What tokenized trade finance invoices actually are

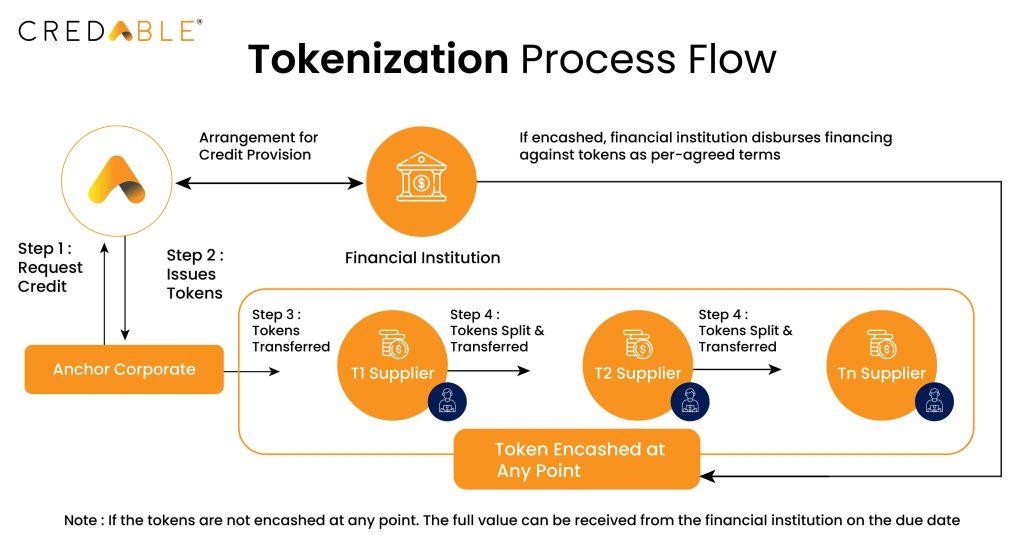

Tokenized trade finance invoices are unpaid commercial claims represented as digital tokens on a blockchain. This process transforms a standard PDF invoice into a programmable asset that can be financed, traded, or settled on-chain. Unlike simple digital copies of paper documents, these tokens carry the underlying financial claim as a native object, enabling direct verification of ownership and payment status.

The distinction lies in the data structure. Traditional digital invoices remain static files stored in email or accounting software. Tokenized invoices exist as entries in a distributed ledger, where every transfer or pledge is recorded immutably. This creates a single source of truth for the asset’s lifecycle, reducing the friction of manual reconciliation and third-party verification.

This infrastructure shift matters because it unlocks liquidity for trade receivables. By converting invoices into tradeable tokens, businesses can access financing markets that were previously inaccessible or too costly. The token acts as a bridge between the physical trade event and the digital financial system, allowing for faster settlement and broader investor participation.

Mapping the tokenization infrastructure

Tokenizing trade finance invoices is not just about moving money; it is about moving data. The technical stack required to make this work relies on three interconnected layers: smart contracts for execution, oracles for data verification, and interoperability protocols for legacy integration. Without this triad, an invoice remains a static PDF. With it, the invoice becomes a liquid, programmable asset.

The Oracle Layer: Bridging Reality and Blockchain

Smart contracts cannot see the real world. They only execute code based on inputs they receive. For invoice tokenization, the critical input is proof of shipment, bill of lading, or payment status. This is where oracles come in. They act as trusted data feeds, pulling off-chain information and verifying its integrity before passing it to the blockchain.

In trade finance, the risk of "garbage in, garbage out" is high. An oracle must verify that the invoice data matches the underlying trade documents. Chainlink, for example, provides decentralized oracle networks that can aggregate data from multiple sources to ensure accuracy. This prevents a single point of failure from corrupting the tokenized asset. The oracle effectively becomes the digital notary, stamping the blockchain with verified reality.

Smart Contracts: The Execution Engine

Once data is verified, smart contracts handle the tokenization logic. These self-executing agreements define the rules of the invoice token: who can transfer it, when it matures, and how interest is calculated. They automate the lifecycle of the trade finance instrument, reducing the need for manual reconciliation.

The contract must be rigorous. It needs to handle fractional ownership, allowing multiple investors to hold portions of a single invoice. It must also manage the settlement process, automatically transferring funds to the invoice originator upon verified completion of the trade. This automation reduces administrative overhead and accelerates the time to liquidity.

Interoperability: Connecting Legacy Systems

Trade finance is deeply rooted in legacy systems like SWIFT and ERP platforms. Tokenization infrastructure must bridge this gap. Interoperability layers allow data to flow between traditional banking networks and blockchain environments. This ensures that banks and traders can interact with tokenized invoices without abandoning their existing workflows.

Market Context: Trade Finance Liquidity Indicators

The health of the tokenized trade finance sector is often reflected in the stability and liquidity of the underlying digital assets used for settlement. Monitoring major stablecoins and trade finance indices provides insight into the liquidity depth and market sentiment driving these innovations.

Strategic Questions for Infrastructure Adoption

As institutions evaluate these technical stacks, several strategic questions emerge regarding security, compliance, and scalability.

How tokenized invoices differ from traditional factoring

Traditional invoice factoring has long been the go-to for SMEs needing quick cash, but it comes with friction. Factoring companies buy your invoices at a steep discount, often charging fees that range from 1% to 5% of the invoice value, plus interest. The process is manual, requiring extensive documentation and credit checks, which can take days or even weeks to settle. This delay and cost structure often makes factoring prohibitive for smaller businesses or those with thinner margins.

Tokenized trade finance invoices change this dynamic by bringing the process onchain. Instead of relying on a single factoring company, tokenized invoices are converted into digital assets that can be traded or financed across a decentralized network. This opens up liquidity to a broader range of investors, not just specialized financial institutions. The result is often faster access to capital and lower costs, as the tokenization platform automates many of the verification and settlement steps that traditionally slow down the process.

The following comparison highlights the key differences between these two models.

| Feature | Traditional Factoring | Tokenized Invoices |

|---|---|---|

| Settlement Speed | 3-10 business days | Near-instant to 24 hours |

| Cost Structure | 1-5% discount fee + interest | Lower platform fees + interest |

| Accessibility | Limited to vetted institutions | Open to broader investor base |

| Documentation | Heavy manual verification | Automated smart contract verification |

| Liquidity Source | Single factoring company | Decentralized investor network |

Liquidity shifts and fractional access

Tokenization fundamentally alters the liquidity profile of trade receivables by breaking down large, illiquid assets into tradeable units. Traditionally, accessing trade finance required significant capital commitment and lengthy due diligence, effectively limiting the market to institutional players. By tokenizing invoices, platforms enable fractional ownership, allowing smaller investors to participate in high-value trade finance instruments.

This shift democratizes access while simultaneously increasing market depth. Multiple investors can fund portions of a single invoice, dispersing risk and creating a more resilient secondary market. As noted by Spydra, this structure reduces the need for traditional intermediaries, streamlining the flow of capital from investor to exporter.

The impact on liquidity is measurable. Fractional tokens can be traded more frequently than the underlying physical goods or services, creating a dynamic pricing mechanism that reflects real-time supply and demand. This enhanced liquidity helps exporters get paid faster, while investors gain exposure to a diversified asset class with historically low correlation to traditional equity markets.

How to Implement Tokenized Invoices

Adopting tokenized trade finance requires a structured approach that bridges blockchain infrastructure with existing enterprise workflows. The goal is to convert invoice rights into digital tokens without disrupting current operations.

Before technical implementation, verify that your jurisdiction recognizes digital tokens as valid legal instruments for debt settlement. Consult the International Trade Administration’s guidelines on trade finance to ensure your token structure meets regulatory standards for cross-border transactions.

Choose a blockchain platform that supports interoperability with traditional banking rails. Your partner must provide clear governance models and audit trails, ensuring that tokenized invoices remain traceable from origin to payment.

Map your existing ERP invoice data to the new tokenized structure. Use API connectors to sync invoice details, ensuring that the digital token accurately reflects the underlying commercial transaction without manual data entry errors.

Launch a limited pilot with a small group of suppliers and buyers. Test the end-to-end flow: invoice creation, tokenization, transfer, and redemption. Measure settlement times and cost savings against your baseline.

Gradually expand the network to include more participants. Implement real-time monitoring dashboards to track token liquidity and compliance status, adjusting parameters as the network grows.

KeyTakeaways items=["Verify legal recognition of tokens before build","Ensure ERP interoperability via APIs","Start with a controlled pilot group"]

No comments yet. Be the first to share your thoughts!