What tokenized trade finance invoices are

Tokenized trade finance invoices are unpaid financial claims represented as digital tokens on a blockchain. This process converts static, paper-based receivables into dynamic, on-chain assets that can be financed, traded, or settled programmatically.

In traditional trade finance, an invoice is a promise of future payment that sits in a ledger, illiquid and difficult to verify. By tokenizing the invoice, the underlying claim is digitized. This creates a unique cryptographic representation of the debt that can be transferred between parties without the friction of manual reconciliation.

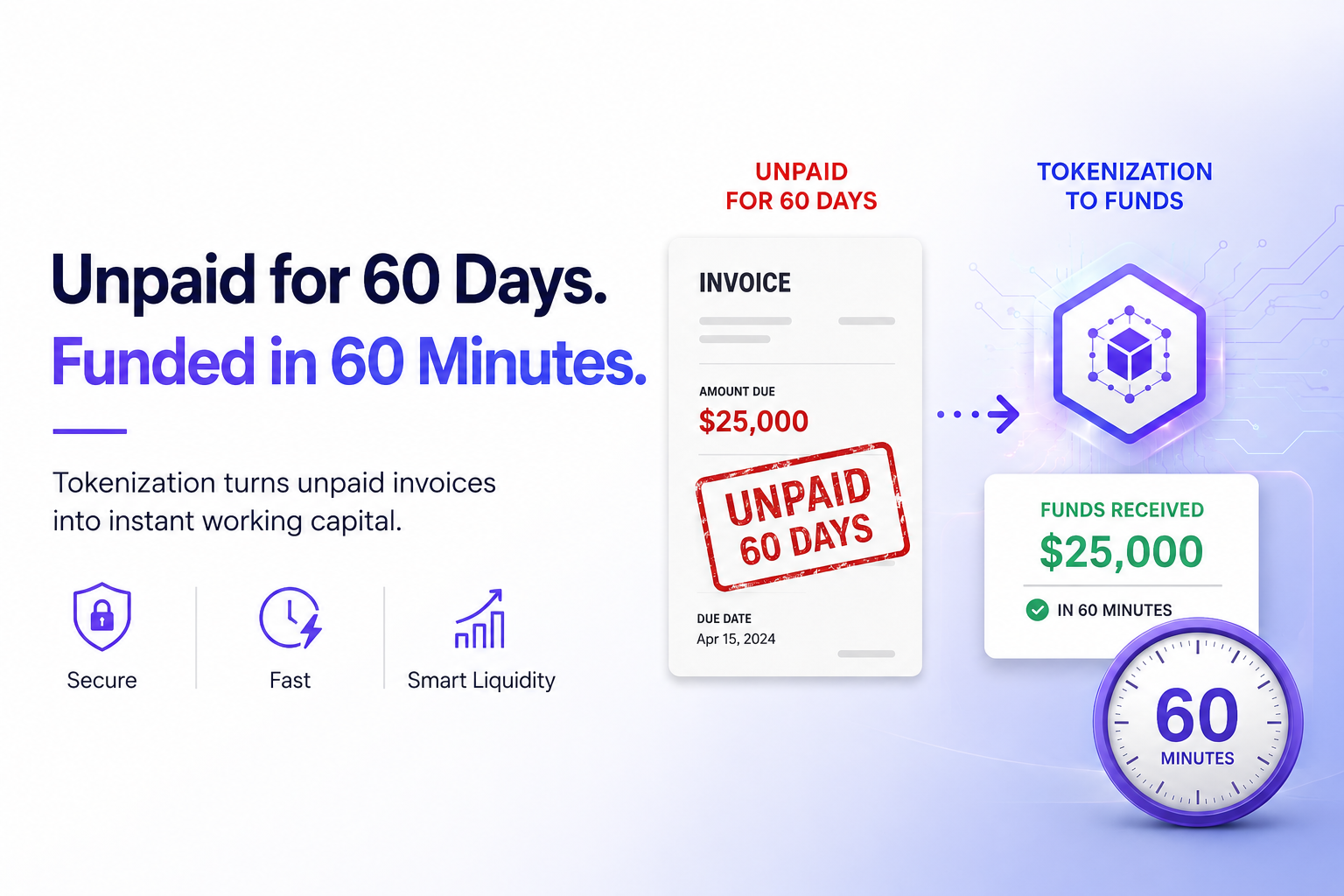

The infrastructure relies on smart contracts to enforce the terms of the invoice. When an invoice is tokenized, the smart contract holds the rights to the payment. Investors or lenders can purchase these tokens, providing immediate liquidity to the seller. The buyer still pays the full amount at the original due date, but the seller no longer has to wait for cash flow.

This shift from offline paperwork to on-chain tokens reduces counterparty risk. The immutable nature of the blockchain provides a single source of truth for the invoice's status, ownership, and payment history. As noted by Chainlink, this representation allows financial claims to be integrated directly into decentralized finance (DeFi) protocols, unlocking new sources of capital for trade.

How tokenized trade finance invoices move through the system

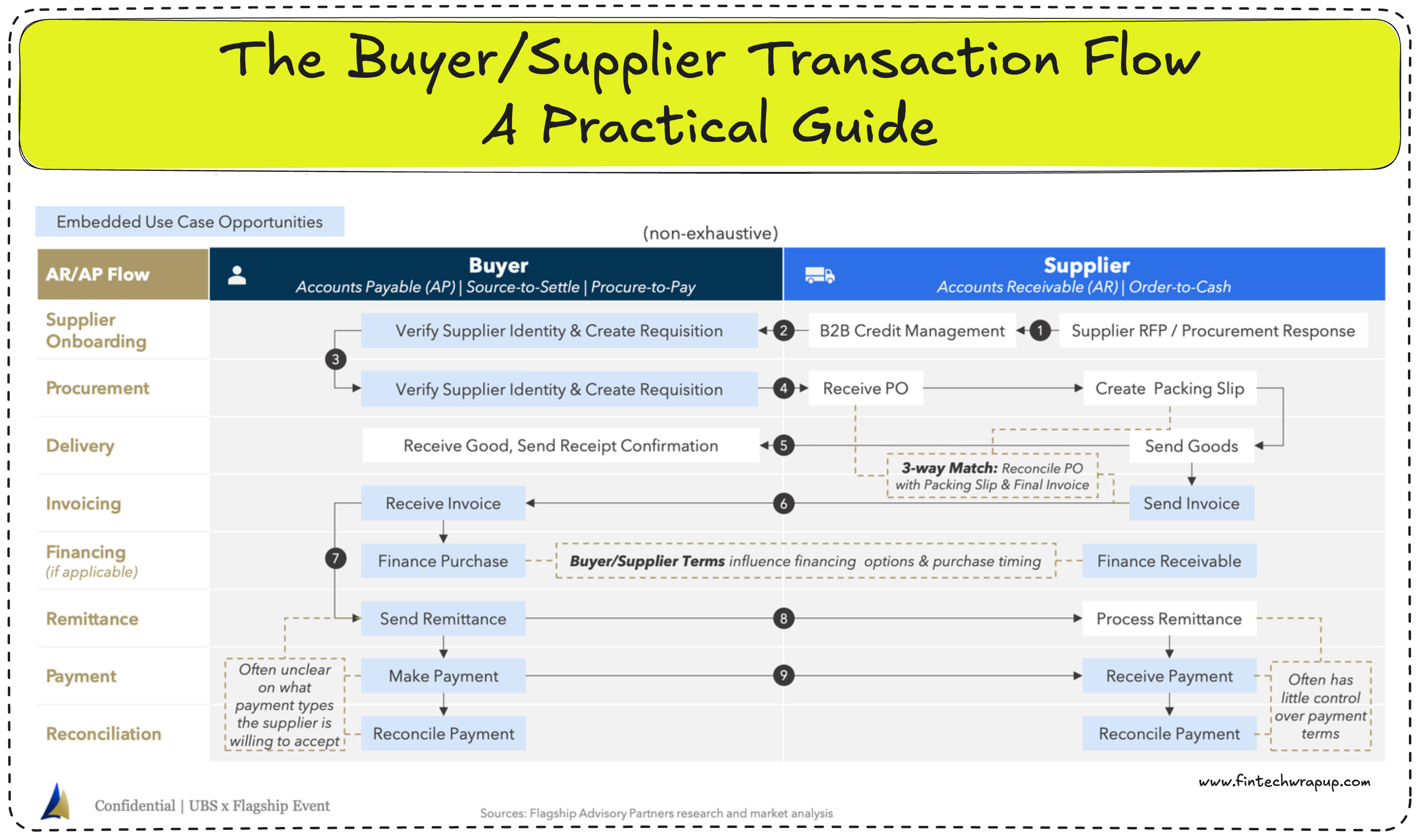

The workflow for tokenizing trade finance invoices follows a strict sequence: issuance, verification, minting, and trading. Each step relies on specific infrastructure to ensure that the digital representation of the invoice is legally binding and financially sound. Without this structured pipeline, the liquidity benefits of tokenization cannot be realized.

The process begins when a supplier issues a trade invoice or trade receivable. This unpaid claim is digitized and recorded on a distributed ledger. The invoice data, including payment terms and buyer details, is structured into a smart contract that defines the asset’s properties. This step transforms a traditional paper-based claim into a programmable digital asset.

Before the asset enters the market, all participants must undergo strict Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. This ensures that only verified investors and institutions can interact with the tokenized invoice. The verification process is typically handled by centralized identity providers or decentralized identity protocols, creating a permissioned layer that maintains regulatory compliance.

Once verified, the invoice data is minted as a token on a blockchain. This token represents a fractional or whole ownership stake in the underlying receivable. The minting process locks the original invoice data off-chain or on a private layer, while the token on the public or permissioned chain serves as the tradable proof of ownership. This token is now ready for secondary market trading.

The final step is trading. Investors can buy, sell, or hold these tokenized invoices on decentralized or centralized platforms. This liquidity allows suppliers to access capital faster than traditional factoring, while investors gain exposure to short-term, asset-backed returns. The entire lifecycle, from issuance to settlement, is transparent and immutable on the blockchain.

This structured approach ensures that tokenized trade finance invoices are not just digital copies of paper documents, but functional financial instruments. The integration of KYC/AML checks and smart contract automation reduces counterparty risk and operational friction, making the market more accessible to a broader range of participants.

Dual value for suppliers and investors

Tokenized trade finance invoices create a two-sided market where liquidity meets need. Suppliers get immediate cash flow, while investors access higher yields with transparent risk data. This structure bridges the gap between traditional supply chain finance and modern digital asset markets.

Faster working capital for suppliers

For suppliers, especially deep-tier vendors, tokenization solves the cash flow bottleneck. Traditional factoring often excludes smaller suppliers due to high costs and manual verification. Tokenization automates this process, allowing invoices to be split and sold in seconds.

This speed is critical for maintaining operations. Instead of waiting 60-90 days for payment, suppliers can access funds immediately upon invoice approval. The reduced intermediary layer also lowers discount rates, keeping more capital in the supplier’s pocket. It’s not just about speed; it’s about accessibility for smaller players in the supply chain.

Higher yields and liquidity for investors

Investors benefit from the granular exposure to trade receivables. Tokenization allows for fractional ownership of invoices, lowering the entry barrier for institutional and retail investors alike. This fractionalization increases market liquidity, as tokens can be traded on secondary markets more easily than traditional trade finance instruments.

The transparency of blockchain records provides investors with real-time visibility into invoice status and payment history. This data reduces information asymmetry, allowing for more accurate risk pricing. As a result, investors can achieve higher yields compared to traditional fixed-income instruments, with the added benefit of diversification across multiple suppliers and industries.

Comparison: Traditional vs. Tokenized

| Feature | Traditional Invoice Factoring | Tokenized Trade Finance Invoices |

|---|---|---|

| Settlement Speed | Days to weeks | Seconds to minutes |

| Access for Deep-Tier Suppliers | Limited | Broad |

| Minimum Investment | High (often $50k+) | Low (fractional ownership) |

| Transparency | Manual, opaque | Real-time, on-chain |

| Liquidity | Illiquid until payment | Tradeable on secondary markets |

The shift from opaque, manual processes to transparent, automated systems is reshaping trade finance. Suppliers gain access to capital they previously couldn’t reach, while investors find a new asset class with better risk-adjusted returns.

Essential tools and infrastructure platforms

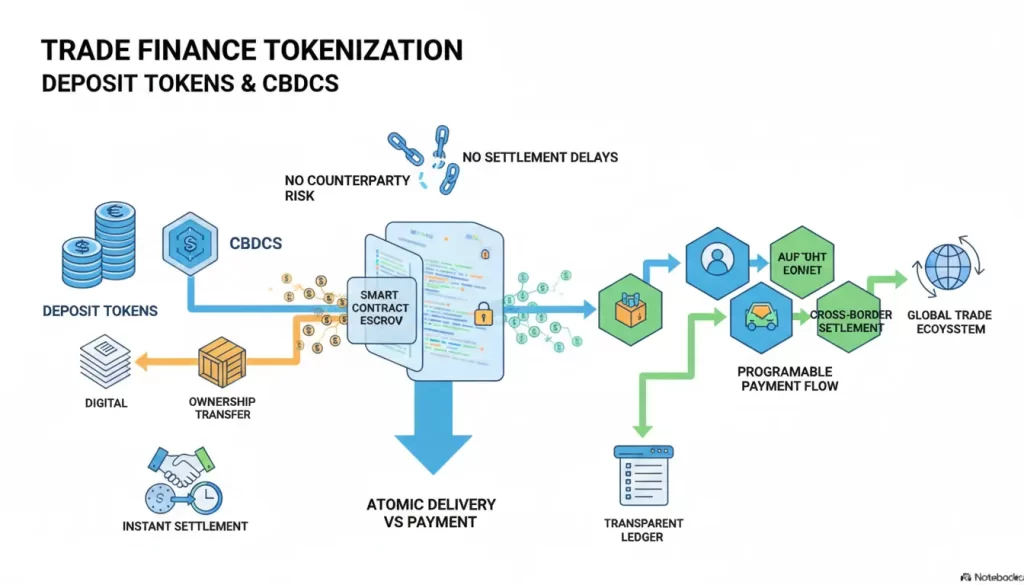

Tokenizing trade finance invoices is not a solitary act; it requires a stack of interoperable systems. The infrastructure layer bridges the gap between traditional banking ledgers and public blockchains, ensuring that digital tokens are backed by real-world data and can settle efficiently.

Oracle Integration and Data Verification

The most critical component in this stack is the oracle network. Since invoices originate off-chain, they require a trusted bridge to communicate their status—such as payment due dates or credit ratings—to the blockchain. Chainlink serves as the industry standard for this verification, pulling real-world invoice data into smart contracts. This ensures that the tokenized asset reflects the actual financial claim, preventing discrepancies between the digital token and the underlying paper invoice.

Without reliable oracles, tokenized invoices would be blind to their own validity. The oracle acts as the sensory organ of the smart contract, confirming that the invoice has not been paid elsewhere and that the debtor remains solvent. This verification step is what transforms a static PDF into a dynamic, tradable financial instrument.

Settlement Layers and Marketplaces

Once verified, the invoice must settle on a layer that balances speed with regulatory compliance. Platforms like 2Tokens provide the marketplace infrastructure, allowing tokenized invoices to be listed and traded by institutional investors. These platforms handle the legal wrappers and investor onboarding, making the asset class accessible without requiring every participant to be a blockchain expert.

The settlement layer often utilizes stablecoins or central bank digital currencies (CBDCs) to finalize transactions. This reduces the friction of cross-border payments, which traditionally take days to clear. By settling on-chain, lenders can access liquidity in minutes rather than weeks, turning idle receivables into immediate working capital.

Market Context

The growth of this infrastructure is mirrored in the performance of related RWA (Real World Asset) tokens. As institutional adoption of tokenized trade finance increases, so does the market capitalization of the platforms facilitating these trades. The following chart illustrates the price action of ONDO Finance, a prominent player in the RWA tokenization space, reflecting broader market interest in on-chain financial infrastructure.

Market Dynamics and Institutional Adoption

The tokenization of trade finance invoices has moved from experimental pilot programs to a phase of measurable institutional adoption. Driven by the need for greater liquidity in traditional receivables, major financial institutions are increasingly treating tokenized trade assets as a core component of their treasury and supply chain finance strategies. This shift is not merely about digitizing paper; it is about creating a new class of onchain assets that can be traded, settled, and financed with unprecedented speed.

Regulatory clarity remains the primary catalyst for this growth. Recent frameworks from bodies like the European Union’s MiCA and the US Federal Reserve’s exploration of digital asset settlement have provided the legal certainty required for large-scale participation. As noted in recent research on tokenized trade assets, the securitization of invoice-based financing through blockchain infrastructure allows for fractional ownership and secondary market trading, effectively unlocking trapped value in global supply chains.

Market interest is reflected in the rising volume of onchain trade finance transactions. While specific aggregate market cap figures for tokenized invoices are still maturing, the trajectory points toward significant integration with traditional banking systems. Institutions are prioritizing infrastructure that ensures compliance and transparency, leveraging smart contracts to automate payment triggers and reduce counterparty risk. This convergence of traditional trade finance principles with blockchain technology is reshaping how global commerce is funded.

To understand the broader market context, it is helpful to look at the performance of related real-world asset (RWA) tokens and the underlying financial instruments driving this sector.

Checklist for evaluating tokenization tools

Choosing the right infrastructure for tokenized trade finance invoices requires more than just checking for blockchain compatibility. You need to verify that the platform can handle the specific regulatory, technical, and liquidity demands of your business. Use this five-point checklist to vet potential vendors before signing contracts.

Ensure the platform supports mandatory identity verification and transaction monitoring. Tokenized invoices often cross borders, so the tool must integrate with KYC/AML providers to prevent illicit flows. Without robust compliance layers, your institution risks severe regulatory penalties and frozen assets.

Tokenized invoices depend on accurate off-chain data feeds. Verify that the platform uses reputable oracles (like Chainlink) to bridge real-world invoice status to the blockchain. If the oracle fails or provides stale data, the token’s value becomes unreliable, breaking the entire trade finance workflow.

Tokenization is only valuable if you can exit the position. Ask vendors about their liquidity pools and connections to secondary markets. A platform with no secondary market creates illiquid assets that are hard to finance or sell, defeating the purpose of faster cash flow.

Demand recent, independent security audits from top-tier firms. Tokenized invoices hold financial value, making them prime targets for exploits. Ensure the codebase is open-source or has undergone rigorous penetration testing to prevent hacks that could drain investor funds or freeze invoice settlements.

Your existing ERP and trade finance systems must communicate seamlessly with the tokenization layer. Check for available APIs and SDKs that reduce development time. If the vendor requires custom coding for every integration, your time-to-market will suffer, and operational costs will spike.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!