the same real-time data. This transparency reduces the friction typically associated with verifying authenticity and ownership in traditional trade finance. The token acts as a proxy for the invoice, allowing it to be used as collateral for immediate financing or sold to investors seeking yield.

The mechanism bridges traditional trade finance with decentralized finance (DeFi) infrastructure. Instead of waiting 30, 60, or 90 days for payment, a company can tokenize its receivables and access liquidity instantly. This shifts the focus from mere record-keeping to active capital management, where unpaid invoices become working capital rather than frozen assets. Understanding this infrastructure is essential for grasping how modern trade finance is evolving beyond traditional banking channels.

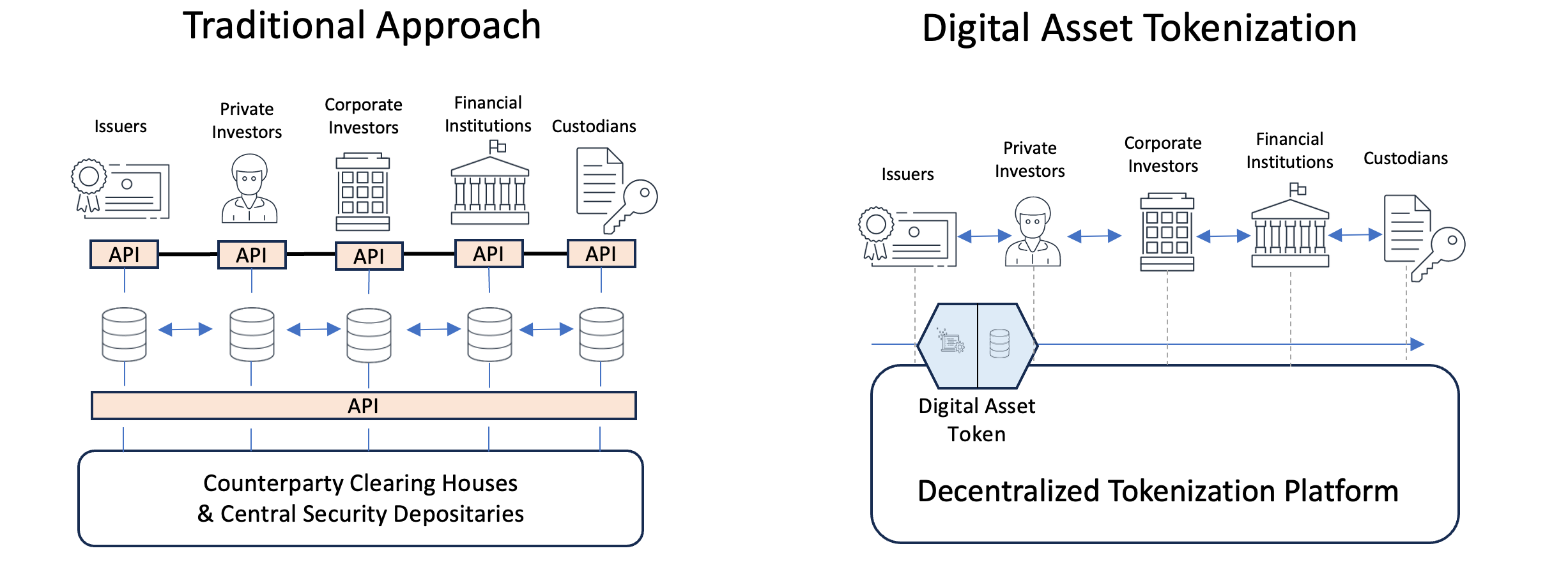

The infrastructure behind on-chain receivables

Use this section to make the Tokenized Trade Finance Invoices decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Liquidity benefits for deep-tier suppliers

Tokenized trade finance invoices solve a persistent problem in supply chain finance: the disconnect between the anchor buyer’s strong credit rating and the financial vulnerability of smaller, deep-tier suppliers. In traditional models, financing is often limited to direct (first-tier) vendors who have established relationships with banks. Second- and third-tier suppliers, who provide raw materials or specialized components, are frequently excluded or forced to pay exorbitant interest rates due to perceived risk.

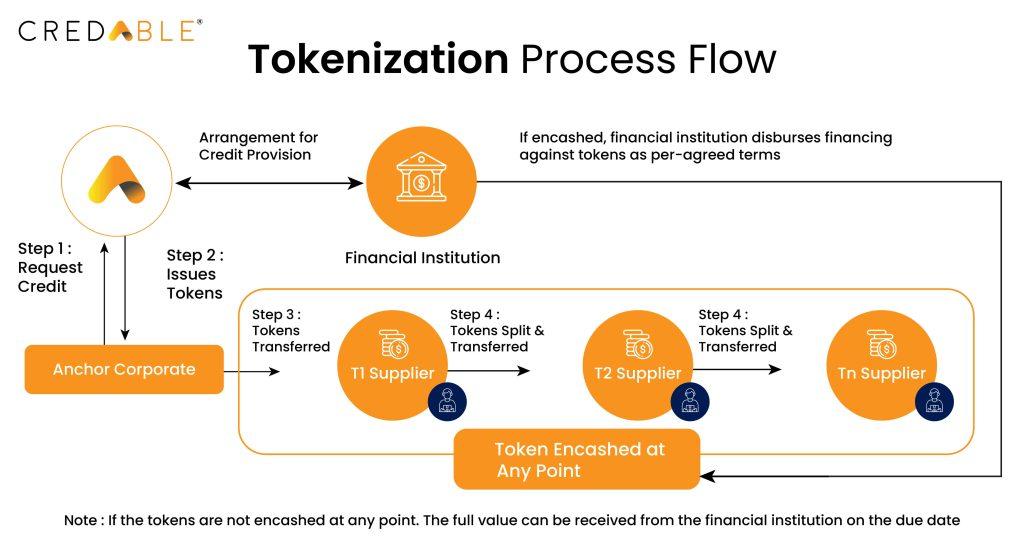

Tokenization bridges this gap by embedding the anchor buyer’s creditworthiness directly into the digital asset. When a first-tier supplier’s invoice is tokenized and passed down the chain, the resulting digital token carries the anchor’s credit profile. This allows deep-tier suppliers to access financing based on the anchor’s robust credit rating rather than their own limited balance sheet. The result is a significant reduction in financing costs and improved cash flow for the smaller players who keep the supply chain moving.

This mechanism effectively turns trade receivables into liquid assets. Instead of waiting 60, 90, or 120 days for payment, deep-tier suppliers can sell these tokenized invoices to a broader pool of investors on secondary markets. This fragmentation of risk allows multiple investors to fund portions of invoices, increasing overall liquidity and providing suppliers with the working capital they need to operate efficiently. By democratizing access to low-cost capital, tokenization strengthens the resilience of the entire supply network.

Tools and platforms for tokenization

Invoice tokenization is no longer a theoretical exercise; it is an operational reality supported by a growing stack of infrastructure providers. These platforms do not merely digitize paper—they create a bridge between traditional trade finance and on-chain liquidity, allowing companies to convert unpaid claims into tradable digital assets.

The current landscape is defined by specialized utility rather than generic blockchain wrappers. Leading platforms focus on three core capabilities: oracle integration for real-world data verification, settlement speed, and clear target user bases ranging from SMEs to large institutional lenders. Without reliable oracles, tokenized invoices lack the trust necessary for institutional adoption.

The following comparison highlights how major platforms differentiate themselves in the tokenized trade finance space.

Platforms like ONINO streamline the process for suppliers by focusing on receivables financing, while others like Spydra provide the deeper infrastructure layer for banks and investors to fund portions of invoices. Chainlink’s role remains critical across this ecosystem, providing the decentralized oracle networks that verify invoice authenticity and payment status on-chain. This verification is the linchpin that transforms a static PDF invoice into a dynamic, collateralizable token.

Strategic risks and regulatory hurdles

Tokenized trade finance operates in a high-stakes environment where legal enforceability and regulatory clarity lag behind technical capability. While the infrastructure is maturing, the market remains constrained by unresolved questions around smart contract law and cross-border compliance.

Legal enforceability of smart contracts

The core promise of tokenization is automated execution, but courts in many jurisdictions have not yet established clear precedents for enforcing smart contracts as binding legal instruments. This creates a gap between digital settlement and legal recourse. If a dispute arises over invoice authenticity or delivery terms, the code may execute automatically, but the legal system may not recognize the outcome without traditional documentation. Enterprises must ensure that tokenized records are backed by legally binding master agreements that can withstand judicial scrutiny.

Regulatory uncertainty

Regulators are still defining how tokenized invoices fit into existing frameworks for securities, money transmission, and anti-money laundering (AML). The classification of these assets varies significantly across borders, creating compliance complexity for global trade finance. For instance, an invoice tokenized in one jurisdiction may be deemed a security in another, triggering different registration and reporting requirements. This fragmentation discourages broad adoption, as financial institutions prefer predictable regulatory environments. The Bank for International Settlements (BIS) and other central banks have highlighted the need for harmonized standards to mitigate these risks.

Operational risks

Beyond legal and regulatory challenges, operational risks remain significant. These include cybersecurity threats, smart contract vulnerabilities, and integration failures with legacy banking systems. A single point of failure in the tokenization platform can disrupt entire supply chains. Additionally, the liquidity of tokenized invoices depends on the depth of the secondary market, which is still nascent. Without sufficient buyers, tokenized assets may not offer the liquidity advantages promised. Companies must conduct rigorous due diligence on platform security and market depth before committing capital.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!