What tokenized trade finance invoices actually are

Tokenized trade finance invoices are digital representations of unpaid commercial invoices, issued on a blockchain network. Instead of a paper document sitting in a warehouse, the receivable becomes a digital asset—a "token"—that can be tracked, verified, and traded instantly.

This process transforms static trade receivables into liquid digital assets. Companies can use these tokens to collateralize loans for immediate cash or sell them to investors seeking yield. It is a fundamental shift from traditional factoring, where a single financial institution typically buys the invoice at a discount.

The distinction lies in accessibility and speed. Traditional factoring is often a slow, relationship-based process limited to specific banks. Tokenization opens the asset to a broader pool of capital providers, including decentralized finance (DeFi) protocols and institutional investors, who can buy fractions of invoices with greater transparency and lower friction.

By converting outstanding invoices into digital tokens, businesses can unlock working capital without waiting for net-30 or net-60 payment terms. This digital infrastructure reduces the risk of fraud through immutable ledger records and streamlines the verification process for all parties involved.

Key infrastructure layers for onchain trade finance

Tokenizing an invoice isn't just about creating a digital twin; it's about building a bridge between traditional banking systems and blockchain networks. This infrastructure stack ensures that off-chain data—like invoice details and payment terms—is accurately represented and secured on-chain. Without these layers, tokenized trade finance would lack the trust and liquidity required to function at scale.

At the core of this stack are smart contracts. These self-executing agreements automate the lifecycle of the invoice token, from issuance to settlement. They enforce the rules of the trade, ensuring that payments are released only when predefined conditions are met. This automation reduces administrative overhead and minimizes the risk of human error or fraud. For a deeper look at how Chainlink facilitates this data flow, see their guide on invoice tokenization.

Identity verification (KYC/AML) is the gatekeeper of this system. Before any invoice is tokenized, all participants—buyers, sellers, and financiers—must undergo rigorous identity checks. This ensures that the network remains compliant with global financial regulations. Without robust KYC/AML layers, the legal and regulatory risks of tokenized finance would be too high for institutional adoption. The University of Surrey’s research highlights how these tokens seamlessly integrate with legacy systems while maintaining compliance 1.

Oracles serve as the critical link between the real world and the blockchain. They feed real-time data—such as shipping status, invoice verification, and payment receipts—into the smart contracts. This ensures that the token’s value and status reflect the actual state of the trade. Without reliable oracles, the smart contracts would be operating in a vacuum, unable to react to real-world events.

This infrastructure works together to create a secure, transparent, and efficient ecosystem. Smart contracts handle the logic, oracles provide the data, and KYC/AML ensures compliance. Together, they enable the rapid settlement of trade finance, unlocking liquidity for businesses worldwide.

Investor demand and liquidity in tokenized trade

The traditional trade finance market has long been defined by friction. Letters of credit and factoring agreements often sit in silos, locked behind manual verification processes and institutional gatekeepers. For investors, this means high barriers to entry and slow capital deployment. Tokenization changes the geometry of these assets, turning illiquid receivables into programmable instruments that can move across borders and balance sheets with minimal delay.

Investor appetite is shifting because the risk-adjusted returns are becoming clearer. When invoices are tokenized, they are no longer just paper promises; they are data-rich assets with transparent provenance. This transparency allows smaller institutional players and decentralized finance (DeFi) participants to access trade assets that were previously reserved for large banks. The result is a deeper pool of capital chasing the same underlying trade flows.

To understand the practical difference, consider how liquidity and speed compare between the old system and the new tokenized infrastructure. The table below breaks down the structural advantages that are driving this demand.

| Feature | Traditional Trade Finance | Tokenized Invoices |

|---|---|---|

| Settlement Speed | Days to weeks | Minutes to hours |

| Minimum Investment | High ($1M+) | Low (fractional) |

| Transparency | Limited, siloed data | Real-time ledger access |

| Secondary Liquidity | Difficult, high friction | High, automated trading |

This shift toward fractionalization and instant settlement is creating a new asset class for yield-seeking investors. While specific token yields fluctuate with market conditions, the structural efficiency of tokenized trade finance offers a compelling alternative to traditional fixed-income instruments. The liquidity premium is not just theoretical; it is being built into the code of these new financial instruments.

Strategic tools for implementing tokenization

Building a tokenized invoice system requires more than just a blockchain node. You need a stack that handles legal wrappers, KYC/AML checks, and integration with existing ERP systems. The right infrastructure turns unpaid receivables into tradable assets without breaking your current accounting workflow.

Choose a permissioned ledger like Hyperledger or Corda for enterprise control, or a public chain like Ethereum if you need broader investor access. The legal wrapper is critical; it defines how the token represents the underlying invoice debt. Without a clear legal structure, the token is just a digital receipt, not a financial instrument.

Your platform must talk to your ERP (like SAP or Oracle) and your bank’s API. Manual data entry defeats the purpose of tokenization. Look for vendors offering pre-built connectors that pull invoice data directly into the blockchain, ensuring the token’s value is backed by real, verified trade data.

Tokenization doesn’t eliminate credit risk; it just makes it more visible. Use smart contracts to automate payment triggers based on delivery confirmation or time-based milestones. Ensure your platform supports KYC/AML checks for all token holders, especially if you’re opening the pool to deep-tier suppliers or institutional investors.

The goal is to lower financing costs for deep-tier suppliers by leveraging the anchor buyer’s creditworthiness. When selecting a vendor, ask how they handle data privacy and whether they offer secondary market liquidity solutions. This isn’t just about technology; it’s about creating a new financial rails for your supply chain.

-

Verify legal enforceability of tokenized claims

-

Check ERP integration capabilities

-

Assess KYC/AML compliance features

-

Evaluate secondary market liquidity options

Start with a pilot program involving a single supplier or a specific invoice class. This allows you to test the infrastructure and legal framework without disrupting your entire supply chain. Success in tokenization comes from solving specific liquidity bottlenecks, not just adopting blockchain for the sake of innovation.

Real-world examples and use cases

Tokenized trade finance invoices are moving from pilot programs to active marketplaces. Several platforms are already demonstrating how this technology solves the friction of cross-border payments and liquidity constraints.

TradeIX and Supply Chain Finance

TradeIX has integrated invoice tokenization into its supply chain finance ecosystem. By converting invoice rights into digital tokens, the platform allows suppliers to access working capital faster while giving buyers extended payment terms. This dual benefit strengthens supplier relationships and stabilizes the supply chain during cash flow crunches.

C2FO and Digital Liquidity

C2FO uses tokenization principles to digitize payables and receivables. Their platform enables businesses to tokenize invoices, making them tradable assets. This liquidity allows companies to access capital without traditional banking hurdles, reducing the time between invoice issuance and payment from weeks to days.

Komgo and Agricultural Trade

In the agricultural sector, Komgo has pioneered tokenized trade finance for commodities. By tokenizing bills of lading and invoices, the platform reduces fraud and document handling errors. This use case highlights how tokenization brings transparency to high-value, complex trade transactions.

Practical Takeaways

These examples show that tokenized trade finance invoices offer tangible benefits: faster payments, reduced fraud, and improved liquidity. As more platforms adopt these solutions, the trade finance landscape is shifting toward greater efficiency and transparency.

As an Amazon Associate, we may earn from qualifying purchases.

Common Questions About Tokenized Trade Invoices

Tokenized trade finance invoices are still a developing niche, so it is natural to have questions about how they work in practice. Here are the most common questions readers ask about security, regulation, and accessibility.

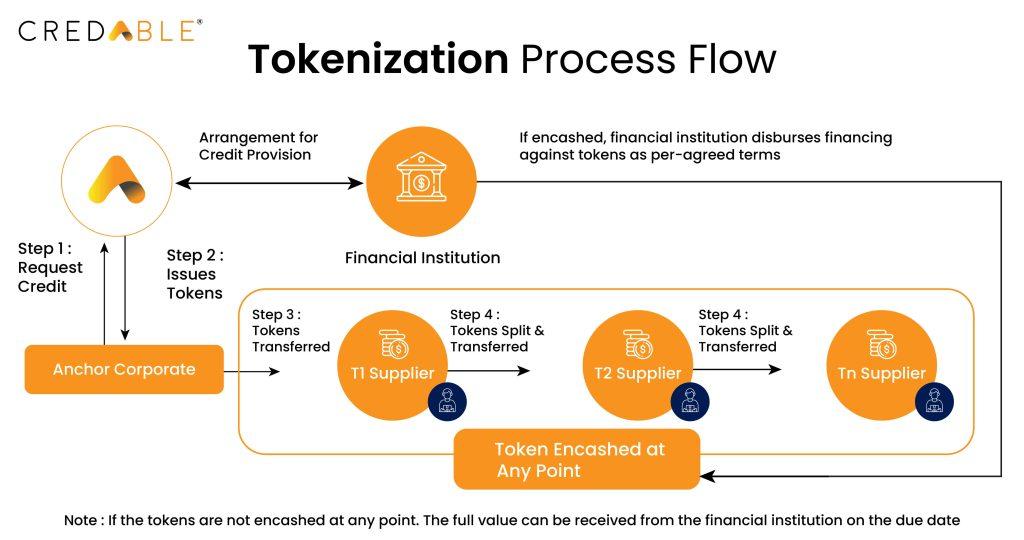

Technical Chart Analysis

Understanding the mechanics of tokenized trade finance requires visualizing the flow of value and data. The following chart illustrates the lifecycle of a tokenized invoice, from issuance to settlement, highlighting the key infrastructure components involved.

No comments yet. Be the first to share your thoughts!