What tokenized trade finance invoices are

Tokenized trade finance invoices turn unpaid receivables into digital tokens on a blockchain. This process converts outstanding invoices into digital assets that can be financed, traded, or used as collateral for lending. By digitizing these claims, companies unlock liquidity that was previously locked in long payment terms, creating a more efficient market for short-term working capital.

This mechanism differs significantly from traditional factoring. In traditional factoring, a business sells its invoices to a third-party factor at a discount to get immediate cash. The factor then assumes the risk of collecting payment from the buyer. Tokenization, however, often allows the seller to retain a relationship with the buyer while accessing liquidity through a broader pool of onchain investors or lenders. The token represents a claim on the underlying invoice, but the structure is more flexible and often programmable.

The core value lies in transparency and speed. Because the invoice exists as a token on a distributed ledger, its ownership, status, and payment history are visible to authorized participants in real time. This reduces the friction of due diligence and verification, which are major bottlenecks in traditional trade finance. As noted by Chainlink, this onchain approach enables invoices to be collateralized more easily, bridging the gap between traditional trade receivables and decentralized finance (DeFi) liquidity.

For finance professionals, this means viewing tokenized invoices not just as a new asset class, but as a structural upgrade to how trade credit is managed. It shifts the focus from manual reconciliation and paper-based verification to automated, trustless settlement. This distinction is critical for understanding the strategic implications for treasury management and supply chain financing.

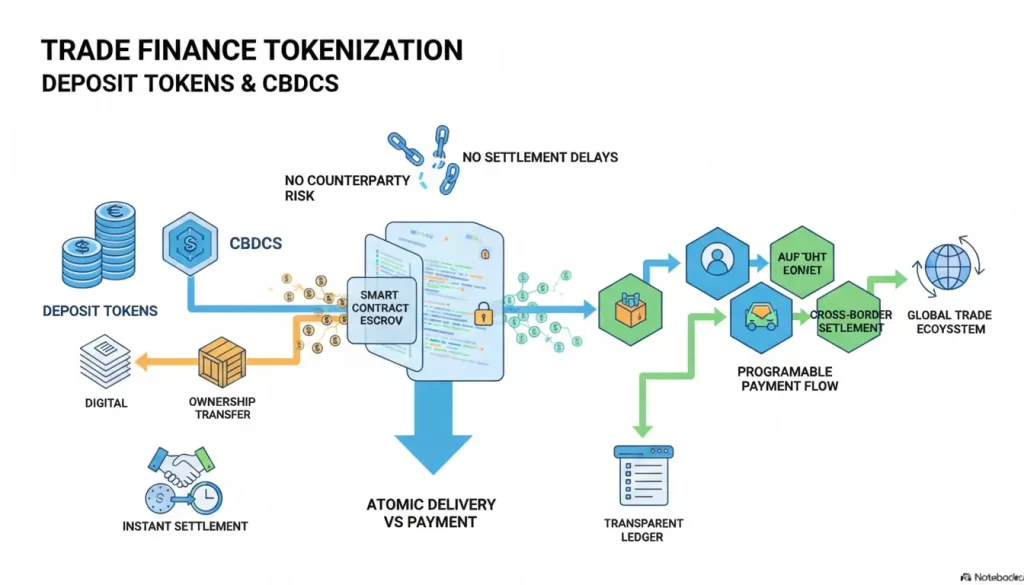

The technical stack behind tokenized trade finance

Tokenized trade finance invoices do not exist in a vacuum. They rely on a precise technical stack that bridges physical trade documents with digital ledger entries. This infrastructure ensures that the token represents a real, verifiable asset rather than a speculative derivative.

At the core of this system are oracles. These networks bridge off-chain invoice data with on-chain smart contracts. They verify that the underlying trade documents—such as bills of lading and commercial invoices—are authentic and have not been altered. Without this verification layer, the token lacks the integrity required for institutional adoption.

Settlement rails provide the liquidity mechanism. Most tokenized invoices are settled in stablecoins to avoid currency volatility during the short-term financing period. This requires smart contracts that support standard token protocols, such as ERC-3643 or ERC-1400, which embed compliance rules directly into the asset’s code. These standards ensure that only verified participants can hold or trade the token.

The convergence of these layers creates a transparent, efficient market. Trade finance participants can access liquidity instantly, while lenders gain real-time visibility into the collateral’s status. This technical foundation transforms a traditionally opaque process into a programmable financial instrument.

Liquidity and secondary market dynamics

Tokenization fundamentally changes how trade finance invoices are funded by breaking them into digital units. Instead of a single institution holding the entire debt, the invoice is split into smaller, tradable tokens. This fragmentation allows both institutional funds and retail investors to provide fractional funding, significantly increasing the pool of available capital.

This shift creates a secondary market for receivables that did not exist in traditional finance. Investors can now buy and sell these tokenized positions with greater ease, improving market depth and reducing the friction typically associated with trade finance. As noted in research on tokenized trade assets, this structure facilitates the securitization of trade instruments, making them more accessible and liquid (ResearchGate, 2024).

The contrast between traditional methods and tokenized receivables is stark. Traditional factoring often involves lengthy negotiations and limited investor access, while tokenization offers near-instant settlement and broader participation. Spydra highlights that this multi-investor model enhances liquidity by allowing multiple parties to fund portions of a single invoice, rather than relying on one buyer (Spydra, 2024).

Traditional Factoring vs. Tokenized Receivables

| Feature | Traditional Invoice Factoring | Tokenized Receivables |

|---|---|---|

| Investor Access | Limited to large institutions | Open to institutional and retail investors |

| Liquidity | Low; assets are illiquid until maturity | High; tokens can be traded on secondary markets |

| Speed | Days to weeks for settlement | Near-instant settlement via blockchain |

| Minimum Investment | High (often $100k+) | Low (fractional ownership possible) |

| Transparency | Opaque; manual reporting | Real-time on-chain data and tracking |

Strategic adoption for supply chain finance

Tokenized trade finance invoices are shifting from experimental pilots to core infrastructure for enterprises seeking to optimize working capital. The business case rests on three pillars: compressed cash conversion cycles, reduced financing costs, and unprecedented transparency for deep-tier suppliers. By moving receivables and payables onto a shared ledger, companies can unlock liquidity that was previously trapped in complex, multi-layered supply chains.

Accelerating working capital cycles

Traditional supply chain finance often relies on bilateral relationships between a buyer and a direct supplier. Tokenization breaks this constraint by enabling the seamless transfer of value across multiple tiers. When an invoice is tokenized, it becomes a digital asset that can be verified, traced, and settled in near real-time. This reduces the friction of manual reconciliation and accelerates the time from invoice issuance to payment, freeing up cash for reinvestment.

Lowering financing costs through transparency

Access to capital is often constrained by information asymmetry. Lenders and investors lack visibility into the true risk profile of deep-tier suppliers, leading to higher interest rates or outright denial of credit. Tokenized invoices provide an immutable record of transaction history and ownership, allowing financial institutions to assess risk more accurately. This enhanced transparency lowers the cost of capital for suppliers, particularly those in emerging markets or smaller industries that traditionally struggle to secure affordable financing.

Extending benefits to deep-tier suppliers

The most significant impact of tokenization is felt at the bottom of the supply chain. Deep-tier suppliers often face long payment terms and limited access to formal financial services. By tokenizing invoices, primary suppliers can extend the benefits of their own creditworthiness to their subcontractors. This creates a more resilient and equitable supply chain, where smaller businesses can access liquidity at rates comparable to their larger counterparts.

Evaluating platform reliability

Adopting tokenization requires careful due diligence. Enterprises must evaluate platforms based on regulatory compliance, oracle reliability, and settlement finality. A robust platform ensures that the digital representation of the invoice accurately reflects the underlying legal obligation and that settlement is irreversible and final. Without these safeguards, the potential benefits of tokenization are undermined by operational and legal risks.

-

Regulatory compliance with local and cross-border financial laws

-

Oracle reliability for accurate data ingestion and verification

-

Settlement finality to ensure irreversible and secure transactions

Market Outlook and Risk Considerations

The transition of trade finance invoices onto the blockchain is no longer a theoretical exercise; it is an active infrastructure build. However, the path to institutional scale is paved with significant regulatory and technical hurdles. For finance professionals, the immediate challenge is not adoption speed, but risk management.

Regulatory frameworks remain fragmented. While bodies like the Basel Committee are reviewing tokenized assets, local enforcement varies wildly. A tokenized invoice valid in one jurisdiction may face liquidity or legal recognition issues in another. This uncertainty requires legal teams to audit smart contract structures before deployment.

Smart contract risk is the second pillar of concern. Unlike traditional banking ledgers, code errors are immutable. Audits are mandatory, but they are not foolproof. Institutional players are demanding multi-sig wallets and formal verification methods to mitigate the risk of exploits.

Despite these headwinds, the trajectory points toward consolidation. Major banks are moving from pilot programs to live production environments. The market is shifting from hype to utility, focusing on efficiency gains in settlement times and working capital optimization.

No comments yet. Be the first to share your thoughts!