What tokenized trade finance invoices actually are

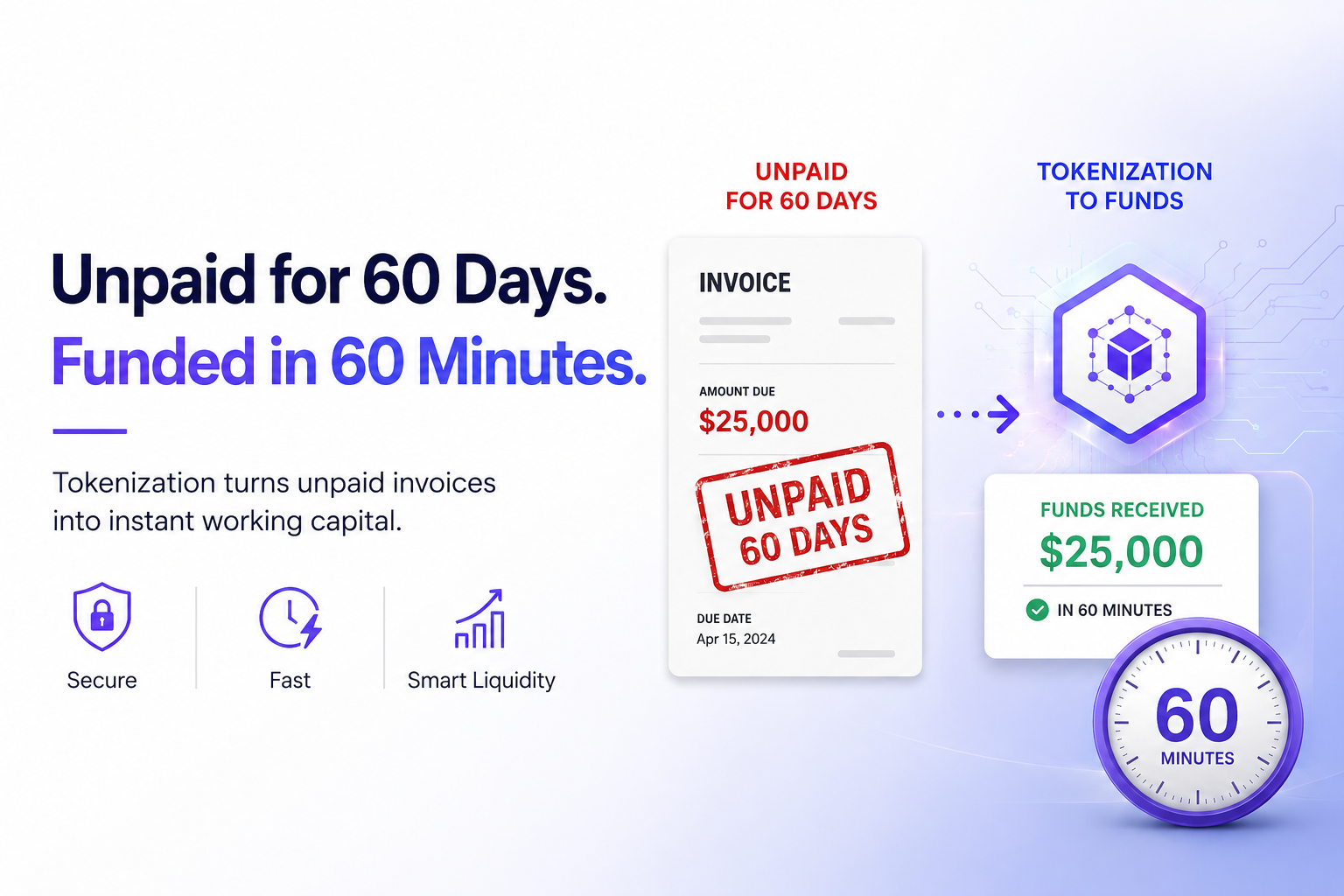

Tokenized trade finance invoices are unpaid commercial receivables converted into digital tokens on a blockchain. Instead of waiting 30 to 90 days for a corporate buyer to pay, a supplier can turn that invoice into a digital asset. This process transforms illiquid receivables into tradable digital assets, bridging traditional trade finance with DeFi liquidity.

Think of an unpaid invoice as a piece of real estate that is hard to sell in small chunks. Tokenization breaks that real estate into thousands of digital shares. Each token represents a fraction of the invoice’s value. Investors or liquidity providers can buy these tokens, giving the supplier immediate cash.

The mechanics rely on blockchain infrastructure to track ownership and automate payments. When the original buyer eventually settles the invoice, the smart contract automatically distributes the funds to token holders. This removes the friction of manual reconciliation and reduces the risk of double-spending or fraud.

Major platforms like Chainlink and ONINO are building the rails for this system. They ensure that the data backing the token is accurate and that the blockchain records are immutable. This creates a transparent ledger where every transfer of ownership is visible and verifiable.

For suppliers, this means better cash flow without taking on traditional debt. For investors, it offers exposure to trade finance yields that are often uncorrelated with broader stock markets. The result is a more efficient capital market where money moves as fast as data.

How tokenized trade finance invoices work

Tokenization turns an unpaid invoice into a digital asset that can be financed or traded on a blockchain. The process starts when a supplier issues an invoice and the buyer approves it. Once approved, the invoice data is hashed and recorded on a distributed ledger, creating a unique, verifiable digital token.

This digital representation solves a major problem in traditional trade finance: trust and transparency. In the old system, a supplier might sell the same invoice to multiple lenders, leading to fraud or "double-dipping." With tokenization, the blockchain records every transfer and ownership change. If a supplier tries to sell the same tokenized invoice twice, the network rejects the second transaction because the ownership is already assigned.

The workflow typically follows these steps:

The process begins with the supplier issuing an invoice for goods or services. The buyer reviews the delivery and formally approves the payment terms. This approval is the critical trigger that moves the invoice from a standard accounting record into the tokenization pipeline.

The approved invoice details—amount, due date, buyer identity, and goods description—are hashed into a cryptographic fingerprint. This hash is registered on the blockchain. The original sensitive data often remains off-chain in secure databases, while the blockchain holds the immutable proof of existence and validity.

A unique digital token is minted, representing the right to receive the payment specified in the invoice. This token is distinct and traceable. It can be held by the supplier, transferred to a financier, or split into smaller fractions to allow multiple investors to fund the same invoice.

The tokenized invoice can now be sold on a secondary market. Investors or liquidity providers buy the token, effectively lending money to the supplier against the future payment. The supplier gets paid immediately (minus a discount fee), and the investor holds the token until the buyer pays the full amount on the due date.

When the buyer pays the invoice on the due date, the funds are distributed according to the smart contract. The investor receives their principal plus interest, and the token is retired or burned on the blockchain. This closes the loop, ensuring no further claims can be made on that specific digital asset.

This structure reduces risk significantly. Because every step is recorded on an immutable ledger, financiers can see the entire history of the invoice. This transparency allows them to offer lower discount rates compared to traditional factoring, where due diligence is manual and opaque. The result is faster access to capital for suppliers and better returns for investors.

Why companies tokenize receivables

Tokenizing trade finance invoices shifts receivables from static assets into liquid, programmable instruments. Instead of waiting 60 to 90 days for payment terms to mature, companies can break down large invoices into smaller tokens and sell fractions to a global pool of investors. This process directly addresses three operational bottlenecks: cash flow timing, intermediary friction, and geographic capital access.

Accelerating cash flow

Traditional invoice factoring relies on a single financial institution to advance capital, often requiring lengthy due diligence. Tokenization automates much of this verification through blockchain transparency. By splitting an invoice into tokens, a business can access liquidity immediately upon token sale, rather than waiting for a bank’s approval cycle. This speed transforms receivables from a balance sheet liability into active working capital, allowing companies to reinvest in inventory or operations without waiting for the customer’s payment date.

Reducing intermediary costs

In traditional trade finance, multiple intermediaries—including banks, factoring companies, and clearinghouses—take cuts from the transaction. Each layer adds fees and delays. Tokenization creates a direct peer-to-peer or institutional-to-issuer channel. Smart contracts handle the distribution of payments automatically, reducing the need for manual reconciliation and administrative overhead. As noted in research on tokenized trade assets, this streamlined structure enhances efficiency by removing the need for redundant validation steps that occur in centralized systems [src-serp-3].

Accessing global capital pools

Local banks often have limited capacity to fund large trade volumes, especially for small and medium-sized enterprises (SMEs). Tokenization opens receivables to a worldwide investor base. Because tokens are standardized and tradeable on secondary markets, investors from different jurisdictions can participate without navigating complex cross-border banking regulations. This democratization of liquidity means a manufacturer in one country can find funding from investors in another, increasing the depth and stability of available capital [src-serp-7].

Traditional Factoring vs. Tokenized Receivables

The following comparison highlights the structural differences between legacy factoring and modern tokenized solutions.

| Feature | Traditional Factoring | Tokenized Receivables |

|---|---|---|

| Capital Source | Single Bank or Factor | Global Investor Pool |

| Speed | Days to Weeks | Near-Instant Settlement |

| Cost | High (Multiple Intermediaries) | Lower (Automated Smart Contracts) |

| Accessibility | Limited by Bank Capacity | Open to Qualified Investors Worldwide |

The Technical Stack Behind Tokenized Invoices

Tokenizing an invoice isn’t just about moving a file onto a ledger. It requires a specific stack of tools to bridge the gap between traditional trade finance and on-chain liquidity. Think of it as a three-layer engine: the blockchain handles the settlement, oracles provide the real-world data, and compliance layers ensure the transaction is legal.

Oracles: The Real-World Bridge

Blockchains are isolated systems; they don’t automatically know what’s happening in the physical world. Oracles like Chainlink act as the bridge, feeding verified off-chain data onto the blockchain. For trade finance, this means the smart contract can trust that an invoice exists, that it’s been approved, and that the goods were delivered. Without this data feed, a tokenized invoice is just a digital claim with no proof of reality.

Blockchain Platforms

The underlying ledger must handle high volume and low costs. While Ethereum offers security, its gas fees can eat into the thin margins of trade finance. Many platforms are turning to Layer-2 solutions or specialized permissioned ledgers that offer faster finality and lower transaction costs. The goal is to make the tokenization process cheaper than the paperwork it replaces. As noted by the University of Surrey, interoperability with legacy systems is just as important as the speed of the chain itself.

Compliance and Identity

You can’t move money without knowing who is moving it. Compliance layers integrate identity verification (KYC/AML) directly into the transaction flow. This ensures that only verified participants can hold or trade the tokenized invoices. This isn’t an afterthought; it’s a core component of the infrastructure that keeps the system secure and regulated.

Navigating Risks and Regulation in Tokenized Trade Finance

Tokenizing invoices shifts risk from opaque paper trails to transparent code, but it doesn’t eliminate the core challenges of trade finance. The primary advantage is reduced fraud and lower discount rates, as every transfer is recorded on-chain. However, businesses must still navigate complex regulatory landscapes that vary by jurisdiction. The International Trade Administration notes that while digital tools streamline processes, legal frameworks for cross-border tokenized assets remain fragmented 1.

Before adopting this infrastructure, conduct a rigorous due diligence process. Verify that your blockchain partner complies with local securities laws and anti-money laundering (AML) standards. Unlike traditional invoices, tokenized assets can be sold multiple times if safeguards fail, creating double-financing risks 2. Implementing smart contract audits and legal reviews is not optional—it is the foundation of secure adoption.

-

Legal review of tokenization structure

-

Assessment of blockchain interoperability

-

Due diligence on partner liquidity providers

-

Integration with existing ERP systems

The transition requires more than just technology; it demands a shift in operational mindset. Start with a pilot program involving trusted partners to test the workflow before scaling. This approach minimizes exposure to technical glitches or regulatory missteps while allowing your team to build internal expertise.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!