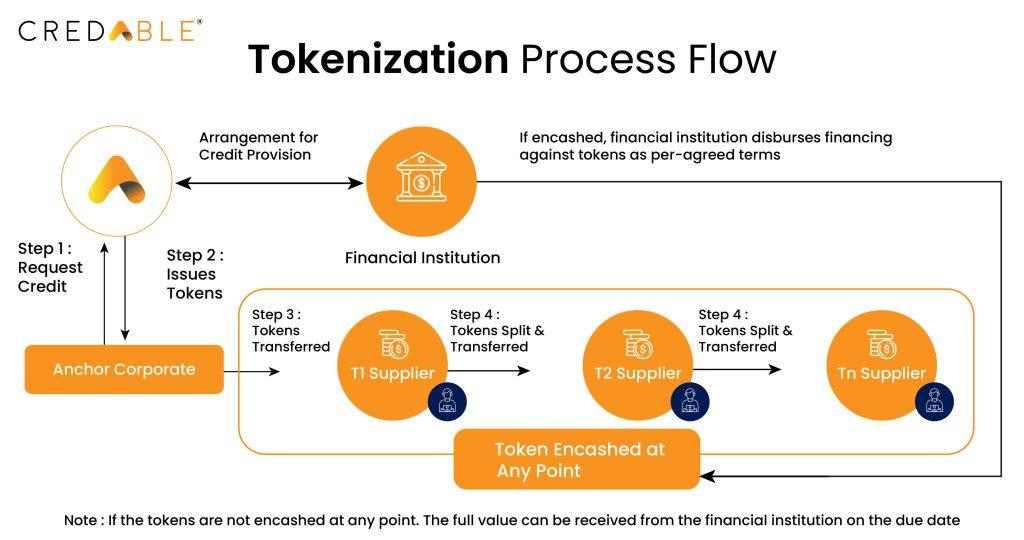

What tokenized trade finance invoices are

Tokenized trade finance invoices are digital tokens representing a claim on specific outstanding receivables. This process converts illiquid accounts receivable into on-chain assets that can be financed, traded, or used as collateral. Unlike traditional factoring, where a business sells its receivables to a single factor at a discount, tokenization allows these claims to be split into fractional units. This model opens the asset class to a broader range of investors, from institutional funds to retail participants, enabling capital to flow directly to trade assets while bypassing intermediary layers.

The core value proposition lies in liquidity and transparency. Recording the invoice on a blockchain makes ownership history and payment terms immutable and verifiable. This reduces due diligence friction and accelerates settlement. Companies access working capital faster, while investors gain exposure to tangible, trade-backed yields often less correlated with broader equity markets.

How the technical stack secures trade finance

Tokenizing an invoice requires bridging traditional commercial paper with blockchain logic. The infrastructure relies on a three-layer stack: data oracles to verify authenticity, smart contracts to enforce terms, and the underlying blockchain to settle transactions.

Oracles: Verifying the source of truth

The oracle network bridges off-chain commercial data with on-chain execution. In trade finance, the oracle must verify invoice existence, shipment confirmation, and buyer acceptance. Chainlink, for instance, provides decentralized oracle networks that pull data from multiple ERP systems, ensuring the tokenized asset reflects the actual trade state rather than a single point of failure. This verification confirms provenance and prevents double-spending, creating a tamper-evident record that smart contracts can trust without manual due diligence.

Smart contracts: Automating enforcement

Smart contracts encode the terms of the trade finance deal, defining payment due dates, interest calculations, and default protocols. Because the code is immutable, parties execute terms without relying on banks or factoring companies. These contracts enable programmability, such as automatically releasing funds upon shipping confirmation or triggering liquidation if a buyer’s credit rating drops. This automation reduces settlement times from weeks to minutes and lowers operational costs.

Blockchain: The settlement layer

The blockchain provides the immutable ledger for token transfers and state changes. For trade finance, networks with high throughput and low fees, such as Polygon or Ethereum L2s, are often preferred. The blockchain ensures the tokenized invoice is unique and traceable, creating a clear audit trail essential for regulatory compliance and institutional trust.

Comparing tokenization models and platforms

The underlying infrastructure dictates settlement speed, regulatory liability, and liquidity access. There is no single "best" model; rather, there are distinct trade-offs between private permissioned ledgers and public blockchains. Private networks offer the control and compliance frameworks traditional banks require, while public chains provide deeper liquidity pools and transparent audit trails.

| Model | Settlement | Compliance | Liquidity Access |

|---|---|---|---|

| Private Permissioned Ledger | T+0 to T+1 | Built-in KYC/AML | Restricted (Institutional) |

| Public Blockchain | Near-instant | On-chain identity required | Open (Retail & Institutional) |

| Hybrid Architecture | T+0 | Off-chain data, on-chain proof | Segmented |

| DLT Consortium | T+1 | Multi-party governance | Interbank only |

Private Permissioned Ledgers

Private permissioned networks, such as those built on Hyperledger Fabric or Corda, are the current standard for large banks. These platforms restrict participation to verified entities, allowing for strict control over data privacy and regulatory compliance. Settlement is fast, often occurring within the same business day (T+0) or next day (T+1), but liquidity is limited to consortium members.

Public Blockchains

Public chains like Ethereum or Solana offer open access, allowing a wider range of investors to fund tokenized invoices. This openness drives higher potential liquidity but introduces complexity in identity management. Compliance must be enforced through on-chain smart contracts or decentralized identity protocols, which can be technically challenging to integrate with legacy banking systems.

Hybrid and Consortium Models

Hybrid architectures keep sensitive data off-chain while recording transaction proofs on-chain, satisfying regulatory data protection laws while leveraging public ledger transparency. Consortium models, often governed by multiple financial institutions, offer a middle ground with shared governance and restricted, interbank liquidity.

Market risks and regulatory limits to account for

Tokenized trade finance invoices sit at the intersection of traditional credit risk and emerging blockchain vulnerabilities. While the technology promises efficiency, the underlying legal frameworks and smart contract logic introduce distinct hazards that institutions must navigate carefully.

Smart Contract and Operational Risk

The integrity of a tokenized invoice depends entirely on the code governing its lifecycle. Smart contract bugs, oracle failures, or governance attacks can freeze assets or enable unauthorized transfers. Unlike traditional banking errors, blockchain transactions are immutable. A flaw in the token standard or the integration layer between the ERP system and the blockchain can lead to significant financial loss with no easy rollback mechanism.

Operational risk also extends to key management. If the private keys controlling invoice issuance or settlement are compromised, the asset is lost. Institutions must implement multi-signature wallets and hardware security modules (HSMs) to mitigate this. In addition, reliance on oracles to feed real-world payment data introduces a single point of failure. If the oracle provides incorrect data regarding a payment default, the token’s value may not adjust correctly, misleading investors and disrupting secondary market trading.

Legal Enforceability and Credit Risk

The legal status of a tokenized invoice varies significantly by jurisdiction. In many regions, it is unclear whether a digital token constitutes a legally enforceable claim against the debtor. Traditional trade finance relies on established legal precedents for bills of exchange and promissory notes. Tokenization often bypasses these structures, creating a "legal gap" where the token holder may not have clear recourse to the underlying asset in the event of default.

Credit risk remains the primary driver of value, but it is compounded by information asymmetry. In traditional supply chain finance, lenders often have established relationships with buyers and suppliers. In tokenized ecosystems, especially those involving deep-tier payables, lenders may face difficulty verifying the authenticity of the invoice or the creditworthiness of the distant supplier. Research indicates that traditional supply chain finance theories, focused primarily on bilateral relationships, provide limited guidance in understanding these network effects (SSRN, 2023). Without robust due diligence and transparent data sharing, the risk of fraud or double-spending increases, particularly if the same invoice is tokenized on multiple platforms.

Regulatory Fragmentation

Regulatory uncertainty is perhaps the most significant barrier to widespread adoption. Trade finance is inherently cross-border, involving multiple jurisdictions with differing rules on securities, money transmission, and data privacy. A tokenized invoice issued in the EU may be classified as a security, while the same asset in the US might be treated as a commodity or a simple contract. This fragmentation creates compliance headaches for institutions operating globally.

Regulators are increasingly scrutinizing stablecoins and asset-backed tokens. The Bank for International Settlements (BIS) and other central banks have highlighted the need for clear guidelines on the custody, issuance, and settlement of tokenized assets. Until a harmonized regulatory framework emerges, institutions must navigate a complex web of local laws, often requiring bespoke legal structures for each transaction. This lack of standardization increases costs and slows down the adoption of tokenized trade finance solutions.

Strategic adoption for 2026

Entering the tokenized trade finance market requires a disciplined approach. The infrastructure is maturing, but the risk of protocol failure or regulatory misalignment remains. Businesses and investors must move from observation to structured integration, treating tokenization as a strategic layer rather than a speculative asset.

1. Audit existing trade finance workflows

Start by mapping your current invoice and letter of credit processes. Identify bottlenecks where liquidity is trapped due to manual verification or fragmented data. Tokenization solves for speed and transparency, not for broken processes. If your underlying documentation is inconsistent, tokenizing it will only accelerate errors.

2. Evaluate platform compliance and custody

Not all tokenized invoice platforms are created equal. Prioritize platforms that integrate with traditional banking rails and offer clear custody solutions. Look for providers that have passed third-party security audits and maintain clear regulatory standing in key jurisdictions. The goal is to access the efficiency of blockchain without assuming unmanaged counterparty risk.

3. Start with a pilot program

Avoid scaling immediately. Select a single, low-risk trade finance instrument, such as a short-term receivable from a trusted partner, and tokenize it on a testnet or private ledger. This allows you to stress-test the settlement logic and user interface without exposing significant capital. Success in a pilot validates the operational fit before broader deployment.

4. Diversify across instruments and regions

Once the pilot proves viable, expand your exposure. Tokenized trade finance offers access to a variety of instruments, including invoices, credit letters, and receivables across different regions and industries. This diversification mitigates the risk associated with any single counterparty or geographic market, creating a more resilient portfolio.

5. Monitor market liquidity and pricing

Liquidity in tokenized trade finance is still evolving. Keep a close watch on secondary market trading volumes and pricing spreads. Use live market data to understand how these assets perform under stress. The following chart provides context for broader market trends that often influence trade finance liquidity.

Due diligence checklist

Before committing capital or integrating a new platform, verify these core requirements:

-

Regulatory Alignment: Does the platform comply with local securities and trade laws?

-

Custody Solution: Who holds the private keys, and is insurance coverage in place?

-

Smart Contract Audit: Has the code been audited by a reputable third-party firm?

-

Exit Strategy: Is there a clear mechanism for redeeming tokens for fiat currency?

-

Counterparty Risk: Have the underlying trade partners been vetted for financial stability?

No comments yet. Be the first to share your thoughts!