What tokenized trade finance invoices actually are

Tokenized trade finance invoices are digital representations of off-chain receivables. Instead of holding a paper PDF or a legacy database entry, a company converts an unpaid invoice into a token on a blockchain. This process turns a static claim on future payment into a dynamic, programmable asset that can be held, traded, or used as collateral.

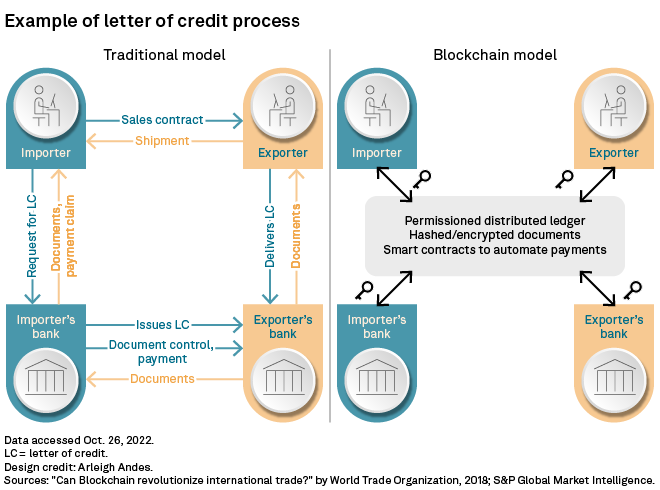

The distinction between this model and traditional factoring is structural. In traditional factoring, a business sells its invoice to a factor (usually a bank or specialized lender) at a discount. The factor assumes the risk of non-payment and handles the collection. The relationship is bilateral, opaque, and bound by the operating hours of the financial institutions involved.

Tokenization changes the infrastructure. The invoice becomes a smart contract on a public or permissioned ledger. This programmability allows for automated compliance checks, real-time status updates, and fractional ownership. An invoice can be split into smaller units, allowing multiple investors to fund a single trade finance deal. Settlement is no longer limited to T+2 banking days; it can occur nearly instantly, provided the underlying blockchain network permits it.

This shift from a private ledger relationship to an on-chain asset class reduces friction. It replaces manual verification with cryptographic proof of ownership and debt obligation. For market participants, this means greater liquidity for receivables and more granular risk management for investors. The asset itself remains tied to the real-world commercial transaction, but its lifecycle is now governed by code rather than paperwork.

The infrastructure behind on-chain receivables

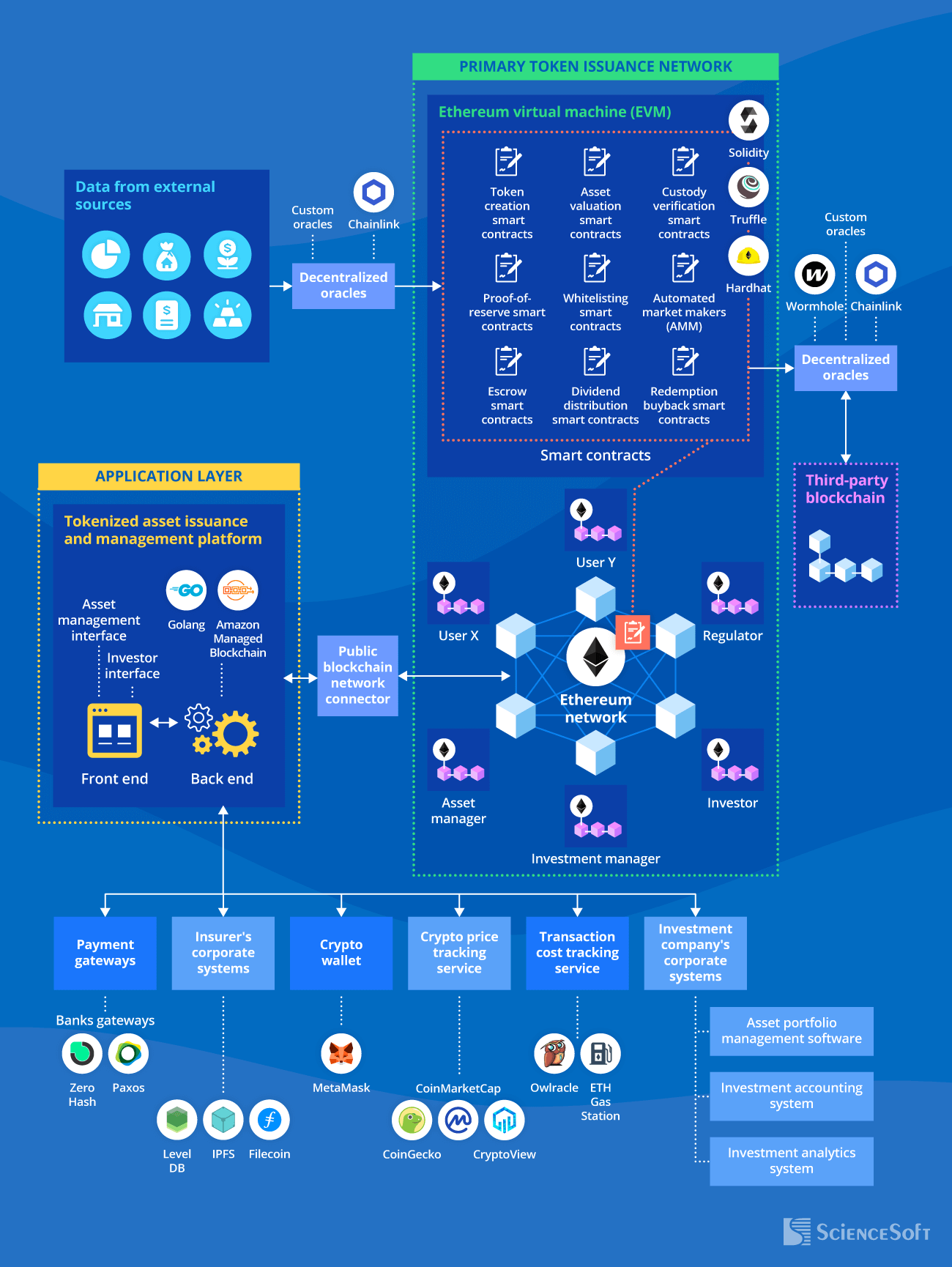

Tokenizing trade finance invoices isn't just about moving data onto a ledger; it requires a coordinated stack of blockchain networks, oracle feeds, and stablecoin rails to function. The process converts outstanding invoices into digital tokens, allowing them to be used as collateral or settled directly. Without this technical foundation, the promise of instant liquidity remains just that—a promise.

The blockchain layer provides the immutable record of ownership. When an invoice is tokenized, its terms and payment history are locked into smart contracts. This eliminates the need for manual reconciliation between banks, suppliers, and buyers. However, a blockchain is only as good as the data it records. This is where oracles come in. They bridge the gap between traditional banking systems and the blockchain, feeding real-time invoice status and payment confirmations into the smart contract. If the oracle data is stale or incorrect, the tokenized asset becomes worthless or, worse, fraudulent.

Settlement speed depends heavily on the stablecoin infrastructure. Unlike traditional wire transfers that take days, tokenized invoices can be settled in minutes using stablecoins pegged to fiat currencies. This reduces counterparty risk and frees up working capital for businesses. The combination of immutable ledgers, trusted oracles, and fast stablecoin rails creates a new standard for trade finance efficiency.

Liquidity and yield for institutional investors

Tokenized trade finance invoices are shifting from experimental pilots to a recognized asset class because they solve the liquidity mismatch that has long plagued invoice financing. Traditional invoice factoring locks capital into illiquid, bilateral contracts with high administrative overhead. Tokenization breaks these receivables into standardized digital tokens, allowing investors to enter and exit positions with the speed of a securities trade rather than the pace of a bank loan.

For institutional portfolios, the primary attraction is diversification. Trade finance yields are driven by commercial payment cycles, not stock market sentiment. This creates a low-correlation return stream that can stabilize broader portfolio volatility. As tokenization infrastructure matures, the ability to access this uncorrelated yield becomes a structural advantage rather than a niche speculation.

The market dynamics are still forming, but the trajectory is clear. Early adopters are building the plumbing—smart contract standards, oracle feeds for payment verification, and secondary market liquidity pools. This infrastructure is what transforms a simple debt obligation into a tradable financial instrument.

To understand the mechanical shift, it helps to compare the traditional model with the tokenized approach. The differences in cost, speed, and accessibility are stark.

| Feature | Traditional Factoring | Tokenized Invoices |

|---|---|---|

| Settlement Time | 5-10 business days | T+0 to T+1 |

| Minimum Investment | $50,000 - $100,000+ | $100 - $1,000 |

| Cost Structure | 1.5% - 3% per month | 0.5% - 1.5% per month |

| Liquidity | Locked until maturity | Secondary market trading |

| Transparency | Opaque bilateral contracts | On-chain ledger visibility |

This comparison highlights why institutional interest is accelerating. The reduction in friction allows for tighter risk management and more efficient capital deployment. Investors are no longer just buying debt; they are accessing a liquid, transparent market for real-world commercial activity.

Regulatory hurdles and credit risk management

Tokenized trade finance invoices sit at the intersection of traditional credit underwriting and blockchain compliance. While the technology promises liquidity, the underlying assets remain subject to stringent regulatory frameworks. Market participants must navigate a dual-layer risk profile: the digital infrastructure's security and the traditional counterparty's solvency.

Compliance is non-negotiable. Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols must be embedded directly into the token issuance process. Unlike traditional trade finance, where checks occur offline, on-chain tokenization requires automated identity verification at the smart contract level. Failure to integrate these standards exposes platforms to severe legal penalties and loss of institutional trust.

Credit risk assessment has evolved but not disappeared. Tokenization does not erase the risk of invoice default; it merely makes the risk more transparent. Lenders still rely on rigorous credit models to evaluate the buyer's ability to pay. The key difference lies in data accessibility. With real-time ledger updates, credit models can incorporate live payment behavior, potentially reducing information asymmetry between lenders and borrowers.

However, over-reliance on algorithmic scoring introduces new vulnerabilities. If the underlying data feeds are manipulated or the smart contract logic is flawed, the credit assessment becomes invalid. Therefore, robust due diligence remains essential. Investors should treat tokenized invoices as secured loans, not risk-free digital assets. The technology enhances efficiency, but it does not eliminate the fundamental need for sound credit analysis.

Strategic steps for market entry

Entering the tokenized trade finance market requires moving beyond pilot projects to institutional-grade infrastructure. Success depends on selecting partners who understand both blockchain settlement and traditional trade compliance, while ensuring your legal framework can handle cross-border disputes.

Before building, determine if you are issuing invoices, providing liquidity, or facilitating settlement. Each role requires different technical integrations. For issuers, focus on automating the invoice-to-token lifecycle. For investors, prioritize platforms with deep pools of trade receivables. Define your risk appetite early to select the right chain and settlement layer.

Not all blockchain providers understand letters of credit or bills of lading. Look for partners who have existing relationships with banks, freight forwarders, and insurers. They should offer APIs that integrate with your existing ERP or supply chain finance systems. Avoid platforms that treat trade finance as a generic asset class; specialized knowledge reduces operational friction.

Tokenized invoices are legal instruments. Ensure your smart contracts align with local securities laws, anti-money laundering (AML) regulations, and know-your-customer (KYC) requirements. Work with legal counsel experienced in digital assets to draft terms that are enforceable in court. This includes defining ownership rights, redemption mechanisms, and dispute resolution protocols.

Trade finance involves high-value transactions across borders. Integrate identity verification tools that can handle corporate entities and beneficial owners. Your platform must screen participants against sanctions lists and monitor for suspicious activity. This step is non-negotiable for institutional adoption and protects your platform from regulatory penalties.

Start with a small group of trusted partners to test the end-to-end workflow. Validate that invoices are tokenized, traded, and settled correctly. Monitor settlement times, cost savings, and user experience. Once the pilot proves successful, expand to more participants and larger invoice volumes. Gradual scaling reduces risk and allows you to refine your processes.

By following these steps, you can build a sustainable and compliant presence in the tokenized trade finance market. Focus on infrastructure, legal clarity, and strategic partnerships to drive long-term value.

| Role | Key Focus | Tech Priority |

|---|---|---|

| Issuer | Automating invoice issuance | ERP Integration |

| Investor | Access to trade receivables | Liquidity Pools |

| Platform | Settlement and compliance | Smart Contracts |

No comments yet. Be the first to share your thoughts!