What are tokenized trade finance invoices?

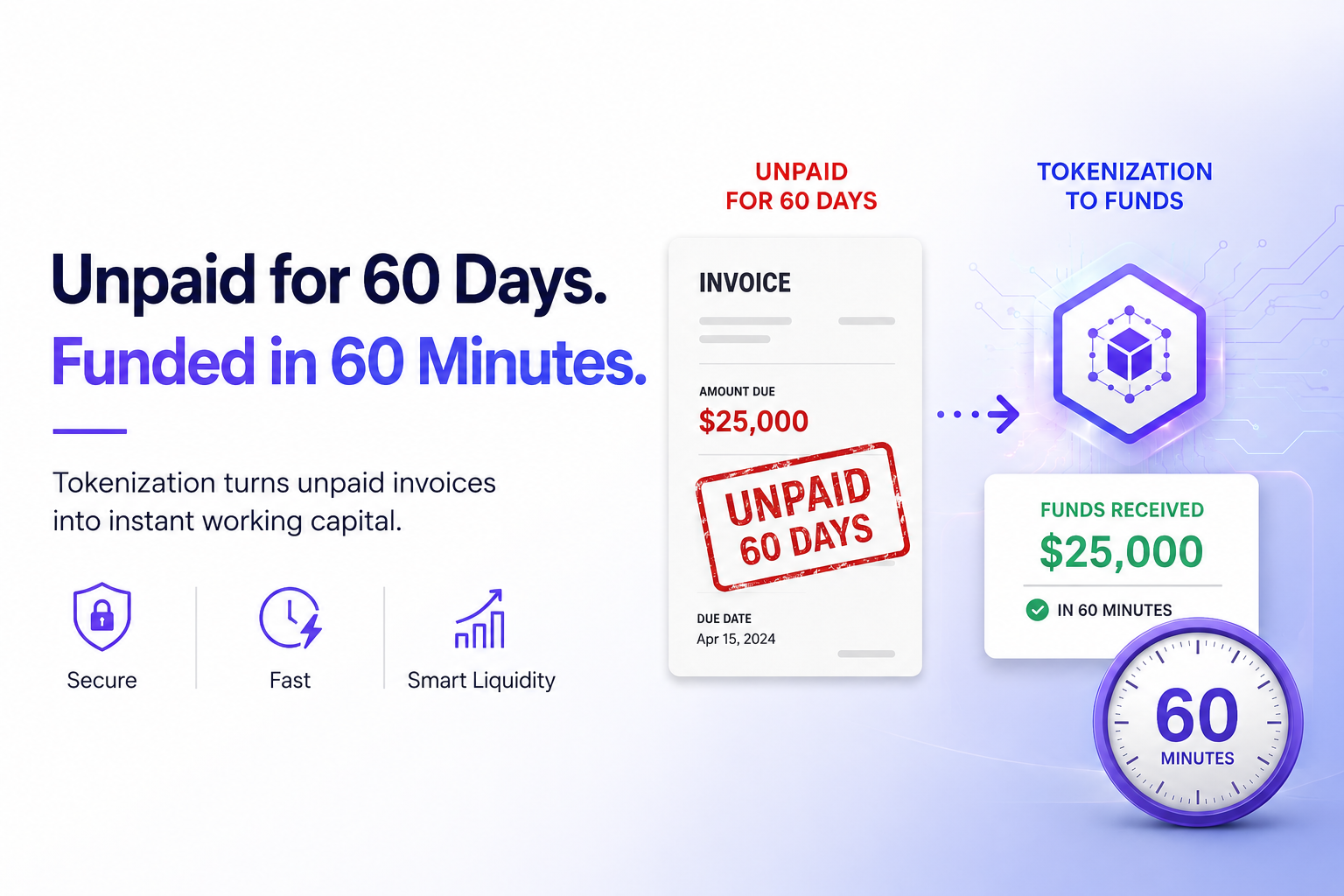

Tokenized trade finance invoices represent unpaid financial claims as digital assets on a blockchain. This process converts traditional receivables into tokens that can be financed, traded, or settled on-chain, offering a distinct alternative to conventional factoring models.

In traditional trade finance, a business sells an unpaid invoice to a factor at a discount to get immediate cash. The relationship is bilateral: the supplier and the factor. Tokenization introduces a programmable layer. The invoice becomes a digital token, often backed by real-world data oracles, which can then be held, traded, or used as collateral in decentralized finance (DeFi) markets or private liquidity pools.

This shift allows for greater liquidity. Instead of waiting for the invoice maturity date or relying on a single financier, tokenized invoices can be fragmented and sold to a broader range of investors. It transforms a static, illiquid asset into a dynamic instrument that can move through the supply chain more efficiently, reducing the friction and time typically associated with cross-border payments and credit verification.

Infrastructure layers for onchain invoices

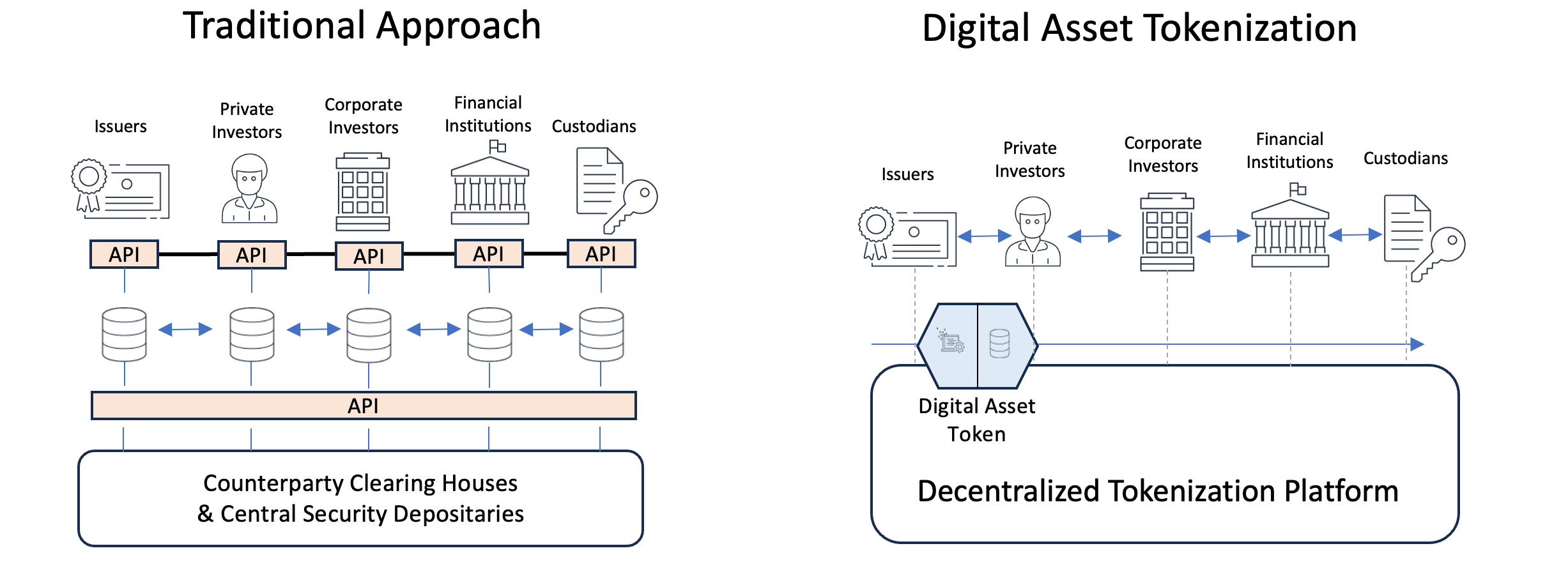

Tokenizing a trade finance invoice requires more than just minting a token. It demands a coordinated stack that bridges off-chain legal claims with on-chain settlement. The infrastructure rests on three pillars: a settlement network, a smart contract standard for the invoice asset, and an oracle layer to verify the underlying trade data.

Settlement and Data Layers

The choice of blockchain network dictates the finality and cost of the invoice token. Enterprise-grade permissioned ledgers like Hyperledger Fabric or Quorum offer privacy for sensitive supply chain data, while public chains like Ethereum provide broader liquidity and composability with decentralized finance (DeFi) protocols. Most modern solutions use a hybrid approach, keeping sensitive commercial documents off-chain while anchoring cryptographic hashes on-chain for immutability.

Oracle networks serve as the critical bridge between the real world and the blockchain. Since an invoice represents a future cash flow, the system must verify that the goods were shipped and the services rendered. Chainlink and similar oracle providers pull verified data from ERP systems, shipping logs, and banking APIs, feeding this information into the smart contract to trigger payments or adjust token status. Without this trusted data feed, the token remains an unverified claim rather than a liquid asset.

Smart Contract Standards

The invoice token itself must adhere to a standard that supports both fungibility and unique attributes. While ERC-20 is common for simple debt instruments, ERC-1400 or ERC-3643 offer more control, allowing for compliance checks, transfer restrictions, and investor whitelisting directly in the contract logic. These standards ensure that the tokenized invoice can be traded, fractionalized, or used as collateral while maintaining regulatory compliance.

Market Context

The infrastructure for tokenized trade finance is evolving alongside broader digital asset markets. Understanding the performance of trade finance-related assets and crypto indices helps contextualize the liquidity and adoption trends in this sector.

Key tools for tokenization and settlement

The shift from paper to digital assets relies on specific infrastructure that handles the entire lifecycle of a tokenized invoice. These platforms act as the bridge between traditional trade finance workflows and blockchain-based settlement, ensuring that unpaid claims can be converted into tradeable digital assets without losing compliance or auditability.

The core of this infrastructure typically involves three layers: issuance, compliance, and secondary marketplaces. Issuance platforms allow corporations or factoring companies to mint invoices as tokens. Compliance layers ensure that these tokens adhere to regulatory standards, such as KYC (Know Your Customer) and AML (Anti-Money Laundering) checks, which is critical for institutional adoption. Finally, marketplaces provide the liquidity needed for investors to buy fractionalized portions of these invoices.

Comparison of major platforms

Different platforms serve different segments of the trade finance ecosystem. Some focus on enterprise-grade issuance for large corporations, while others prioritize liquidity for smaller businesses and investors.

| Platform | Primary Focus | Compliance Features | Target Audience |

|---|---|---|---|

| ONINO | Invoice & Receivable Tokenization | Built-in KYC/AML workflows | Corporations & Factoring Companies |

| Spydra | Blockchain-Powered Trade Finance | Regulatory-ready infrastructure | SMEs & Investors |

| 2Tokens | Invoice Markets | Standardized token frameworks | Investors & Financial Institutions |

These tools are not just about digitization; they are about creating a new asset class. By tokenizing invoices, companies can unlock liquidity that was previously tied up in long payment terms. This process allows multiple investors to fund portions of invoices, increasing liquidity and reducing the reliance on traditional intermediaries.

The choice of platform often depends on the specific needs of the business. Large enterprises may prefer platforms that offer deep integration with existing ERP systems, while smaller businesses might look for platforms that provide easy access to a broad pool of investors. Regardless of the choice, the underlying goal remains the same: to make trade finance faster, more transparent, and more accessible.

Market Strategy for Investors and Issuers

Tokenized trade finance creates a two-sided market where liquidity meets credit risk. For issuers, the strategy centers on moving beyond traditional bank financing to tap into a broader pool of capital. For investors, it offers access to supply chain finance with enhanced transparency and faster settlement cycles.

For Issuers: Streamlining Access to Capital

Issuers—typically large enterprises or financial institutions—use tokenization to unlock working capital trapped in deep-tier supply chains. The primary goal is to reduce the cost of funding and extend payment terms to suppliers without straining the issuer’s balance sheet. By converting invoices into digital tokens, issuers can offer suppliers earlier payment at a discount, effectively creating a secondary market for receivables.

Success requires rigorous on-chain infrastructure. Issuers must ensure that the underlying invoices are legally enforceable and that the smart contracts governing the tokens are audited. This reduces counterparty risk and builds trust with institutional investors who are cautious about regulatory compliance. The result is a more efficient supply chain where even small, deep-tier suppliers can access affordable financing.

For Investors: Balancing Yield and Risk

Investors enter this market seeking yields that often exceed those of traditional fixed-income instruments, while benefiting from the security of underlying trade assets. The key appeal is the visibility into the asset’s lifecycle. Unlike traditional bonds, tokenized invoices allow investors to track the status of the underlying trade in real-time, from shipment to payment.

However, risk management remains critical. Investors must evaluate the creditworthiness of the original debtor (the buyer of the goods) and the operational integrity of the issuer. Diversification across multiple invoices and industries helps mitigate default risk. Additionally, understanding the smart contract’s code and the legal framework governing the token is essential to avoid structural risks.

The Strategic Balance

The market thrives on alignment. Issuers need liquidity; investors need yield. Tokenization bridges this gap by creating a transparent, efficient marketplace. As regulatory frameworks evolve, particularly around digital assets and cross-border payments, the strategic advantage will go to those who can navigate both the technological and legal complexities. For now, early adopters are setting the standard for how trade finance will operate in a digital economy.

Regulatory and security considerations

Tokenized trade finance invoices operate in a high-stakes environment where the margin for error is thin. Unlike traditional paper-based instruments, digital tokens introduce new vectors for failure, making regulatory clarity and technical security the foundation of any viable strategy. You cannot treat tokenization as a mere tech upgrade; it is a fundamental shift in how liability and ownership are recorded and enforced.

The legal status of these tokens varies significantly by jurisdiction. In the United States, the International Trade Administration provides guidance on trade finance basics, but it does not explicitly define the legal standing of blockchain-based invoices. This ambiguity means that while the technology is available, the legal enforceability of a tokenized claim against a counterparty remains untested in many courts. Finance professionals must assume that current frameworks are incomplete and structure contracts accordingly.

Security risks extend beyond simple hacking attempts. The integrity of the underlying ledger is paramount, but so is the security of the off-chain data that anchors the token. If the invoice data stored off-chain is altered or lost, the token becomes worthless or, worse, fraudulent. This "oracle problem" requires robust verification mechanisms and often involves trusted third parties to validate the authenticity of the underlying trade documents.

Compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations is non-negotiable. Tokenized invoices can move faster than traditional wire transfers, increasing the risk of rapid, cross-border fund movement that could be exploited for illicit purposes. Systems must embed identity verification and transaction monitoring directly into the token lifecycle, ensuring that every transfer is traceable and compliant with local financial regulations.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!