The shift from factoring to tokenization

Traditional trade finance has long relied on factoring, a process where businesses sell their unpaid invoices to a third party at a discount to access immediate cash. While this provides liquidity, it introduces significant friction. Intermediaries—banks, factor companies, and clearinghouses—take cuts at every stage, and the settlement process can take days or weeks. This legacy model is opaque, expensive, and often inaccessible to smaller enterprises that lack the credit history to secure favorable terms.

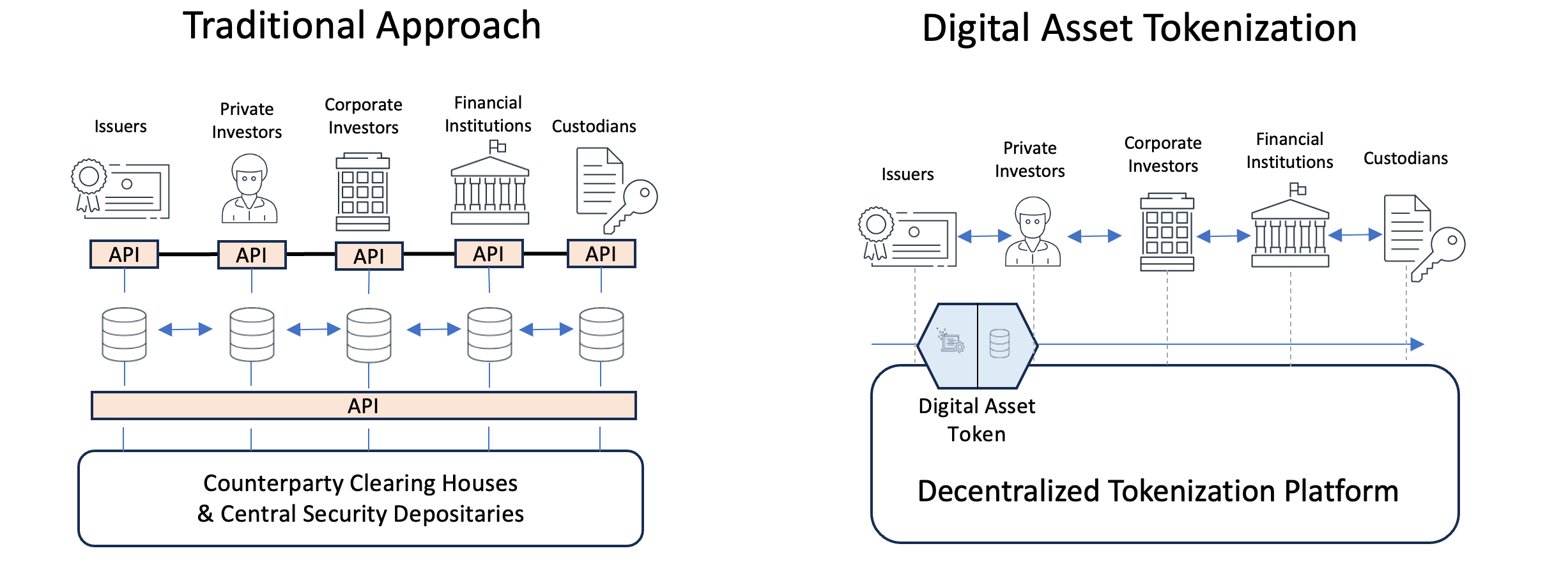

Tokenized trade finance invoices infrastructure changes this dynamic by converting illiquid receivables into digital assets on a blockchain. Instead of a single institution holding the risk, tokenization allows these invoices to be fractionalized and distributed among a broader pool of investors. This process, often referred to as Supply Chain Finance (SCF) tokenization, transforms a static claim into a liquid, tradable instrument. The result is a more efficient market where capital can flow directly from investors to businesses, bypassing the traditional gatekeepers.

The core value proposition lies in efficiency and transparency. By moving onto a blockchain, the lifecycle of an invoice—from creation to payment—becomes immutable and visible to all authorized parties. This reduces the need for manual reconciliation and lowers the risk of fraud. For companies, it means faster access to working capital. For investors, it offers exposure to real-world assets (RWA) with yields that often outperform traditional fixed-income products, all while maintaining the security of distributed ledger technology.

As we move toward 2026, the infrastructure supporting this shift is maturing. We are seeing a clear transition from experimental pilots to production-ready platforms that integrate with existing ERP systems. This isn't just about digitizing paper; it's about re-engineering the financial plumbing of global trade. The following chart illustrates the broader market context for tokenized real-world assets, reflecting the growing institutional interest in this space.

Core components of the infrastructure

Tokenized trade finance invoices rely on a specialized technical stack that bridges traditional legal obligations with blockchain efficiency. The system rests on three pillars: verified data inputs, standardized ownership logic, and instant settlement rails. Without these integrated layers, tokenization remains a theoretical exercise rather than a functional financial instrument.

Oracle feeds for invoice verification

Blockchain networks cannot natively verify real-world documents. Oracle feeds act as the bridge, pulling invoice data from legacy Enterprise Resource Planning (ERP) systems and banking platforms onto the ledger. This step is critical for preventing fraud; the token is only as valid as the underlying commercial transaction it represents.

For trade finance, oracles must validate not just the invoice amount, but also the delivery status and the creditworthiness of the counterparty. This requires trusted data sources that can handle the complexity of international trade documentation, ensuring that the digital token accurately reflects the physical asset or service.

Smart contract standards for fractional ownership

Once verified, invoices are tokenized using smart contract standards that define how ownership is split and managed. Standards like ERC-3643 or proprietary enterprise frameworks allow a single invoice to be divided into fractional tokens, enabling smaller investors to participate in high-value trade finance.

These contracts automate the lifecycle of the invoice. They handle interest accrual, payment distribution, and compliance checks (such as KYC/AML) automatically. When the buyer pays, the smart contract executes the transfer of value to token holders, reducing the need for manual reconciliation and intermediary fees.

Settlement layers: CBDCs and stablecoins

The final component is the settlement layer, which determines how value moves between parties. Central Bank Digital Currencies (CBDCs) and regulated stablecoins are emerging as the preferred rails for tokenized trade finance due to their speed and finality.

Research from the University of Surrey highlights how CBDCs and Distributed Ledger Technology (DLT) enable the tokenization of invoices, transforming them into digital assets that can be seamlessly settled. This combination reduces settlement times from days to seconds, freeing up working capital for businesses. The choice between CBDCs and stablecoins often depends on regulatory jurisdiction and the specific liquidity needs of the trade participants.

Comparing tokenization platforms

The infrastructure layer for tokenized trade finance invoices is no longer a monolith. Three providers—Spydra, ONINO, and Zoniqx—dominate the conversation, each carving out a distinct niche in how digital trade receivables are created, managed, and settled. Choosing the right platform depends less on hype and more on your specific liquidity needs and regulatory footprint.

Spydra positions itself as a bridge between traditional trade finance and digital assets. Their platform focuses on tokenizing trade assets to allow multiple investors to fund portions of invoices or receivables. This fractional ownership model is designed to increase liquidity for buyers who might otherwise be locked out of short-term financing. By reducing intermediaries, Spydra aims to lower the friction costs associated with cross-border trade payments.

ONINO takes a more procedural approach, offering tools specifically designed to tokenize invoices and trade receivables as digital assets. Their focus is on the conversion process: taking unpaid claims and turning them into tradable instruments. This makes ONINO particularly attractive for companies looking to integrate tokenization directly into their existing accounts receivable workflows without overhauling their entire financial stack.

Zoniqx approaches the problem from a supply chain transparency angle. While their technology supports invoice tokenization, their primary value proposition lies in streamlining payment processes while enhancing security and visibility across the entire transaction lifecycle. For organizations where audit trails and supply chain integrity are as important as liquidity, Zoniqx offers a more holistic view of the trade finance ecosystem.

| Platform | Primary Focus | Liquidity Model | Target Audience |

|---|---|---|---|

| Spydra | Fractional ownership of trade assets | Multi-investor funding pools | Institutional investors, trade finance houses |

| ONINO | Invoice and receivable tokenization | Direct asset conversion to digital tokens | SMEs, corporate finance departments |

| Zoniqx | Supply chain transparency and payments | Streamlined payment processes with security | Supply chain managers, logistics providers |

The choice between these platforms often comes down to risk tolerance and operational complexity. Spydra’s model requires a more sophisticated investor base but offers deeper liquidity pools. ONINO is easier to implement for companies already dealing with high volumes of invoices. Zoniqx is best for firms where the physical movement of goods and the digital movement of money need to be perfectly synchronized.

Strategic risks and regulatory hurdles

Building tokenized trade finance invoices infrastructure requires navigating a landscape where legal enforceability often lags behind technological capability. While tokenization transforms invoices into secure, verifiable, and instantly tradable digital assets, the underlying legal frameworks vary significantly across jurisdictions.

The primary risk lies in the recognition of tokenized claims as valid legal instruments. In many markets, the link between the digital token and the underlying receivable is not yet fully established in case law. This creates counterparty risk: if a borrower defaults, can the token holder actually seize the underlying asset or enforce payment through traditional courts? Without clear legal precedents, the "token" may be viewed as a speculative derivative rather than a direct claim on trade debt.

Regulatory bodies are still defining how these assets fit into existing financial regulations. The Basel Committee on Banking Supervision and local central banks are examining whether tokenized receivables qualify as high-quality liquid assets (HQLA). Until clear guidelines are issued, institutions must assume a higher capital charge for these assets, which can erode the efficiency gains promised by tokenization.

Also, smart contract risk remains a critical vulnerability. Unlike traditional paper invoices, tokenized claims are bound by code. A bug in the tokenization protocol or the oracle feeding trade data to the blockchain can lead to irreversible errors. In a high-stakes trade finance environment, this technical risk translates directly into financial loss.

To mitigate these risks, leading infrastructure providers are adopting a "legal-first" approach. This involves embedding legal opinions directly into the token’s metadata and using multi-signature wallets for any settlement actions. By aligning technology with legal reality, tokenized trade finance invoices infrastructure can move from experimental pilot to mainstream adoption.

Implementation Checklist for Tokenized Trade Finance Invoices Infrastructure

Adopting tokenized trade finance invoices infrastructure requires a methodical evaluation of legal, technical, and liquidity factors. This workflow helps enterprises plan around the complexities of converting unpaid claims into secure, verifiable digital assets.

Begin by assessing the regulatory landscape. Tokenization changes the legal nature of receivables, so ensure compliance with local securities laws and banking regulations before proceeding.

Evaluate the underlying distributed ledger technology. Verify that the platform offers robust security protocols, interoperability with existing ERP systems, and transparent settlement mechanisms.

Determine if sufficient investor demand exists. Tokenized assets rely on secondary markets, so confirm that there are active participants willing to fund portions of these invoices.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!