What tokenized trade invoices actually are

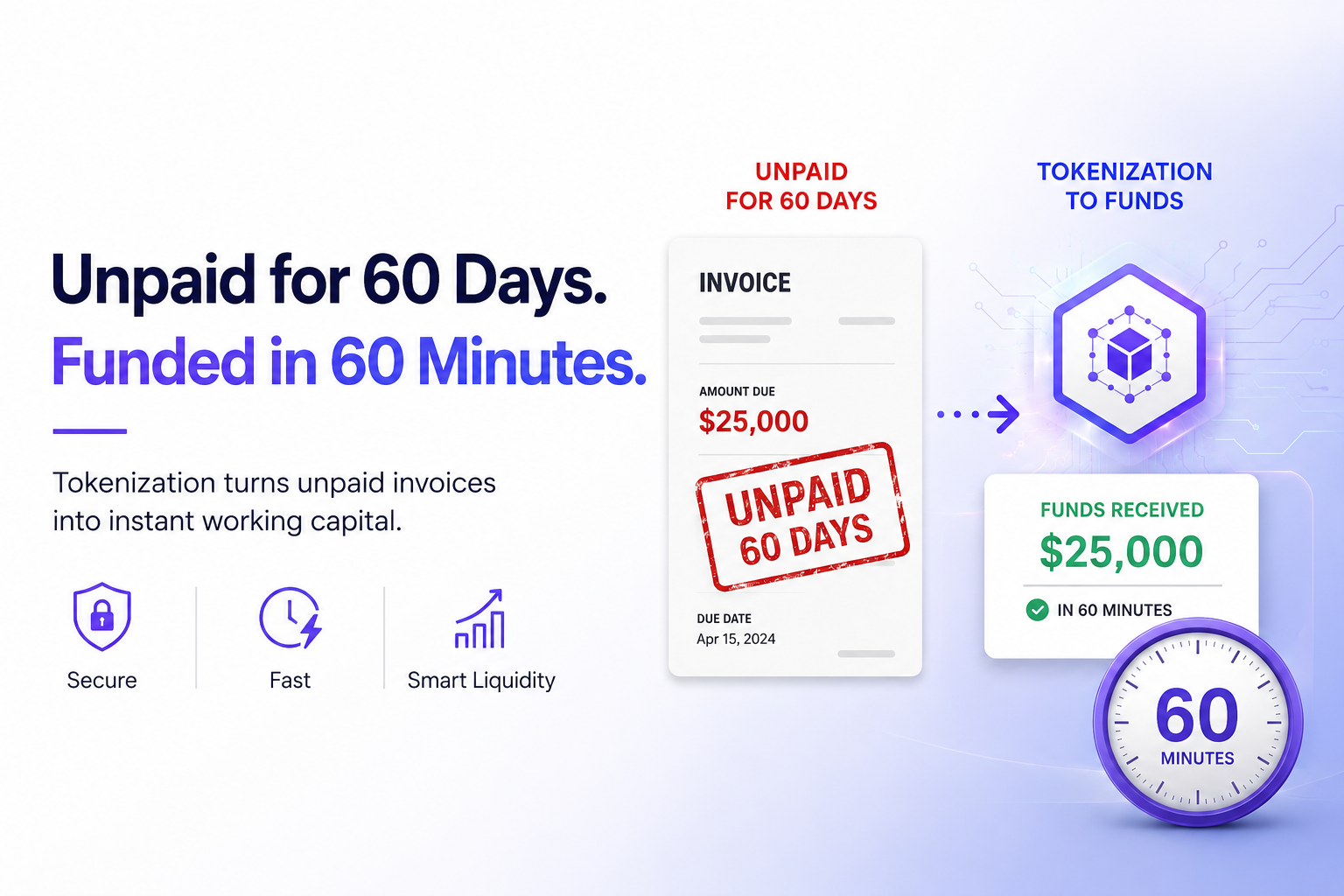

Tokenized trade invoices are unpaid financial claims represented as digital tokens on a blockchain. Instead of a static PDF or paper document sitting in an accounting system, the invoice becomes a dynamic digital asset. This conversion allows companies to finance or trade their receivables with greater speed and transparency than traditional methods allow.

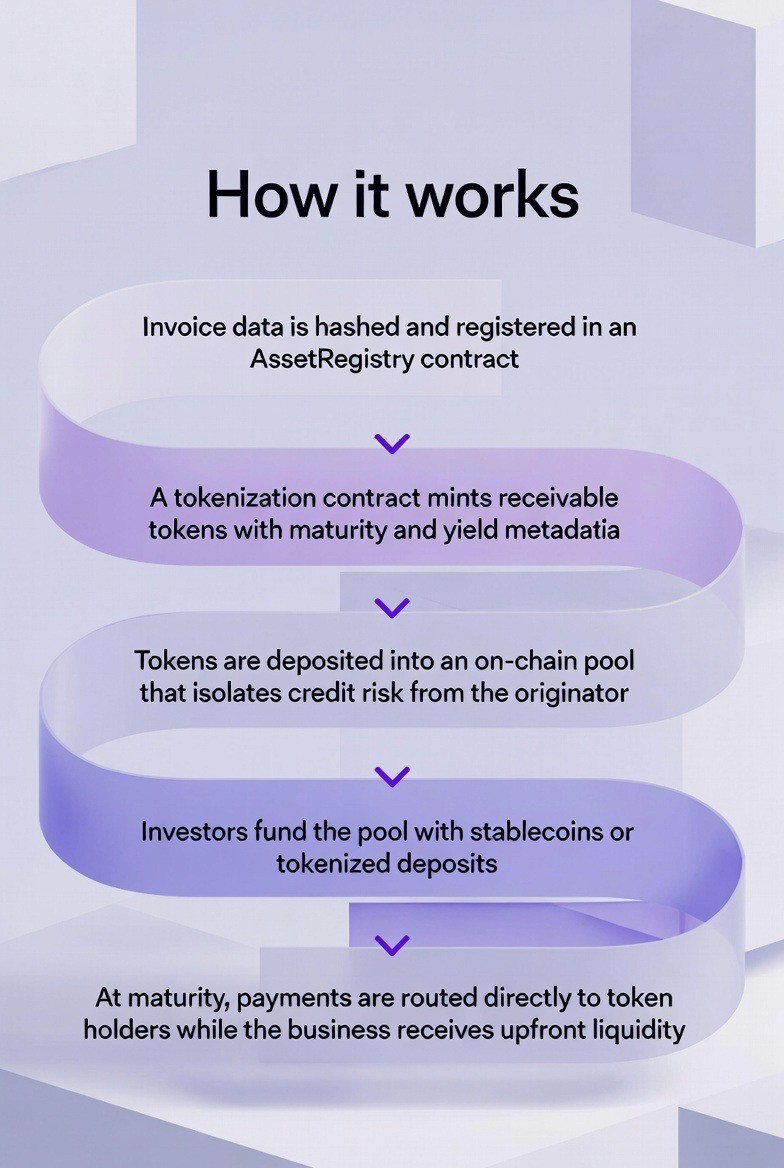

The mechanism works by locking the original invoice data into a smart contract. This contract mints a corresponding token that proves ownership and tracks the payment status in real time. If the buyer pays the invoice, the smart contract automatically updates the token’s status or settles the payment to the token holder. This eliminates the need for manual reconciliation and reduces the risk of double-spending or fraud.

Unlike traditional factoring, where a company sells its invoice to a factor at a discount to get immediate cash, tokenization opens the invoice to a broader pool of liquidity. Investors can buy these tokens directly, often at more competitive rates than banks offer. The digital nature of the asset also makes it easier to split into smaller fractions, allowing smaller investors to participate in trade finance markets that were previously reserved for large institutions.

This shift from paper-based claims to onchain assets is not just a technological upgrade; it is a fundamental change in how trade finance operates. By making invoices liquid and transparent, tokenization reduces the friction that has long slowed down global trade.

The infrastructure powering onchain credit

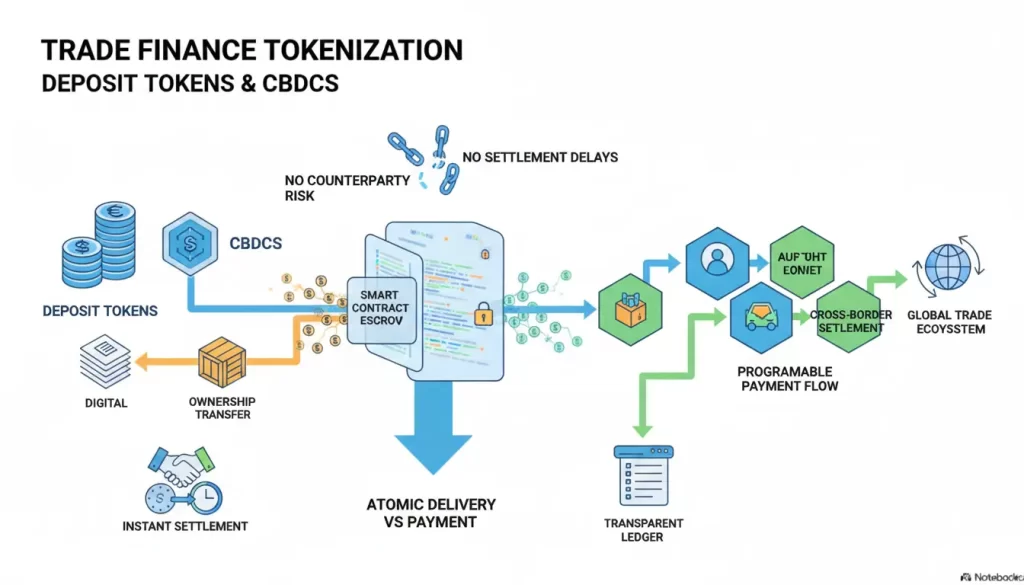

Tokenizing an invoice isn't just about moving a PDF onto a ledger. It requires a coordinated stack of blockchain layers, oracle networks, and smart contract standards to ensure the digital token accurately reflects a real-world financial claim. Without this infrastructure, a tokenized invoice is just a speculative asset with no underlying value.

The foundation is the blockchain layer itself. Most trade finance tokens settle on high-throughput networks like Ethereum or specialized L2s (such as Base or Arbitrum) that offer low fees and finality. These chains provide the immutable ledger where the token’s ownership history is recorded. The choice of chain often depends on whether the platform prioritizes EVM compatibility for developer access or specific regulatory compliance features.

However, the blockchain only sees on-chain activity. To link the token to reality, you need an oracle network like Chainlink. Oracles verify off-chain data—such as invoice maturity, credit scores, and shipping documents—and feed this information into the smart contract. This "proof of reality" is what prevents the token from becoming a detached derivative. Without reliable oracles, the token cannot prove that the underlying invoice is valid, unpaid, or due for settlement.

Finally, the smart contract standard dictates how the token behaves. While ERC-20 is common for fungible debt, ERC-1400 or ERC-3643 are often preferred for security tokens because they embed compliance rules directly into the token’s logic. These standards allow for features like whitelisting, transfer restrictions, and automated dividend distribution, ensuring that only verified participants can hold or trade the tokenized invoice.

Top tools and platforms for tokenization

The infrastructure for tokenized trade finance has matured from experimental pilots to production-ready platforms. For finance professionals evaluating these tools, the choice isn't just about blockchain technology—it's about integration depth, target audience fit, and regulatory compliance. The landscape splits clearly between solutions built for large enterprises with complex supply chains and those designed for SMEs seeking immediate liquidity.

| Platform | Primary Focus | Target Audience | Key Integration |

|---|---|---|---|

| Molten Networks | Invoice factoring marketplace | SMEs | ERP & accounting software |

| TradeGo | Supply chain finance | Large enterprises | Banking APIs & ERP |

| Onino | Invoice tokenization engine | Banks & Fintechs | Custom API integration |

| Pedex | B2B invoice financing | SMEs | Direct payment gateways |

Molten Networks

Molten Networks operates as a marketplace specifically designed to connect SMEs with invoice financing. Their platform tokenizes unpaid invoices, making them accessible to a broader pool of investors. This approach significantly reduces the cost of capital for small businesses compared to traditional factoring. The platform integrates directly with major accounting software, allowing for automated invoice verification and settlement.

TradeGo

TradeGo focuses on the enterprise side of the spectrum, offering a comprehensive supply chain finance platform. It enables large corporations to extend their payment terms while providing their suppliers with early payment options. The platform leverages blockchain to create transparent, immutable records of trade transactions. This transparency reduces fraud risk and streamlines the reconciliation process for finance teams managing complex global supply chains.

Onino

Onino provides a white-label tokenization engine that allows banks and financial institutions to build their own invoice tokenization platforms. This solution is ideal for traditional financial institutions looking to enter the tokenized asset market without building infrastructure from scratch. Onino handles the complex regulatory and technical requirements, enabling clients to launch compliant tokenized invoice products quickly.

Pedex

Pedex specializes in B2B invoice financing for SMEs, offering a streamlined process for converting invoices into digital assets. Their platform emphasizes speed and simplicity, allowing businesses to access cash within hours rather than days. Pedex integrates with payment gateways to facilitate seamless transactions, making it an attractive option for businesses that prioritize liquidity over complex supply chain management.

Strategic advantages for deep-tier suppliers

Tokenized trade finance invoices fundamentally alter the liquidity equation for suppliers further down the supply chain. Traditionally, deep-tier suppliers—often small and medium-sized enterprises (SMEs)—relied on their direct buyers' creditworthiness to secure financing. This created a bottleneck where working capital was trapped, inaccessible, or prohibitively expensive to unlock. Tokenization removes this friction by converting receivables into digital assets that can be traded on secondary markets, effectively decoupling financing access from the supplier's immediate position in the hierarchy.

The most immediate benefit is a significant reduction in financing costs. Traditional factoring services typically charge fees based on the perceived risk of the end buyer and the time value of money, often resulting in rates that erode thin manufacturing margins. By tokenizing invoices, the risk profile is more accurately priced through market mechanisms rather than blanket institutional spreads. This allows deep-tier suppliers to access working cash at rates closer to the primary buyer's credit rating, rather than their own, which is often weaker due to smaller scale and limited collateral.

Beyond cost, tokenization opens access to a broader, more diverse pool of investors. Instead of relying on a single bank or factoring company, tokenized assets can be fractionalized and sold to a global network of institutional and private investors seeking short-term, trade-backed yields. This diversification of capital sources provides suppliers with greater stability and flexibility. If one investor segment tightens its lending criteria, others can step in, ensuring that cash flow remains uninterrupted. This liquidity is not just a convenience; it is a strategic tool that allows deep-tier suppliers to invest in growth, manage payroll, and fulfill orders without the constant pressure of delayed payments.

This shift represents a move from static, relationship-based financing to dynamic, market-driven liquidity. For deep-tier suppliers, this means their invoices become active, tradable instruments rather than passive claims on future payment. The result is a more resilient supply chain where capital flows more freely to where it is needed most, empowering smaller players to operate with the financial agility of much larger corporations.

Key Risks and Security Considerations

Tokenized trade finance invoices are only as trustworthy as the infrastructure backing them. While the technology offers speed, it introduces specific vulnerabilities that traditional banking systems did not face. Understanding these risks is essential for any strategy aiming to deploy capital in this space by 2026.

The most immediate threat lies in the smart contract layer. A bug in the code governing the token can lead to irreversible loss of funds. Unlike traditional accounts, there is no customer service to reverse a transaction. You must verify that the smart contract has undergone rigorous auditing by reputable firms and that the oracle sources feeding real-world invoice data are reliable. If the oracle is compromised, the token’s value becomes detached from the actual invoice.

Regulatory uncertainty remains another significant hurdle. The legal status of digital tokens representing real-world assets varies widely across jurisdictions. In some regions, the enforcement of rights attached to a tokenized invoice may be unclear if the issuer defaults. This legal ambiguity can complicate recovery efforts, making due diligence on the legal structure of the tokenization platform just as important as its technical security.

Finally, the risk of "garbage in, garbage out" cannot be overstated. If the underlying real-world asset—the unpaid invoice—is fraudulent or already disputed, the tokenized version will be worthless. The blockchain ensures the token moves correctly, but it cannot verify the legitimacy of the initial data entry. Rigorous off-chain verification processes are critical to maintaining the integrity of the entire system.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!