What tokenized trade finance invoices actually are

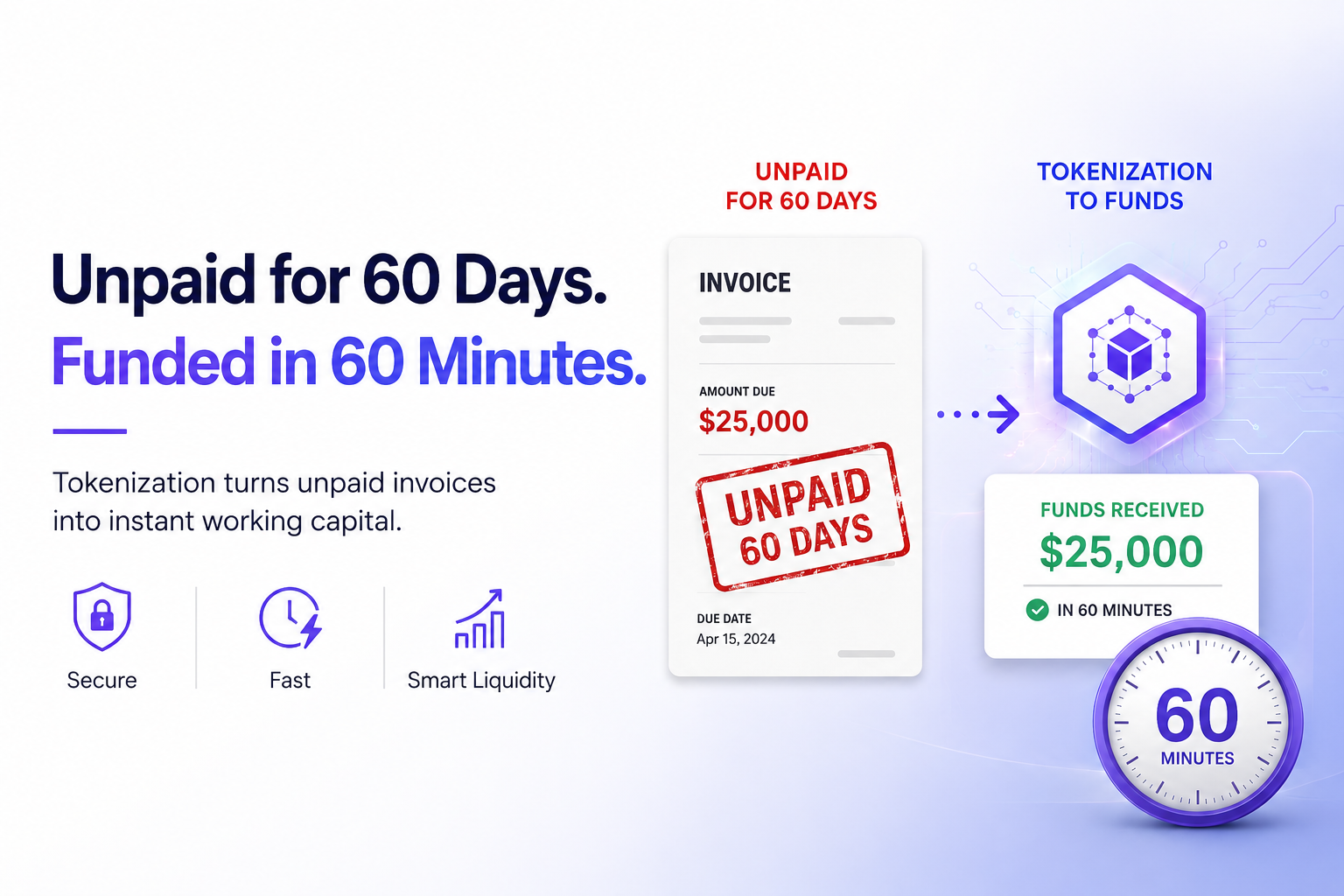

Tokenized trade finance invoices are blockchain-native digital representations of unpaid commercial claims. This process converts specific invoice details—such as the total amount, due date, and buyer-seller identifiers—into a unique digital token on a distributed ledger [1]. This is distinct from simple digitization. A scanned PDF is a static image of a document; a tokenized invoice is a programmable financial instrument with embedded settlement rules and ownership rights.

The core value proposition lies in liquidity and fractional ownership. Traditional trade finance often locks capital for 30 to 90 days while waiting for payment. Tokenization breaks these large invoices into smaller, tradeable units. This allows suppliers to access working capital immediately and enables investors to participate in short-term, asset-backed yields. It transforms a static receivable into a liquid, tradable asset.

By anchoring these financial claims to a blockchain, the infrastructure ensures transparency and reduces counterparty risk. The token serves as a single source of truth for the invoice's status, eliminating the reconciliation delays common in traditional banking corridors. This clarity is what enables the secondary market to function efficiently.

Comparing tokenization infrastructure layers

Building a tokenized trade finance invoice system isn't just about picking a blockchain; it's about selecting a stack that balances settlement speed with regulatory compliance. The infrastructure layer dictates how quickly capital moves, how much legal overhead is required, and how deep the liquidity pool can become. For any Tokenized Trade Finance Invoices guide, understanding these technical differences is essential to choosing the right architecture for your risk profile.

The core infrastructure typically consists of three components: the settlement layer (blockchain), the verification layer (oracles), and the legal wrapper. Public chains offer high liquidity but require complex compliance wrappers. Private or permissioned chains offer faster settlement and lower gas costs but limit investor access. Oracles bridge the gap by feeding real-world invoice data onto the chain, ensuring the token represents a valid, enforceable claim.

To help you evaluate which infrastructure fits your needs, we've broken down the tradeoffs between the most common approaches. The decision often comes down to whether you prioritize speed and privacy or liquidity and transparency.

| Infrastructure Layer | Settlement Speed | Compliance Overhead | Liquidity Depth |

|---|---|---|---|

| Public Blockchain (e.g., Ethereum) | High (10-60 mins) | High (KYC/AML wrappers) | High (Global investors) |

| Permissioned Ledger (e.g., Hyperledger) | Low (Seconds) | Medium (Internal control) | Low (Restricted network) |

| Hybrid Architecture | Medium (T+1) | Medium-High | Medium (Selective access) |

The choice between these layers impacts your operational costs and investor base. Public chains attract a broader range of capital but introduce regulatory friction. Permissioned ledgers are easier to manage internally but struggle to attract external liquidity. A hybrid approach is becoming increasingly popular, using private chains for initial processing and public chains for final settlement to balance both needs.

How the Secondary Market Moves

The secondary market for tokenized trade finance invoices functions as a high-frequency auction house, where liquidity is determined by real-time risk pricing rather than traditional banking relationships. When an invoice is tokenized, it is no longer a static document waiting for maturity; it becomes a liquid asset that can be traded, sliced, and repriced instantly. This shift transforms the invoice from a passive receivable into an active yield-bearing instrument, allowing capital to flow deeper into the supply chain than traditional factoring ever allowed.

Institutional capital drives the bulk of this volume, seeking stable, short-term yields that outperform money market funds while maintaining lower volatility than equities. These investors—ranging from family offices to specialized credit funds—use algorithmic trading bots to assess the creditworthiness of the underlying debtor and the supplier’s historical performance. The result is a market where pricing is granular: a 90-day invoice from a blue-chip retailer might trade at a 4% discount, while a similar invoice from a riskier vendor trades at 8%, reflecting the immediate, data-driven risk assessment.

Retail participation remains limited but is growing as platforms lower entry barriers. Unlike institutional buyers who trade in millions, retail investors often buy fractional shares of tokenized invoices, diversifying across hundreds of small trades to mitigate default risk. This democratization of access creates a broader liquidity pool, but it also introduces different behavioral dynamics. Retail investors are less likely to hold through volatility, potentially causing sharper price swings during market stress compared to the steadier hands of institutional players.

The efficiency of this secondary market relies on the transparency of the token’s metadata. Every trade updates the ledger, providing a clear audit trail of the invoice’s history, including any prior discounts or assignments. This transparency reduces the "lemons problem" often found in traditional trade finance, where buyers hesitate to purchase assets due to information asymmetry. With tokenized trade finance invoices, the risk profile is visible to all participants, enabling faster execution and tighter spreads.

Note: The chart above illustrates general market volatility patterns relevant to trade finance instruments. Tokenized invoice yields are influenced by broader credit market conditions, as reflected in institutional credit spreads.

Ultimately, the liquidity mechanics of tokenized invoices create a more resilient supply chain finance ecosystem. By enabling rapid repricing and secondary trading, the market ensures that suppliers can access working capital when they need it most, while investors gain access to a diversified, transparent asset class. This dynamic equilibrium between institutional depth and retail breadth is what sustains the long-term viability of the tokenized trade finance market.

How to implement tokenized trade finance invoices

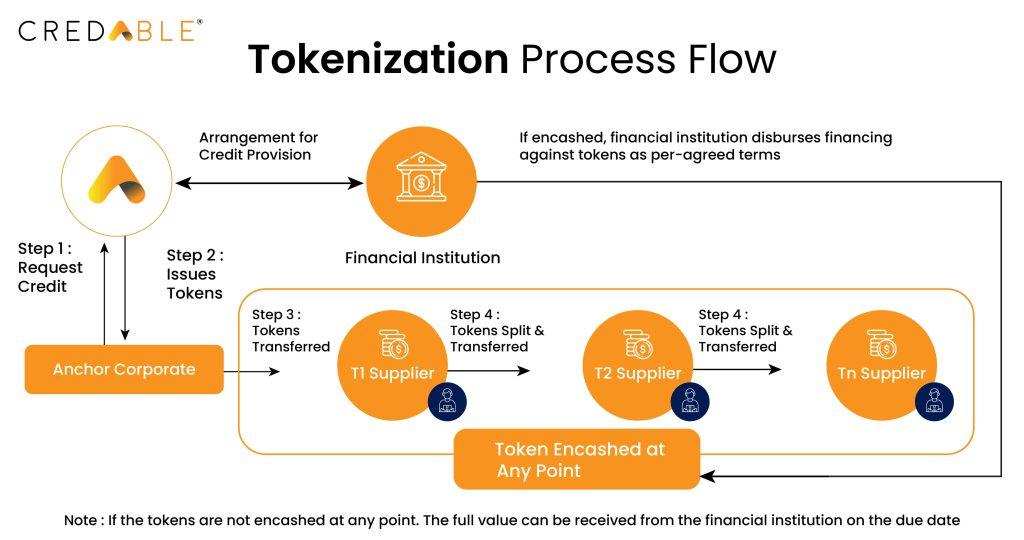

Moving from traditional receivables to a tokenized model requires a structured workflow. The goal is to convert unpaid claims into digital assets that can be financed or traded on secondary markets. This process demands rigorous due diligence and careful partner selection to ensure regulatory compliance and operational efficiency.

Start by isolating the specific invoices you intend to tokenize. Ensure the underlying trade documents are digitized and verified. This step reduces counterparty risk and establishes the asset's baseline value for potential investors.

Choose a provider that supports your jurisdiction's regulatory framework. Look for platforms that offer built-in KYC/AML checks and secure custody solutions. The right infrastructure simplifies the complex legal requirements of issuing digital securities.

Draft the smart contracts and legal wrappers that define ownership rights. This includes specifying how interest is distributed and how defaults are handled. Legal clarity is essential to protect both the issuer and the token holders.

Invite potential investors and liquidity providers to the platform. Conduct thorough due diligence on each participant to maintain the integrity of the pool. This step ensures that only qualified buyers can access the tokenized assets.

Issue the tokens and begin trading. Monitor the performance of the underlying invoices and manage any secondary market activity. Regular reporting and transparent communication with investors are key to maintaining trust and liquidity.

Key risks and compliance considerations

While tokenized trade finance invoices promise liquidity, they introduce a distinct set of vulnerabilities that finance professionals must navigate carefully. The transition from traditional paper-based systems to on-chain assets shifts risk profiles, requiring rigorous oversight of both regulatory frameworks and technical infrastructure.

Regulatory fragmentation

Trade finance operates across borders, yet blockchain regulations remain fragmented. A tokenized invoice issued in one jurisdiction may face conflicting compliance requirements in another. The lack of a unified global standard creates uncertainty around legal enforceability and cross-border settlement. Teams must ensure that smart contracts adhere to local anti-money laundering (AML) and know-your-customer (KYC) rules, which vary significantly by region.

Smart contract vulnerabilities

Code is law, but code can also contain bugs. Smart contracts governing tokenized invoices are immutable once deployed, meaning any flaw in the logic can lead to irreversible financial loss. Audits are essential, but they are not foolproof. The reliance on oracles to feed real-world invoice data onto the blockchain introduces another layer of risk; if the oracle is compromised, the tokenized asset’s value becomes unreliable.

Counterparty and liquidity risk

Tokenization does not eliminate the underlying credit risk of the invoice issuer. If the buyer defaults, the token holder bears the loss. Additionally, while tokenization aims to increase liquidity, secondary markets for trade finance tokens are still nascent. In times of market stress, selling these tokens quickly without significant price slippage can be challenging, exposing investors to liquidity risk that is less pronounced in traditional bank-backed instruments.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!