What Are Tokenized Trade Finance Invoices?

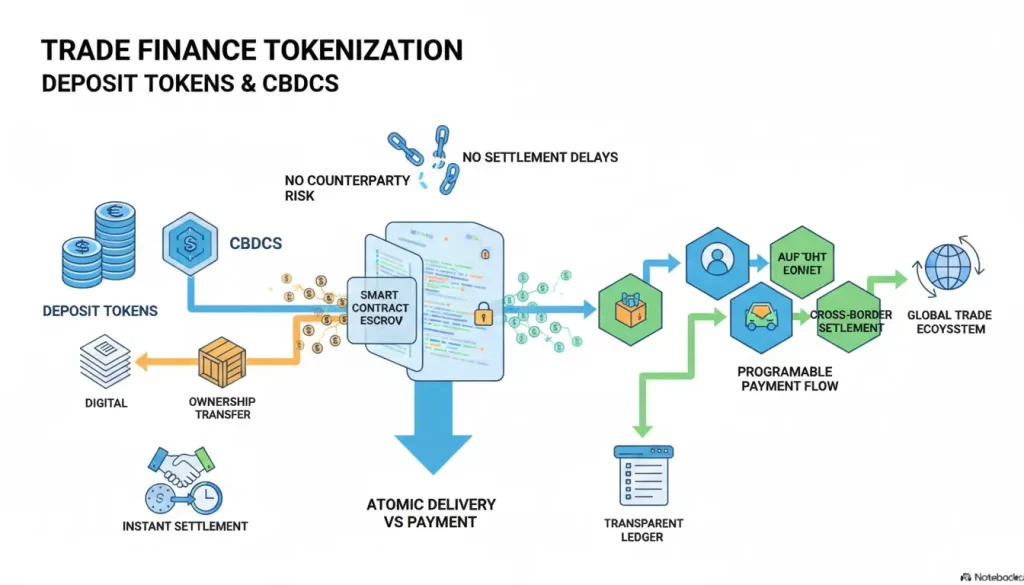

Tokenized trade finance invoices represent a distinct asset class that bridges traditional receivables with onchain liquidity. At its core, invoice tokenization is the process of converting outstanding commercial invoices into digital tokens on a blockchain. This transformation allows companies to collateralize unpaid claims, turning illiquid assets into tradable instruments.

Unlike traditional factoring, where a single financial institution often holds the entire claim, blockchain infrastructure enables fractionalization. This means a single invoice can be split into smaller digital shares, allowing a broader pool of investors to participate. The result is a more liquid market where credit claims can be traded, settled, and collateralized with greater speed and transparency than legacy paper-based systems allow.

The underlying technology creates a verifiable, immutable record of the invoice’s existence and status. This reduces the friction typically associated with verifying trade receivables, making it easier for businesses to access working capital. By moving these financial instruments onchain, the market is shifting from opaque, relationship-based lending to transparent, data-driven credit infrastructure.

Liquidity mechanics for receivables

Tokenized trade finance invoices introduce new liquidity dynamics by separating the asset from the traditional banking relationship. In traditional factoring, liquidity is constrained by the balance sheet capacity of the factor. Onchain, liquidity is determined by the depth of capital providers willing to purchase fractionalized shares of the invoice.

This shift allows for continuous price discovery. Instead of a static discount rate negotiated between a supplier and a bank, the price of a tokenized invoice fluctuates based on real-time supply and demand, the credit profile of the debtor, and the remaining tenor of the receivable. This dynamic pricing mechanism ensures that capital is allocated more efficiently across the market.

However, this liquidity is not frictionless. It depends heavily on the reliability of the underlying legal structure and the technological integrity of the platform. If the legal link between the token and the invoice is weak, or if the platform experiences technical downtime, liquidity can vanish instantly. Investors must therefore assess not just the credit quality of the invoice, but the operational resilience of the tokenization platform.

Risk layers in tokenized invoices

Tokenized trade finance invoices promise efficiency, but they introduce distinct risk layers that traditional factoring does not carry. Investors must assess counterparty default, smart contract vulnerability, and regulatory uncertainty to understand the true exposure. This guide breaks down these risks to help you assess whether tokenized invoices fit your portfolio.

Counterparty and structural risk

The foundational risk remains the same as in traditional trade finance: the buyer’s ability to pay. However, tokenization adds complexity. If the token is backed by a real-world invoice, the investor still relies on the underlying commercial relationship. A default by the buyer triggers a loss, regardless of the blockchain’s efficiency. Additionally, the issuer of the token may face insolvency, separating the digital asset from the underlying claim. This structural risk requires rigorous due diligence on both the originator and the buyer.

Smart contract vulnerability

Tokenized invoices live on code. Smart contracts automate payments and transfers, but they are also susceptible to bugs, exploits, and logic errors. A vulnerability in the contract code could lead to frozen assets or unauthorized transfers. Unlike traditional banking systems, where errors can often be reversed, blockchain transactions are immutable. This means that a successful exploit can result in permanent loss of capital. Investors should prioritize platforms with audited code and established security protocols.

Regulatory uncertainty

The regulatory landscape for tokenized assets is still evolving. Different jurisdictions treat digital tokens differently, creating legal ambiguity around ownership, enforcement, and dispute resolution. If a token is deemed a security, it may fall under stricter regulations, limiting liquidity and investor access. Conversely, if it is treated as a commodity, enforcement mechanisms may be weaker. This uncertainty can impact the enforceability of the underlying invoice in court. Investors need to understand the legal framework governing the specific tokenization platform they use.

To contextualize these risks, it helps to compare tokenized invoices with traditional factoring. The table below highlights key differences in liquidity, speed, and transparency.

| Feature | Traditional Factoring | Tokenized Invoices |

|---|---|---|

| Liquidity | Low (institutional only) | High (retail access possible) |

| Speed | Days to weeks | Near real-time |

| Transparency | Limited (private ledger) | High (public blockchain) |

Who Moves the Needle in Tokenized Trade Finance

The market for tokenized trade finance invoices isn't dominated by a single entity. Instead, it functions as a multi-layered ecosystem where distinct participants play specific roles. Understanding who controls the flow of capital and data is essential for any Tokenized Trade Finance Invoices guide aiming to map the competitive landscape.

Issuers and Originators

At the top of the chain are the issuers—typically supply chain finance providers, banks, or large corporates. They originate the underlying trade assets, such as accounts receivable or letters of credit, and convert them into digital tokens. These entities hold the primary risk and control the initial supply of tokens entering the market. Their credibility directly influences investor confidence, as the token's value is tethered to the real-world asset's performance.

Liquidity Providers

Bridging the gap between issuers and investors are liquidity providers. These can be institutional investors, hedge funds, or specialized DeFi protocols seeking yield from short-term trade assets. They provide the capital necessary to purchase these tokenized invoices, ensuring that issuers can access working capital quickly. Their participation drives market depth, allowing for smoother transactions and tighter spreads.

Technology Platforms and Intermediaries

The infrastructure layer consists of technology platforms that enable the tokenization process. These firms develop the blockchain protocols, smart contracts, and oracle systems that verify the authenticity of the underlying invoices. They also often provide the marketplace where issuers and liquidity providers connect. Reliable technology is critical; any failure in data verification or smart contract execution can undermine the entire trust model.

Regulatory and Compliance Bodies

While not direct market participants in the trading sense, regulatory bodies shape the environment in which these tokens operate. They define the legal status of digital assets, anti-money laundering (AML) requirements, and cross-border payment regulations. Compliance with these frameworks is often baked into the smart contracts themselves, ensuring that only verified participants can trade these tokens.

Due diligence checklist for investors

Tokenized trade finance invoices offer liquidity, but they inherit both traditional credit risk and new on-chain vulnerabilities. A rigorous due diligence framework is essential to separate viable opportunities from speculative noise. This checklist provides a concrete, actionable framework for evaluating tokenized invoice opportunities, focusing on legal structure, underlying asset quality, and platform security.

Confirm that the underlying invoice is legally binding and that the token represents a direct claim on the receivable. Without clear legal recourse in the event of default, the token is merely a speculative instrument. Ensure the issuing entity holds clear title to the invoice and that the tokenization contract explicitly maps the digital token to the physical or digital original debt instrument.

Analyze the creditworthiness of the debtor (the buyer) rather than just the seller. Tokenization often pools invoices, so understand the diversification of the portfolio. Look for transparent data on payment history, debtor concentration, and industry exposure. High-quality receivables from investment-grade buyers significantly reduce the risk of default, making the tokenized asset more resilient.

Examine the platform’s smart contracts for independent audits by reputable firms. Look for evidence of bug bounties, multi-signature wallets for treasury management, and clear protocols for handling oracle failures. The security of the tokenized invoice is only as strong as the weakest link in its digital infrastructure. A single vulnerability can lead to total loss of capital.

Understand how you can exit the position. Check the depth of the secondary market, the frequency of trades, and the spread between buy and sell orders. Illiquidity is a major risk in tokenized assets; ensure there are clear mechanisms for price discovery and that the platform facilitates efficient trading without excessive slippage.

By systematically addressing these areas, you can assess the complexities of tokenized trade finance with greater confidence. Always prioritize transparency and legal clarity over yield promises.

No comments yet. Be the first to share your thoughts!