What tokenized trade finance invoices infrastructure means

Tokenized trade finance invoices infrastructure is the technical backbone that allows traditional trade receivables to function as liquid, on-chain digital assets. It is not simply a marketing term for "crypto invoices." Instead, it represents a specific stack of blockchain protocols, data verification layers, and automated execution engines designed to bridge the gap between slow, paper-based international trade and fast, programmable finance.

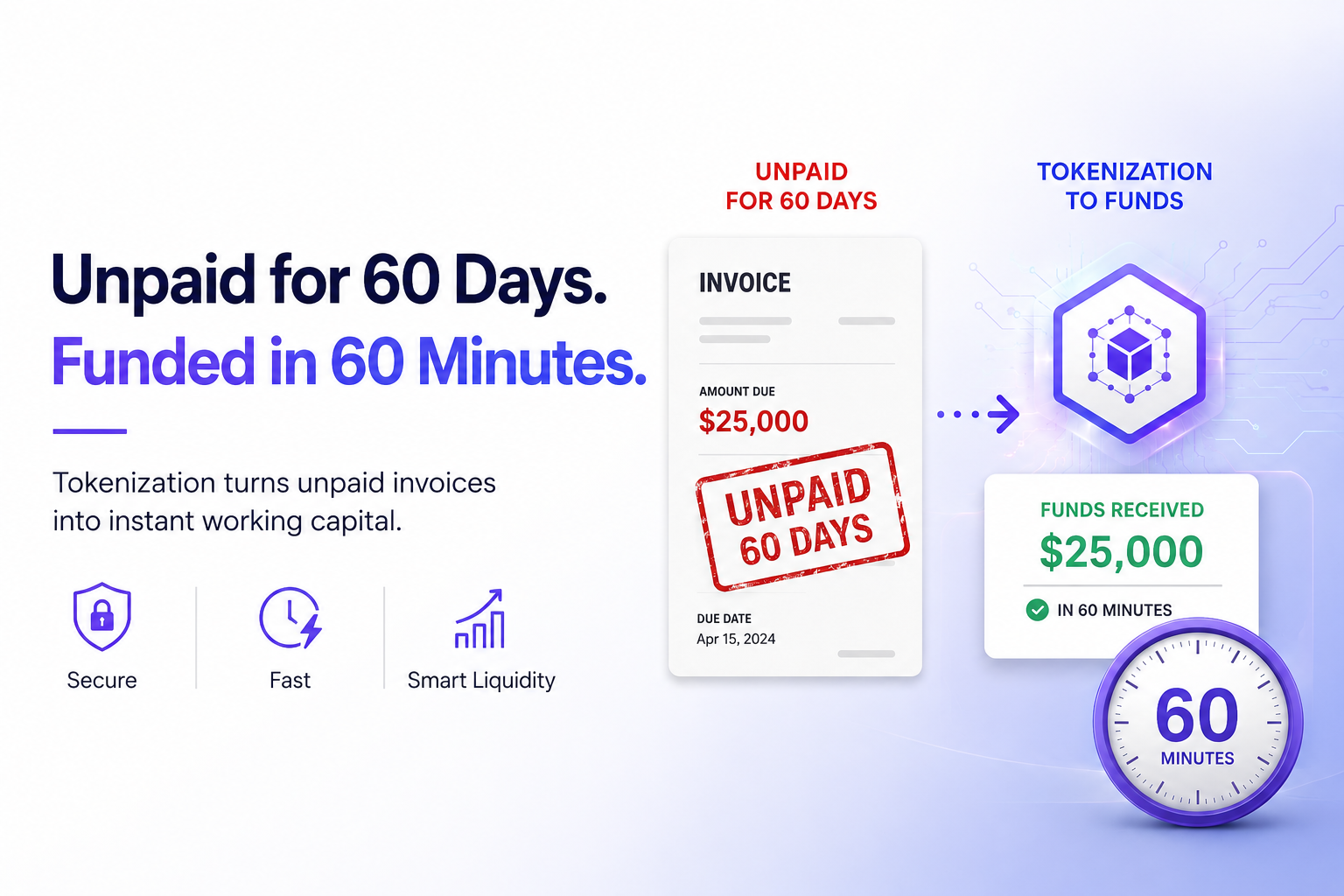

At its core, this infrastructure converts outstanding invoices into digital tokens. These tokens represent a claim on future cash flows. By moving these claims onto a blockchain, companies can collateralize them for immediate financing, fractionalize ownership to access a broader pool of capital, or automate settlement through smart contracts. The result is a system where trade finance becomes as fast and transparent as cryptocurrency trading, but grounded in real-world commercial transactions.

The infrastructure relies on three primary components working in concert:

- Blockchain Networks: These serve as the immutable ledger where tokenized invoices are recorded. The network must support smart contracts to enforce the terms of the trade finance agreement automatically. Common choices include Ethereum, Polygon, or specialized enterprise blockchains like Corda or Hyperledger Fabric, depending on the privacy and regulatory requirements of the participating banks and corporations.

- Oracles: Trade finance is inherently off-chain. An oracle is a critical data bridge that feeds real-world information—such as proof of shipment, customs clearance, or bank account balances—into the blockchain. Without accurate oracle data, the smart contracts cannot verify that the underlying trade event has occurred, making the tokenized invoice worthless. Chainlink is a prominent provider of this kind of decentralized oracle network, ensuring that the data feeding the token is reliable and tamper-proof.

- Special Purpose Vehicles (SPVs): To manage legal risk and isolate assets, tokenized invoices are often held within an SPV. This legal entity owns the underlying receivables and issues the corresponding tokens. The SPV ensures that if one party defaults, the assets are ring-fenced, protecting investors and complying with traditional banking regulations.

The goal of this infrastructure is to reduce the friction that has plagued trade finance for centuries. By automating verification and settlement, it reduces the time it takes to get paid from weeks to hours, while simultaneously lowering the cost of capital for small and medium-sized enterprises (SMEs) that traditionally struggle to access affordable financing.

The Infrastructure Behind Tokenized Invoices

Tokenizing a trade finance invoice is not just about creating a digital token; it requires a robust technical stack to ensure that the token on-chain accurately reflects the legal and financial reality of the underlying asset. Without this infrastructure, tokenized assets remain speculative rather than functional financial instruments. The process relies on three distinct layers: settlement mechanisms, data verification, and legal structuring.

Settlement: Stablecoins as the Medium of Exchange

At the foundation of the transaction is the settlement layer. In trade finance, speed and certainty are paramount, which is why stablecoins have become the preferred medium of exchange for tokenized invoices. Unlike volatile cryptocurrencies, stablecoins pegged to fiat currencies like the US dollar provide the price stability required for commercial transactions. This allows buyers and sellers to settle invoices instantly, 24/7, without the delays associated with traditional banking rails.

The liquidity of these stablecoins is critical. Investors need to be able to buy and sell tokenized invoices without significant slippage. To understand the health of this liquidity, it helps to look at the broader stablecoin market.

Source: TradingView. Chart showing USDC liquidity context.

Verification: The Role of Oracles

A token is only as good as the data backing it. Oracles serve as the bridge between off-chain reality and on-chain execution. In the context of invoice tokenization, oracles verify that the invoice exists, that the goods have been shipped, and that the payment terms are being met. This data is fed into smart contracts, which then release payments or transfer ownership of the token.

Without reliable oracles, smart contracts cannot execute automatically. They rely on external data providers to confirm that the conditions for payment—such as proof of delivery—have been satisfied. This reduces the need for manual verification and minimizes the risk of fraud, as the data is often sourced directly from enterprise resource planning (ERP) systems or logistics providers.

Legal Wrappers: SPVs and Asset Backing

The final layer is legal. Tokenization does not erase the need for traditional legal structures; it digitizes them. Special Purpose Vehicles (SPVs) are typically used to hold the underlying invoices. The SPV ensures that the assets are legally segregated from the originator’s balance sheet, providing bankruptcy remoteness for investors. This structure is crucial for institutional adoption, as it clarifies ownership rights and ensures that the tokens are backed by real, enforceable claims on payment.

Together, these layers create a secure environment where trade finance can be democratized. Stablecoins handle the money, oracles handle the truth, and SPVs handle the law. This triad allows tokenized invoices to function as legitimate, liquid assets in the global financial system.

Leading tools and platforms in the market

The infrastructure for tokenized trade finance is no longer theoretical. It is built on specific software platforms that bridge traditional banking systems with blockchain networks. These tools handle the complex work of converting unpaid invoices into digital assets, managing the legal wrappers, and connecting borrowers with liquidity providers.

Zoniqx: The Enterprise Bridge

Zoniqx operates as a supply chain finance platform that focuses on integrating with existing banking infrastructure. Rather than forcing companies to adopt new crypto wallets, Zoniqx connects directly to bank accounts and ERP systems. This approach allows businesses to tokenize their receivables while maintaining the compliance and security standards of traditional finance. The platform is particularly useful for large enterprises that need to digitize invoices without disrupting their current operational workflows.

ONINO: The Tokenization Engine

ONINO provides a more modular approach, offering the core technology to tokenize invoices and trade receivables. It acts as the engine that converts physical or digital claims into blockchain-based tokens. This platform is often used by fintechs and financial institutions looking to build their own tokenized finance products. ONINO handles the legal structuring and the minting process, ensuring that the digital tokens are backed by real-world assets. Their documentation outlines how to structure these transactions for 2026, emphasizing automation and reduced settlement times.

DeFi Protocols: Centrifuge and Maple Finance

For platforms looking to tap into decentralized liquidity, DeFi protocols like Centrifuge and Maple Finance offer direct access to crypto-native capital.

- Centrifuge specializes in bringing real-world assets (RWA) on-chain. It allows lenders to finance invoices, real estate, and other assets using stablecoins or crypto assets. The platform uses smart contracts to manage the lifecycle of the asset, from origination to repayment.

- Maple Finance focuses on institutional-grade DeFi. It facilitates undercollateralized lending by relying on credit assessments rather than just crypto collateral. For trade finance, this means borrowers can access capital based on their creditworthiness rather than locking up large amounts of crypto as collateral.

These protocols remove the traditional intermediaries, allowing for faster settlement and often lower financing costs. However, they require a deeper understanding of blockchain mechanics and smart contract risks.

Platform Comparison

Choosing the right tool depends on your existing infrastructure and risk tolerance. The table below compares the primary approaches.

| Platform | Type | Target Audience | Blockchain Compatibility |

|---|---|---|---|

| Zoniqx | SaaS Platform | Enterprise & Banks | Multi-chain (Enterprise) |

| ONINO | Tokenization Engine | Fintechs & Institutions | Multi-chain (Public) |

| Centrifuge | DeFi Protocol | Crypto Natives & SMEs | Ethereum & Polygon |

| Maple Finance | DeFi Protocol | Institutional Lenders | Ethereum |

Strategic advantages for businesses and investors

Tokenization transforms trade finance from a relationship-heavy process into a programmable asset class. For businesses, the primary benefit is immediate liquidity. Instead of waiting 90 days for a buyer to pay an invoice, the underlying receivable can be split into digital tokens and sold to investors instantly. This reduces the cash conversion cycle significantly, allowing companies to reinvest working capital faster without relying on traditional bank overdrafts.

The infrastructure also removes friction by reducing intermediary costs. In traditional trade finance, a single transaction might involve a exporter, importer, multiple banks, and insurers, each taking a cut and adding days to the settlement time. Tokenized invoices streamline this flow. By using stablecoin rails for settlement, funds can move 24/7 across borders with near-zero marginal cost, bypassing the legacy correspondent banking network.

For investors, the value proposition lies in access and transparency. Tokenization allows fractional ownership of high-value trade receivables, meaning smaller institutional investors or even accredited individuals can participate in trade finance pools that were previously reserved for large banks. This broadens the investor base, which in turn increases overall market liquidity. Also, because the trade data is recorded on-chain, investors have real-time visibility into the status of the underlying shipment and invoice, reducing the information asymmetry that often leads to fraud or default in traditional trade finance.

Risks and regulatory hurdles to watch

Tokenized trade finance invoices promise efficiency, but they introduce distinct legal and operational risks that traditional trade finance did not face. The core challenge lies in bridging the gap between digital code and physical legal reality. If a smart contract executes a payment automatically, does that satisfy the legal requirement for invoice settlement under local law? The answer is often "not yet," creating a enforceability gap that can stall liquidity or trigger disputes.

Legal enforceability of smart contracts

A smart contract is self-executing code on a blockchain. While it ensures transparency and speed, it lacks the legal standing of a traditional contract unless explicitly recognized by jurisdiction. For tokenized invoices, this means that if the code contains a bug or is exploited, legal recourse may be unclear. Unlike a standard bank transfer, reversing a blockchain transaction is technically impossible, placing the burden of accuracy entirely on the initial coding and legal framework.

KYC and AML compliance

Trade finance involves high-value transactions across borders, making it a prime target for money laundering. Tokenization does not remove the need for Know Your Customer (KYC) and Anti-Money Laundering (AML) checks; it shifts where they happen. Platforms must integrate identity verification layers that comply with regulations like the EU’s MiCA or the US’s FinCEN guidelines. Failure to embed these checks directly into the token issuance process can result in severe regulatory penalties and frozen assets.

Counterparty and oracle risk

In traditional trade finance, the risk lies with the buyer or the bank. In tokenized systems, you also face "oracle risk." Oracles are external data feeds that bring real-world information (like shipping status) onto the blockchain. If an oracle provides incorrect data, the smart contract may release payment for goods that were never shipped. This reliance on third-party data sources introduces a new layer of vulnerability that must be mitigated through diversified, redundant oracle networks.

Checklist for evaluating tokenization tools

Choosing the right infrastructure requires looking past the marketing to the underlying mechanics. A viable tokenization platform must bridge the gap between traditional finance compliance and blockchain efficiency. Use this framework to assess whether a specific tool fits your operational needs.

Ensure the platform uses a Special Purpose Vehicle (SPV) to hold the underlying invoices. This legal wrapper isolates risk and ensures that token holders have a clear, enforceable claim on the asset, separate from the issuer’s balance sheet.

The value of a tokenized invoice depends on accurate off-chain data. Evaluate how the platform uses oracles to verify invoice authenticity and payment status. Look for redundant data sources to prevent single points of failure in the verification process.

Tokenization is only valuable if you can exit. Verify whether the platform provides built-in secondary market access or integrates with existing liquidity pools. Without a clear path to resale, your invoice tokens remain illiquid digital receipts.

Trade finance is heavily regulated. The tool must support automated Know Your Customer (KYC) and Anti-Money Laundering (AML) checks at the token level. This ensures that only verified investors can trade your tokenized assets, maintaining regulatory compliance.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!